Image Source: Pexels

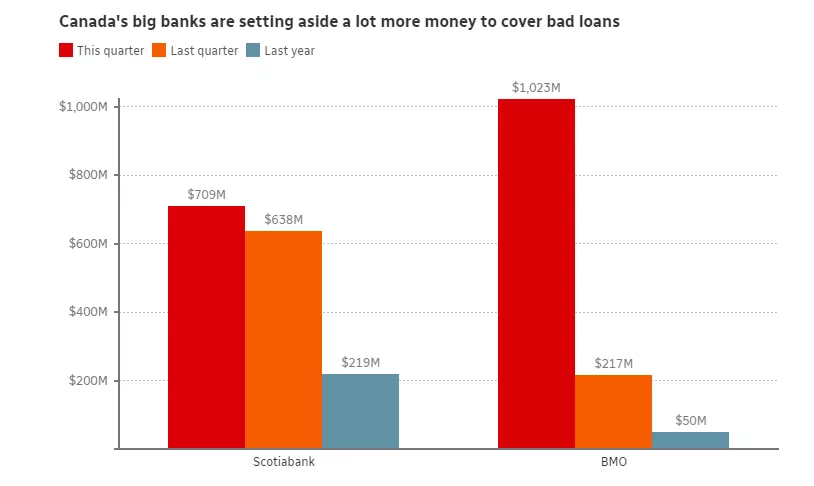

The Canadian banks registered very disappointing performance in the second quarter as profits fell by as much as 20% y/y. This reflects a weakening loan book coupled with higher staffing and technology costs. Moreover, all banks are anticipating a gloomier outlook for Canada's economy as they set aside money to write off bad loans in the coming quarter. The PCL, provisions for credit losses, are closely monitored as an indicator of future economic performance. To be fair, bank officials are making educated guesses on loan losses which have often proven to be overly pessimistic, in which case profits are enhanced in subsequent quarters. Nonetheless, today’s revised PCL projections are quite dramatic and should be a warning to the Bank of Canada that future rate hikes need to be very carefully considered as to their negative impacts on credit markets.

In an earlier blog, I pointed out that Canadian banks were collectively downgraded as the investment community is taking a dim view of Canada’s short-term to medium-term prospects. Of special note is the steady contraction in the money supply and its negative results (Downgrades). The big question for investors is how to price bank stocks, given the prospects for a weakening economy.

(Click on image to enlarge)

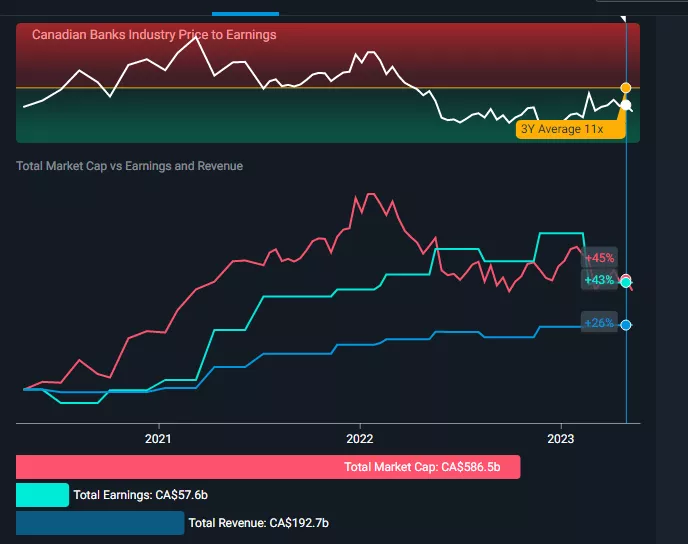

The exuberance for Canadian bank stocks hit a high point in early 2021 when the P/E ratio for the overall industry hit 13.6 and the market cap reached C$ 1.1 trillion. Canadians were in love with their banks during the height of the pandemic. Deposits were way up as consumer savings soared during the pandemic, supported by government cash payments. Since that high water mark, Canadian banks started a steady downward shift. Today the industry P/E has dropped to 9.9 and its market cap is down by 14%.

By no means are the Canadian banks stressed. Although the mortgage market, both residential and commercial, represents a large portion of bank loans, delinquencies, and defaults are well within acceptable ranges. However, the banks have made it known that they will work with clients to ease some of the stress from the surge in interest rates, such as changing amortization periods and repayment schedules.

The Canadian banks are just echoing concerns expressed by the Bank of Canada in its most recent review of financial conditions. (Review). The Bank expects households to face growing pressures from mortgage renewals, lower homeowner equity, and more expensive consumer loans. In sum, the Canadian banking sector is in for a rough ride as the full force of the surge in interest costs hits the real economy.

More By This Author:

Why Central Banks Forecasts Totally Missed The Surge In Inflation

What Lies Behind The Downgrading Of Canadian Banks

The Bank Of Canada Sets The Bar Way Too Low When It Comes To Economic Performance

Comments

Log in or sign up to join the conversation.