Taiwan Semiconductor Manufacturing Company (TSM) physically builds the most advanced, complicated, and microscopic components that drive the global economy and technological progress. TSMC reportedly earned 61% of the semiconductor foundry market share in the fourth quarter of 2023, blowing away second-place Samsung’s 14%.

Taiwan Semi is nearly unrivaled, expanding its moat around cutting-edge manufacturing by ramping up its industry-leading 3-nanometer technology.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Taiwan Semi’s clients include AI powerhouse Nvidia (NVDA), Apple, and other tech giants, making TSM stock a play on many of the biggest growth areas across the economy.

Taiwan Semi is crucially addressing geopolitical fears by expanding its manufacturing footprint outside of Taiwan, which is supported by its robust balance sheet and government incentives.

Taiwan Semi posted a beat-and-raise second quarter, driven by strong AI demand and beyond. Taiwan Semi’s upward EPS revisions earn TSM a Zacks Rank #1 (Strong Buy). Taiwan Semi is projected to grow its adjusted earnings by 25% in 2024 and 28% in 2025 on the back of 24% revenue growth in both years.

(Click on image to enlarge)

Image Source: Zacks Investment Research

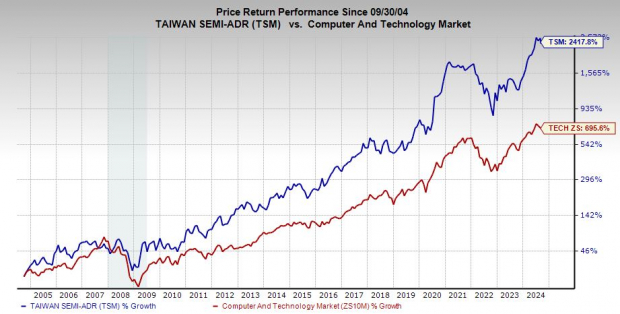

Taiwan Semi stock more than doubled the Zacks Tech sector over the last 10 years and nearly tripled it during the past two decades. TSM stock has climbed 60% YTD, yet it trades 15% below its July highs and 27% below its average Zacks price target.

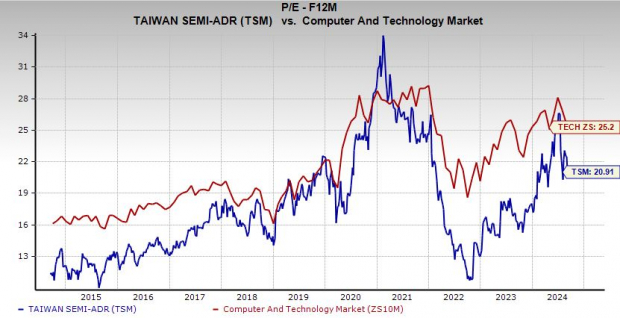

Taiwan Semi trades at a 40% discount to its 10-year highs at 20.9X forward 12-month earnings and 20% below the Zacks Tech sector.

Why Spotify Technology Stock is a Strong Buy

Spotify Technology S.A. (SPOT) was one of the pioneers of paid streaming music, helping alter the music industry in the same way Netflix changed TV and movies. Despite competition from tech giants, Spotify reportedly held 32% of the global streaming music market share in 2023, blowing away No. 2 Apple Music’s 15%, as well as YouTube’s 14% and Amazon’s 13%.

Spotify grew its Premium Subscribers by 80% between Q2 FY20 and Q2 FY24, while monthly active users surged 110%.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Spotify's commitment to efficiency and price hikes in back-to-back years have helped it reach a profitability inflection point. SPOT’s FY24 EPS estimate has surged 28% since its Q2 release, with its FY25 figure 22% higher, helping it land a Zacks Rank #1 (Strong Buy).

SPOT’s recent bottom-line revisions are part of an impressive trend that’s seen its FY24 EPS estimate skyrocket 930% over the last 12 months, with its FY25 figure up 280%.

Spotify is projected to swing from an adjusted loss of -$2.95 a share last year to +$6.37 per share in 2024 and then surge 38% next year. Spotify is projected to grow its revenue by 19% in 2024 and 15% next year to reach $20 billion—doubling revenue between FY20 and FY25.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Spotify stock has soared over 300% off its 2022 lows, including a 75% YTD climb. Yet Spotify trades around 10% below its 2021 peaks and 15% under its average Zacks price target.

