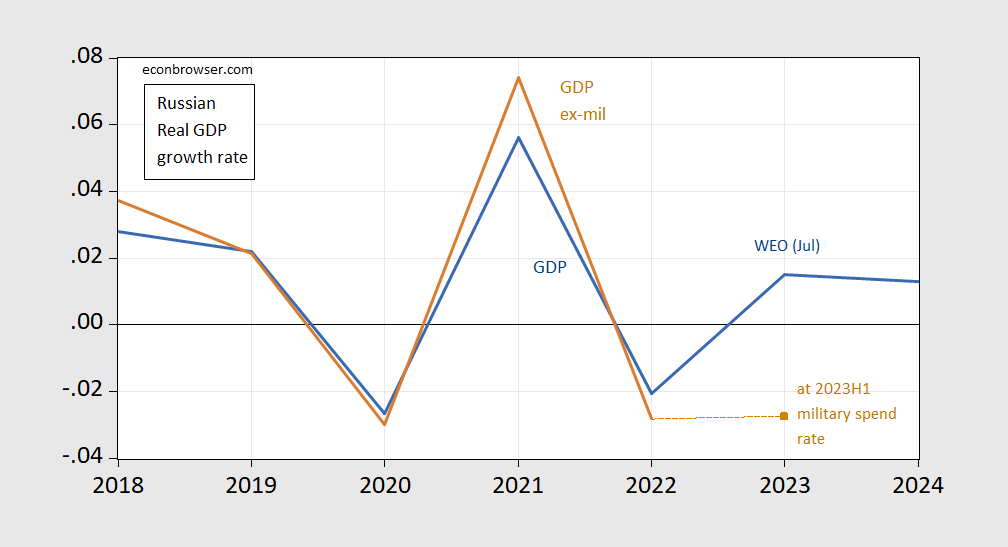

There has been much discussion of how Russian GDP growth exceeded some forecasts (see discussion here). While GDP measures output, it does not measure only output that contributes to necessary to welfare. It also excludes non-market mediated activities. One big change in the past year and a half is military expenditures, which is now a larger component of GDP. In Figure 1 below, I show real GDP growth y/y as reported, and real GDP growth ex-military spending as tabulated by SIPRI.

Figure 1: Russian real GDP growth (blue), and GDP ex-military spending (tan), both y/y. GDP growth for 2023 and 2024 is IMF WEO July 2023 forecasts. 2023 ex-military spending value is calculated using spending rate in 2023H1. Source: GDP from IMF WEO (April, July), military spending from SIPRI, Reuters.

Note that the calculation of real GDP ex-military spending relies upon applying the GDP deflator to the GDP ex-military spending output. In the absence of reliable deflators for the two components, this is just an expedient.

The calculations imply that y/y GDP ex-military spending contracted at a rate of 2.8% in 2022, and will again in 2023, assuming that military spending in 2023H2 proceeds at the same nominal rate it did in 2023H1 (the April 2023 IMF WEO assumed about 10% inflation rate in the GDP deflator, so my assumption is pretty conservative I think).

One might be very well skeptical of the validity of these calculations, given doubts about Russian GDP statistics, as well as SIPRI calculations. I will note that a lot of the surge in manufacturing production seems to be defense related (see discussion at BOFIT), so something of this phenomenon shows up in other statistics.

More detailed discussion from this June SIPRI report.

If one wanted to calculate net GDP (another step in the process of calculating the old Tobin-Nordhaus MEW), one would likely get a lot slower growth than reported in GDP. That’s because lots of capital has become obsolescent faster given sanctions; that’s not to mention the destruction of military capital assets.

On this last point, I gave up trying to calculate and/or estimate a number. For instance, in a July Bloomberg article:

“Russia has lost nearly half the combat effectiveness of its army,” Radakin told the legislature’s defense committee. “Last year it fired 10 million artillery shells but at best can produce 1 million shells a year. It has lost 2,500 tanks and at best can produce 200 tanks a year.”

Without knowing the composition of the 2500 tanks (T-90s vs T72s, etc.), and valuation, it’s hard to say how gross investment differs from net.

More By This Author:

Uncertainty In ChinaNo GDP Downturn Forecasted: SPF

Chinese Growth In Question (Again) - Updated

Comments

Log in or sign up to join the conversation.