Image Source: Pexels

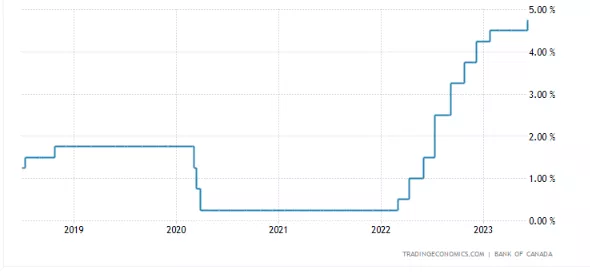

Pity the Bank of Canada when it tries to time its rate policy decisions. During 2021 when inflation was starting to percolate throughout the world, the Bank of Canada was very reluctant to raise its bank rate, arguing that inflation was ‘transitory’. To be fair, central bankers everywhere looked at the impact of the pandemic and concluded that inflation was temporary, fuelled by the disruptions in the world’s supply of goods. Then the Russian invasion in February 2022 resulted in a surge in commodity prices, especially food, and energy, and inflation literally was off to the races. Complacency quickly changed to near panic behavior as the Bank of Canada instituted a steady stream of monthly increases, from near zero to yesterday’s rate setting at 4.75%. The Bank hints that more rate hikes are possible.

Bank of Canada Rate Hikes

At its April 2023, policy meeting, the Bank paused in its rate hikes. It cited that” inflation in many countries is easing in the face of lower energy prices, normalizing global supply chains, and tighter monetary policy” The rate of inflation was falling and there was no need to raise rates further. One could almost feel a sigh of relief that price changes were no longer dominating the public discussion.

This writer finds the June 7th decision to increase the policy rate by another 25bps very strange and far from defensible (rate announcement). To begin with, the Bank of Canada’s press release notes that “globally, consumer price inflation is coming down, largely reflecting lower energy prices compared to a year ago“and “growth around the world is softening in the face of higher interest rates”. Virtually the same observation given in its April policy statement.

Why raise rates further? Even more so, why warn that we anticipate possible more rate increases in the coming months? Now, a sleuth of economists has jumped on the bandwagon and telling clients to brace for more rate hikes. It was only a month ago, the collective wisdom anticipated no more rate hikes and possibly a rate cut starting in 2024.

The Bank of Canada argues a rate hike is justified because“consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains. Demand for services continued to rebound. In addition, spending on interest-sensitive goods increased and, more recently, housing market activity has picked up.” One wonders why the Bank of Canada adopts an anti-growth mentality. Is it because inflation is running at 4.5%? But in the same breath the Bank expects rate to drop to 3% later this year?

In an earlier blog, the writer argued that the contraction in the money supply will ultimately result in a recession (monetary contraction). The commercial banks are tightening up credit conditions and battening down the hatches by taking large loan loss reserves in anticipation of defaults, especially in the commercial real estate market and mortgage debt (loan losses). Raising the cost of capital while restricting the supply of credit is the ultimate in anti-growth philosophy---all in the name of reaching a 2% inflation target?

What makes the Bank’s decision more troubling is that “concerns have increased that the CPI inflation could get stuck materially above the two percent target”. Does that mean the rates continue to go up while inflation remains above the 2% level? Perhaps, it is time to have a public discussion about what is the appropriate inflation target to adopt. After all, the 2% figure has no basis in economic theory, so why stick with it?

More By This Author:

Canadian Banks Signal The Coming Economic Downturn

Why Central Banks Forecasts Totally Missed The Surge In Inflation

What Lies Behind The Downgrading Of Canadian Banks

Comments

Log in or sign up to join the conversation.