That’s from a Reuters report a few days ago. I think it’s important to (1) keep in mind what forecasters are saying, and (2) what GDP ex-military spending looks like.

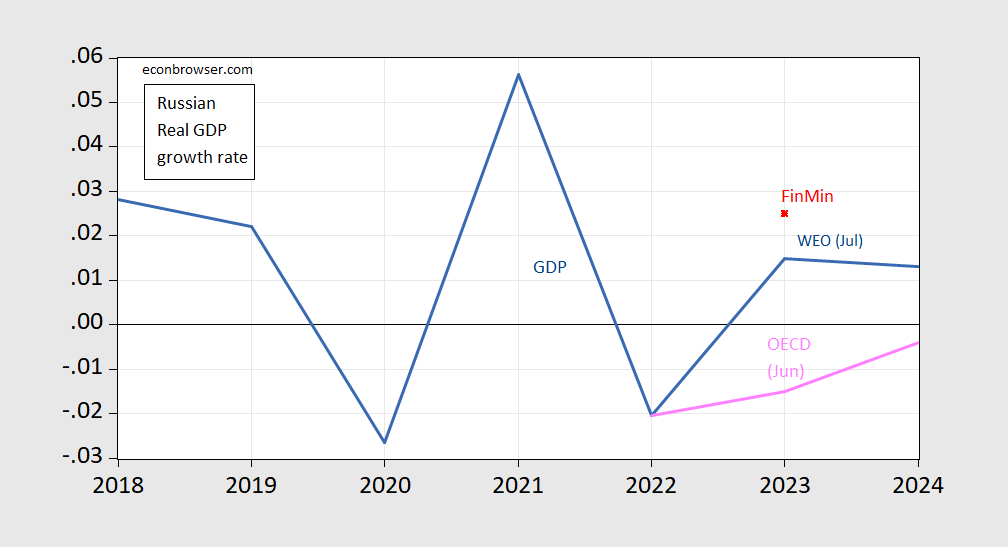

Blue line (pink line) in Figure 1 below shows the IMF July (OECD June) GDP forecasts.

Figure 1: Russian real GDP growth from IMF July WEO (blue), from OECD Economic Outlook (pink) and Russian Finance Minister Aug 2023 (red asterisk). Source: GDP from IMF WEO (April, July), OECD, Reuters.

The Finance Ministry estimate is at the high end of the range given by the Russian Central Bank (1.5-2.5%).

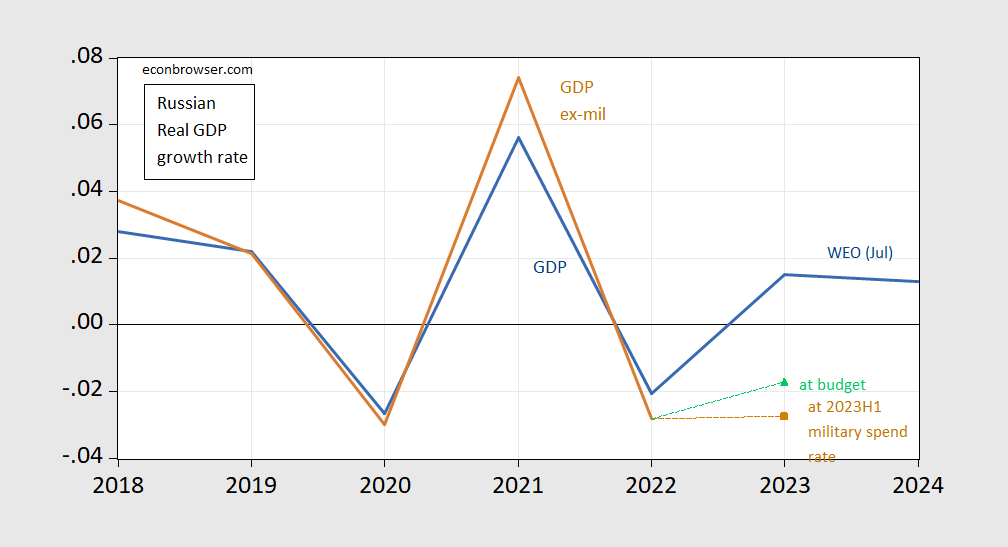

Recall that this is GDP growth overall, part of which is being kept from being more negative by elevated defense spending. The brown line shows the growth rate of ex-military spending (as estimated by SIPRI), working off of IMF WEO forecasts. Shift downward equivalently if using OECD forecasts.

Figure 2: Russian real GDP growth from IMF July WEO (blue), ex-military spending from SIPRI (tan), using 2023H1 spend rate (tan square), using 2023 budget as reported by Reuters (light green triangle). All calculations based on IMF WEO GDP. Source: GDP from IMF WEO (April, July), Reuters.

See the caveats to how I calculate GDP ex-military spending in this post. I assume SIPRI catches all defense/security related spending, which is not likely the case (one estimate is that it’s only 3/4). The other is I assume the deflator for defense expenditures is the same as that for nondefense GDP. Finally, this is “gross” domestic product, not “net”, insofar as the depreciation of defense capital (destroyed tanks, helicopters, self-propelled artillery, expended ammunition) is not included.

Holding constant the estimated defense spending levels, growth in GDP ex-military spending is probably negative, even with the FinMin’s higher GDP growth estimate.

More By This Author:

The Problems With China’s Economy…

The Atavistic Component Of Consumer Sentiment

Q3 GDP Now At 5.9% (SAAR)

Comments

Log in or sign up to join the conversation.