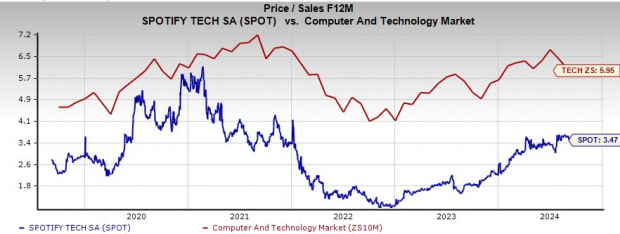

Spotify trades at a 75% discount to its 12-month highs at 44.1X forward 12-month earnings. On top of that, Spotify trades at a 40% discount to the Zacks Tech sector and 41% vs. its highs at 3.5X forward 12-month sales.

Why AppLovin is a Must-Own Under-the-Radar Tech Stock

AppLovin Corporation (APP) helps companies and app developers acquire and keep their ideal users, increase value across a customer’s lifecycle, measure their marketing and reach, and much more. AppLovin’s new machine learning and AI engine AXON 2.0 is generating impressive results for its clients in mobile gaming and beyond.

(Click on image to enlarge)

Image Source: Zacks Investment Research

AppLovin grew its revenue by 17% last year, following slightly higher 2022 sales and 93% growth in 2021. The app monetization company posted another beat-and-raise quarter in early August, pointing to its potential to expand its market share in mobile gaming and grow into new advertising categories.

APP’s FY24 and FY25 earnings estimates surged 14% and 17%, respectively since its last release, with both estimates up 150% from a year ago. AppLovin’s upbeat EPS revisions help it earn a Zacks Rank #1 (Strong Buy).

Wall Street fell in love with AppLovin because its new AI-enhanced features are boosting ROIs for APP’s clients, leading to booming sales and earnings for AppLovin. mobile gaming and apps are an under-than-radar growth segment in our smartphone-obsessed world. AppLovin is projected to grow its revenue by 35% in 2024 to help boost its EPS by 255%, with 14% and 20%, respective growth to follow in 2025.

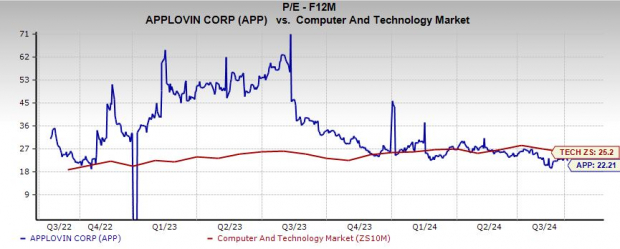

(Click on image to enlarge)

Image Source: Zacks Investment Research

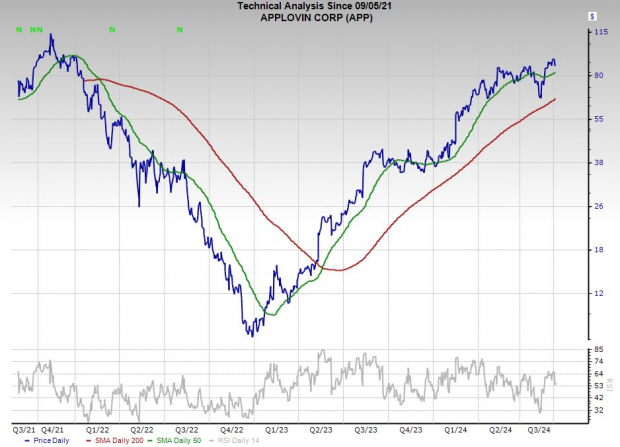

AppLovin has soared 800% since the end of 2022, blowing away Nvidia’s 560%. APP stock has popped 105% in the last year, yet it is down 5% from its 52-week highs and 15% below its 2021 peaks.

AppLovin trades at over a 95% discount to its three-year highs, 50% below its median, and at a 12% discount to the Zacks Tech sector at 22.2X forward 12-month earnings.

More By This Author:

3 Market-Crushing Stocks To Buy For Value And Growth In September3 Nuclear Energy Stocks To Buy And Hold Forever

Bear of the Day:H&E Equipment Services, Inc.

Comments

Log in or sign up to join the conversation.