Photo by Ervin Lukacs on Unsplash

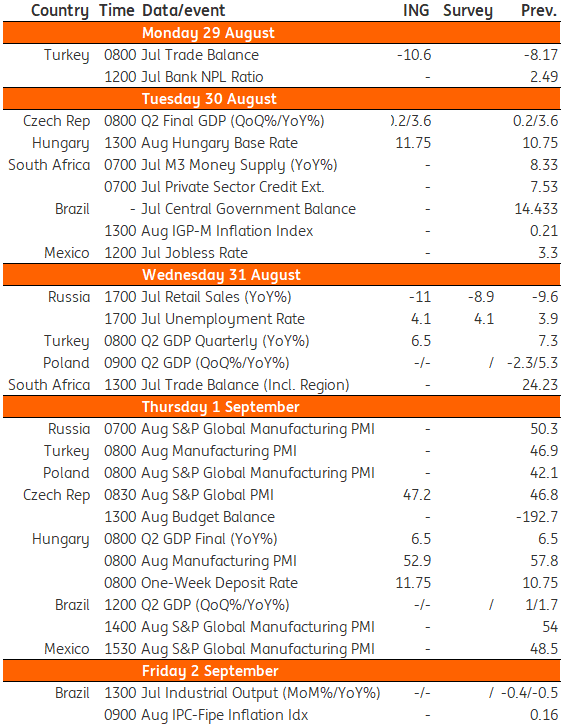

We're expecting a 100bp rate hike from Hungary's central bank next week, as well as some strong growth figures in Turkey.

Hungarian central bank set to hike by another 100bp

We expect the Hungarian central bank to continue with decisive tightening by implementing another 100bp rate hike next week. Based on our updated inflation outlook, we expect additional measures alongside the hike sooner rather than later too, which could help to reduce excess liquidity and therefore improve monetary transmission, supporting the forint. We might see the first steps in that direction as soon as next week's rate-setting meeting.

Besides that, we will get more detail on the stronger-than-expected second-quarter GDP growth figure, with consumption and investment activity likely to be in the driver’s seat. August manufacturing PMI will remain elevated given order books are full and companies are still able to pass rising costs onto consumers.

Turkey: Expect strong second-quarter growth despite initial signs of a slowdown

Based on early indicators, we think the Turkish economy put in another strong performance in the second quarter, with 6.5% YoY growth. However more recently there have been initial signs of a slowdown relative to the first half of the year. We expect economic activity to lose momentum in the second half for a few key reasons. Firstly, a higher risk premium in financial markets and growing macro-stability risks could weigh on domestic demand. Secondly, there's a likely loss of momentum in exports given the slowdown in the eurozone. Finally, we're seeing continued cost pressures, tighter global financial conditions, and a challenging local regulatory environment, putting pressure on the corporate sector.

Key events in EMEA next week

Image Source: Refinitiv, ING

More By This Author:

Rates Spark: Down The Jackson Hole

Impact Of China’s Drought Is Small Compared To Its Real Estate Crisis

Could Double-Digit Inflation Be On The Cards For The Eurozone?

Comments

Log in or sign up to join the conversation.