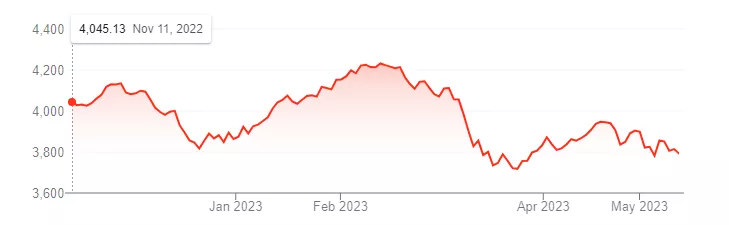

Once the darlings of Canadian investors, the Canadian banks have fallen out of favour and recently received a series of downgrades from a group of analysts. After reaching a high in February, the Canadian composite bank index has fallen 10%, while the overall index remained unchanged.

TSX Composite Bank Index

For those unfamiliar with the Canadian banking system, it is important to recognize that Canadian banks operate in an environment quite different from that of the US. Canada has a unity banking system, dominated by six large banks---akin to the money centre banks in the US. Canadian banks have a much lower concentration of assets in any one industry and thus are not exposed in the way US regional banks are. Finally, it has been decades since a Canadian bank has failed and that bank was a second-tier institution that posed no systematic risk. Overall, Canadian banks are much more cautious lenders than their neighbours to the south and are more stringently regulated.

Hence, the downgrades seem more unlikely given the relative strong position Canadian banks enjoy vis-a-vis their American counterparts. To wit:

- Deposits have steadily grown, in post-pandemic years, and offer a reliable source of loanable funds;

- Canadian banks exhibit very low P/E multiples, even on a historical basis. Dividend yields are touching 6 % and there is no reason to expect any diminution in the dividend payout ratio in the future;

- Net income margins ----the spread between the interest income a bank earns through lending and the interest it pays out to its lenders -----have been augmented as deposit rates lag increases in the prime rate;

Yet, collectively, there is a sense that Canadian banks face a very uncertain near-term outlook, resulting in downgrades, ranging from: ‘overweight’ to ‘equal weight’ (TD) and from ‘overweight’ to ‘underweight’ (RBC); ‘ equal weight’ to ‘underweight’ (Scotiabank). The bloom has clearly come off the rose. (Downgrade).

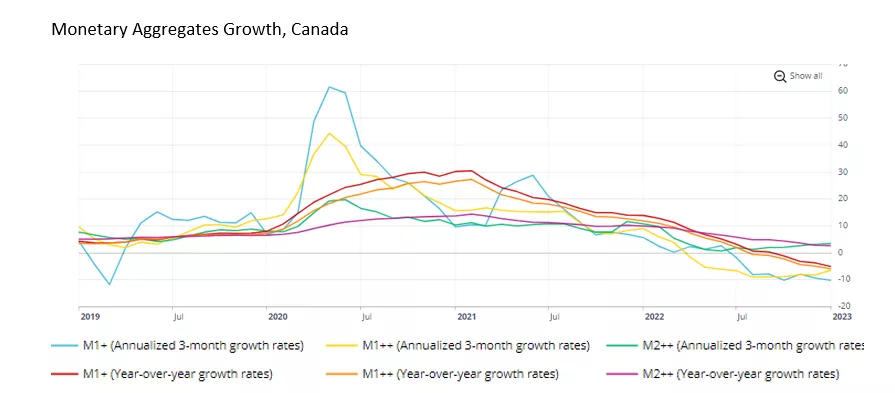

In an earlier blog, I pointed out that the monetary aggregates are already in negative territory, suggested by the contraction of the broadly-defined money supply. (credit contraction). Simply, economies cannot grow if credit conditions--- the price and/or supply of funds--- continuously tighten as is the case now.

(Click on image to enlarge)

Unlike the US banking system, Canadian banks retain most mortgages on their books, rather than repackaging into a secondary market such as mortgage-backed securities. Banks hold 75% of all Canadian residential mortgages. So far, these mortgages have not been a strain on the banks in terms of delinquencies or defaults. However, the bulk of mortgages underwritten less than 5 years ago, at very favourable rates, will be subject to rate increases. The full impact on the mortgage market remains in the future. Finally, although there is a broad consensus that the Bank of Canada has finished raising rates in this most recent rate cycle, the Bank continues to warn investors that it will raise rates should inflation reverses its downward trend.

Hence, the uneasiness among bank analysts.

More By This Author:

The Bank Of Canada Sets The Bar Way Too Low When It Comes To Economic Performance

Monetary Contraction Is Now In Full Force In Canada

Canadian Bond Investors Are Totally Disconnected From The Bank Of Canada

Comments

Log in or sign up to join the conversation.