Towards A New Silver Short Squeeze?

Image Source: Pixabay

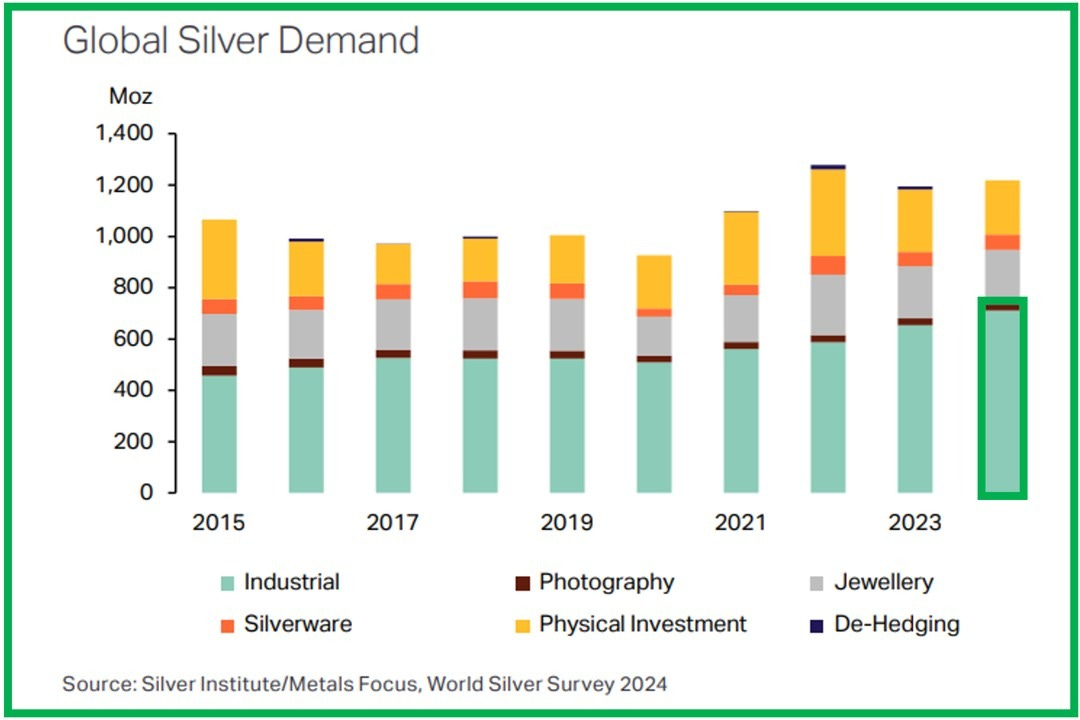

In the last exclusive bulletin to GoldBroker clients, I discussed the rather positive outlook of the recent report from the Silver Institute. It seems likely that last year's silver shortfall will be repeated next year. The current supply is unable to keep pace with ever-increasing demand.

What's new this year is the increase in industrial demand for silver, offsetting the fall in investment demand:

Industrial demand is strong due to the increase in solar panel production in China.

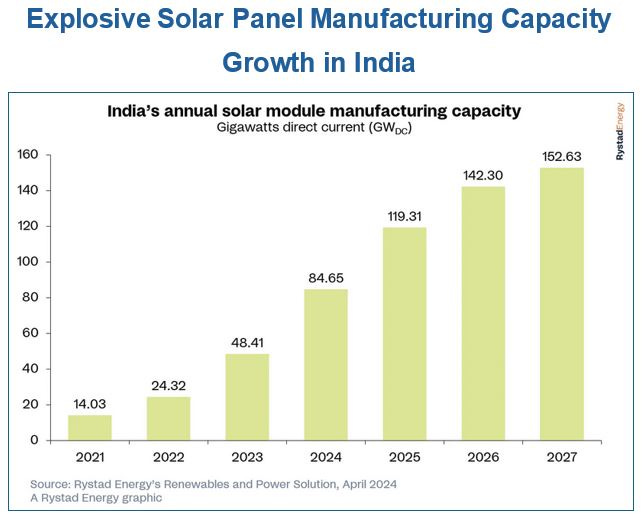

However, this demand also extends to India, which plans to quadruple its production capacity by 2027:

This increase in production is helping to accelerate the reduction of stocks on the Chinese market:

And as stocks on the Chinese market fall, silver premiums rise:

In my bulletin from September 21, 2023, I analyzed the impact of China's premiums on the determination of gold prices.

At the time, I explained that rising premiums were a sign of a new surge in gold prices:

“The effect of this squeeze is to strengthen arbitrage opportunities, increase the flow of physical gold to the East and support the price of gold (precisely because of these arbitrage opportunities).

In recent days, China has raised its import quotas for physical gold, but premiums remain very high. The price of an ounce of gold is $75 higher in Shanghai than in London.

