Although deep in the midst of the pandemic and its immediate economic impacts, economists are now turning their attention to the long haul and the lasting legacy of COVID-19. Every major economic downturn leaves some scars, and this downturn signals lasting damage to our economic wellbeing. The consensus is building that our growth potential will be lower than that experienced pre-COVID-19; we cannot expect a return to customary growth paths.

Economists prefer to measure economic performance against a standard of “potential output”, a measure of how well labor and investment capital combine to generate productivity improvements and overall output. Simply put, potential output is reached when there is very low unemployment (approximately 3%) and all available productive business investment is fully utilized. Although potential can’t be directly measured, economists are able to infer reliable estimates of growth trends. It is the future growth trends that are undergoing permanent downward shifts.

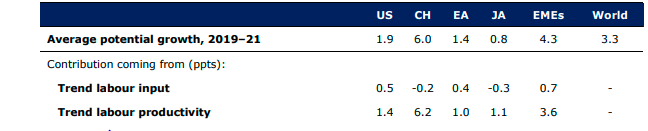

Pre-COVID-19 World. Figure 1 estimates potential growth in the major economies based upon research at the Bank of Canada. In 2019, the Bank estimated global potential output to expand by 3.3%, led by China at 6% and the emerging markets at 4.3%. While these growth trends are somewhat lower than we experienced earlier in this century, they are, nonetheless, adequate to generate a high level of employment and a gradual improvement in overall economic well-being.

Figure 1 World Potential Growth Estimates, 2019 Pre-COVID-19

(Click on image to enlarge)

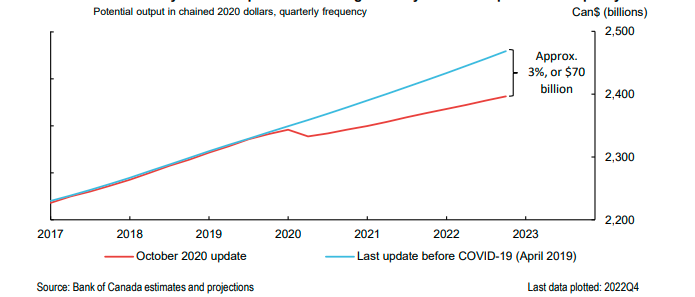

Post-COVID-19 World. In a recent speech, Carolyn Wilkins, outgoing Senior Deputy Governor of the Bank of Canada reported the Bank has revised its estimate of potential output growth over the next few years from about 3¼ % to 2½ %., a marked reduction from the pre-COVID world. The major revisions have the US potential growth dropping down to 1.25%, compared to nearly 2% previously. To better appreciate the impact of this downward revision, Figure 2 measures the cumulative impact of a lower growth for Canada, resulting in a drop in total output of 3% at the end of 2022.

Figure 2 Canadian Potential Pre- and Post-COVID-19

(Click on image to enlarge)

Wilkins argues that,

“we expect that COVID-19 will leave an unfortunate economic legacy through its impacts on investment, the work force and productivity. In our most recent projection, this adds up to a situation where Canada is likely to exit the pandemic with a lower profile for potential output. That means a significantly diminished ability to generate goods, services and incomes on a sustainable basis. And many of those scars could become permanent without deliberate actions from all of us.”

What lies behind this “unfortunate economic legacy”? First, we know that a prolonged recovery results in much weaker business investment in plant, equipment, and technology. Much of this weakness reflects slow growth in overall demand, resulting in thousands of firms shutting down permanently and others putting off expansion plans indefinitely. The Bank estimates that about three-quarters of the reduction in potential growth lies with weak business capital accumulation. Secondly, we are experiencing so many disruptions in the workplace and in supply chains that overall productivity growth has suffered. And, it is productivity growth that lies at the heart of potential growth. From today’s vantage point, we do not know the full extent of the negative impact on productivity, but our instincts are that it will be significant

Comments

Log in or sign up to join the conversation.