Jerome Powell's in the spotlight, but equally important for the immediate Fed outlook will be the upcoming job report next week and the CPI print that follows. He may strive to endorse the market's recently rediscovered hawkishness, but also needs confirmation in the data. The ECB minutes pointed to more tightening ahead, with a hint at the balance sheet.

Powell to speak against an already hawkish-leaning backdrop

Many will have marked Fed Chair Jerome Powell’s speech today as the highlight of the week. Whether he will prove as market-moving as some expect is still to be seen. A likely scenario is that he will endorse the retightening of financial market conditions and thus also the trend towards higher market rates of late, given that the Fed still is a stretch away from getting inflation under control.

Emphasis on the terminal rate may be an attempt to shift the focus away from a slowing hiking pace

Recent Fed speakers have indeed provided a more hawkish backdrop, confirming the market leaning toward such an outcome. The Fed’s Esther George assessed that the Fed still needed to raise rates further to slow demand and bring inflation down, highlighting the importance of clear communication of the destination the Fed is headed – and that could even be above 4%. She pushed back against the notion of cuts following on the heels of the tightening cycle, where the market is currently seeing the peak in the Fed funds rate at close to 3.8% in the first quarter of next year, before pricing in first-rate cuts again.

Putting the emphasis on the terminal rate may be seen as an attempt to shift the focus away from the Fed slowing its hiking pace soon. Whether that happens already in September will be determined by the data – 300k, as is currently the consensus for next week’s payroll increase, would leave a 75bp hike still on the table. We suspect that the next CPI release and whether it can confirm the notion of peak inflation will be more relevant. Here economists see the risk of the core inflation reading still heading higher.

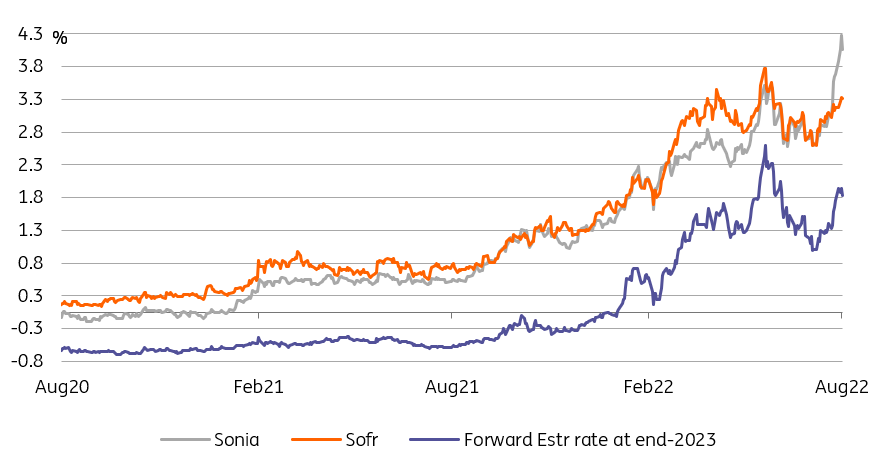

The Fed has European markets to thank for a tightening of financial conditions

Image Source: Refinitiv, ING

ECB still has more tightening to do – could the balance sheet be next?

The main takeaway from the European Central Bank minutes was the signaling of more hikes to come as the outlook for inflation worsened. The larger increase of 50bp in July should be understood as a frontloading of the normalization process, but not as a change of the end-point of the cycle. This end-point will only crystallize once interest rates get closer to it, and – as also our economists have noted – it probably remains a moving target.

While data continues to point lower, even if not as bad as feared as was the case with yesterday’s German Ifo, the ECB appears reluctant to use the word recession. The ECB minutes suggested the central bank continues to hold on to a more optimistic view of the economy, at least at the last July meeting.

Abandoning the rates guidance has provided much-needed flexibility, but balance sheet guidance remains

The minutes also foreshadowed a discussion that could add upward pressure to longer-dated rates. Abandoning the rates forward guidance has provided much-needed flexibility in setting monetary policy. But there still remains guidance in place for the balance sheet, or more precisely the reinvestment of the QE portfolios. For now, the ECB intends to reinvest maturities of the Asset Purchase Programme portfolio “for an extended period of time past the date when it started raising the key interest rates”. Pandemic Emergency Purchase Programme maturities will be reinvested at least until the end of 2024. No direct conclusions were drawn just yet in the minutes, but already earlier, the ECB’s Isabel Schnabel and Bundesbank’s Joachim Nagel hinted that the balance sheet would have to be considered at some point.

Next week the ECB will have to contemplate another CPI print, and given the underlying rise in energy (gas) prices the trend continues to point higher – our economists do not exclude a peak in the double digits. Adjusting the reinvestment guidance may offer the ECB another lever on monetary policy, though we would caution that at a time when flexible reinvestments are used to contain sovereign spreads, talking about reducing reinvestments could prove counterproductive.

Today’s events and market view

Powell's Jackson Hole speech is the day's highlight. Although rates have eased a little lower with the 10Y UST almost touching the 3% mark again, the market is leaning hawkish toward this event. Other Fed speakers have already sounded hawkish tones, such as Esther George just yesterday, setting the backdrop for Powell.

In these turbulent markets, investors will also have to contend with a resurgence in supply as September draws near. We're expecting €25bn of European government bond supply next week, to which the EU will add a €4bn tap.

Other releases of note today are the personal income and spending data. Consumer spending should be OK with lower gasoline prices boosting household spending power, supporting consumption elsewhere. The PCE deflator, the Fed's preferred inflation measure, will reflect the earlier flat CPI release. The University of Michigan Consumer sentiment release is a final reading but might be revised a tad higher given a further slide in gasoline prices.

More By This Author:

Impact Of China’s Drought Is Small Compared To Its Real Estate CrisisCould Double-Digit Inflation Be On The Cards For The Eurozone?

Hungarian Labor Market Situation Remains Pro-Inflationary For Now

Comments

Log in or sign up to join the conversation.