If these premiums persist, arbitrage opportunities are likely to accelerate delivery requests on the COMEX, further complicating the control of futures prices by participants wishing to protect their short positions.

Supply tensions on the Chinese market could enable the gold market to move closer to a true price-determining mechanism linked to physical demand.”

With silver premiums on the rise in China, one wonders whether we are on the verge of an arbitrage phenomenon similar to that which has already occurred in gold.

The persistence of premiums in Shanghai has had the effect of sustaining the rise in the price of gold since last September.

As observed at the beginning of this week, as soon as the Chinese market opened, silver started to rise again due to the differential between silver prices quoted in London and those quoted at a much higher level in Shanghai.

Will this price differential continue to drive up silver prices?

Will we see demand for physical delivery on the COMEX from investors wishing to take advantage of the price differential between the two markets?

Will the arbitrage between Western and Asian silver prices accelerate the drainage of COMEX stocks?

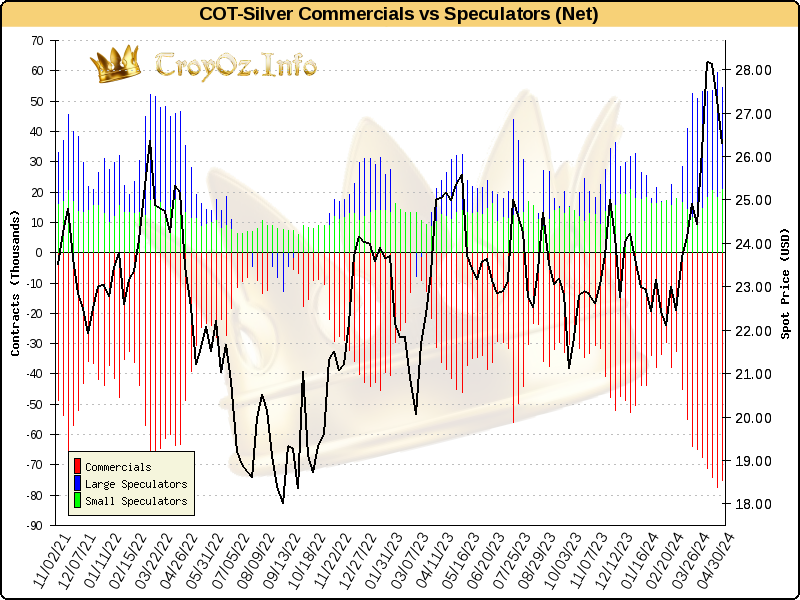

This rush to the COMEX comes at a time when commercials have not significantly reduced their short positions in futures contracts:

In other words, Asian demand could potentially lead to conditions conducive to a short squeeze on the COMEX.

However, unlike the last Silver Short squeeze of 2021, the demand this time isn't coming from "degenerate" investors or "Silver bugs" gathered on a forum, looking to hoard coins and bullion to restrict the physical supply.

This time, demand is linked to industrial storage in anticipation of a sharp rise in silver consumption for solar panel production in India and China.

Under these conditions, a possible Silver Short Squeeze 2 could probably have a far more significant impact on silver prices.

For the moment, silver prices continue their consolidation phase. Despite three consecutive margin increases in a single month, futures maintained their bullish short-term pattern. The 10-day moving average served as support, while most analysts were anticipating a more pronounced pullback and a test of the breakout:

Historically, silver price corrections have been more abrupt. So to see silver bounce back at the start of this week after such a marked period of consolidation is rather encouraging.

The volumes of the latest decline are also lighter than those of previous bullish sessions.

During the summer 2020 peak, we had in fact observed the opposite: there was much more volume during corrections.

This good configuration of silver is very positive for mining stocks.

As we've been saying for a long time in these newsletters, mining stocks graphically follow the silver metal chart.

This has been even more evident since the consolidation began in the summer of 2020: the juxtaposition of the two curves is quite remarkable!

Why does the mining index follow the silver chart?

Several theories have been put forward to explain the correlation between these two assets.

The predominance of passive funds is undoubtedly the most plausible explanation. GDX is "set" on silver by an algorithm...

It is likely that a short squeeze on silver will lead to a strong catch-up in mining stocks if this correlation continues!

This mining index is on the verge of breaking through resistance that has lasted since 2011:

The Silver Short Squeeze of 2021 failed to break through this resistance.

A silver short squeeze triggered by strong demand of physical silver in Asia could this time have a very different effect on silver mining companies.

More By This Author:

Are Europeans Over-Saving Out Of Fear For The Future?Fed Not Yet Pivoting Despite Deteriorating US Economy

The Impossible Equation Of Global Debt

Disclosure: GoldBroker.com, all rights reserved.