As the market widely expected, the FOMC left the Fed Funds rate unchanged. However, the statement summarizing the meeting now includes an economic growth warning- “uncertainty around the economic outlook has increased.” Moreover, they are reducing the amount of monthly QT. The roll-off of Treasury securities will fall to only $5 billion monthly, down from the current $25 billion pace. Agency and MBS roll-off will remain at $35 billion a month.

The Fed also released its quarterly Summary of Economic Projections (SEP). This table provides the economic outlook of the Fed members and can be a good indicator of the board members’ broad economic and inflation views. In this latest SEP, the FOMC reduced its median GDP forecast for 2025 from 2.1% to 1.7%. Furthermore, the FOMC increased their 2025 median PCE and Core PCE projections by 0.2% and 0.3%, respectively. Despite the higher inflation outlook, they remain in line with the Fed Funds futures market with expectations of between two and three 25bps rate cuts this year. However, the range of expectations is now 3.1% to 4.4%. Such is a broader band than 3.6% to 4.4% from the December projections. Given that Fed Funds are 4.50%, no members expect a rate increase. None of the longer-run forecasts changed. One member dissented from the decision to reduce QT.

The initial market reaction to the FOMC statement was that the Fed is shifting to a more dovish tone. The coming speeches from various members will provide more details on the rationale for reduced QT and cautious economic outlook.

Economy

(Click on image to enlarge)

Market Trading Update

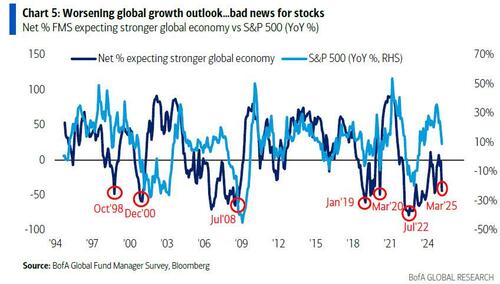

Yesterday, we discussed that while the economy is slowing down, recent data does not suggest a recession is imminent. However, the market has been pricing lower in anticipation of a slowdown in earnings, given the anticipation of a weakening global economy. After a brief uptick into expectations for stronger global growth, those expectations have declined toward 2020 lows.

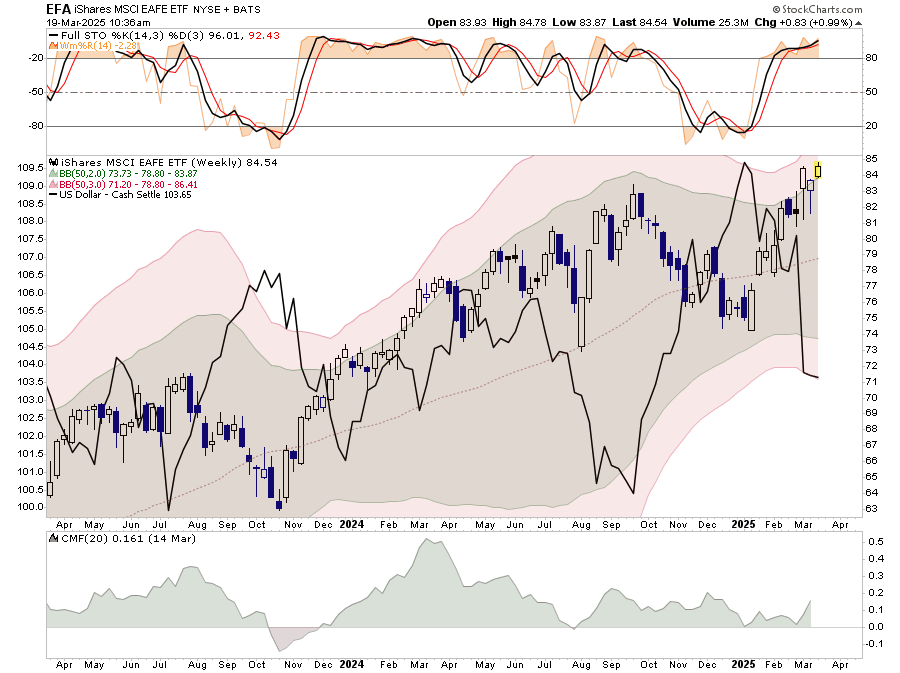

Since earnings growth comes from economic growth, slowing economic growth doesn’t bode well for stronger earnings or higher stock prices. One consideration for investors would be to rotate from extremely overbought markets to oversold ones. For example, international has had a nice run since the beginning of the year. However, global markets are very deviated from their longer-term means and overbought on multiple levels. One of the significant supports for that rally has been the selloff in the U.S. dollar. A reversal in the dollar, which is extremely oversold, will likely cause a reversion in the international market. Likewise, a reversal of the dollar will drag foreign inflows into U.S. stocks, providing a good rotational trading opportunity for investors.

(Click on image to enlarge)

We see this same rotational setup in the Simplevisor. Currently, Megacap growth, High Beta, and S&P 500 growth are extremely oversold, while International, Emerging, and Developed markets are very overbought. While these conditions can remain for some time, they do not last indefinitely. Eventually, the laggards will become leaders and vice versa.

(Click on image to enlarge)

As such, consider taking profits in winning sectors and opportunistically adding to out-of-favor sectors. Such tends to pay dividends more often than not, despite the current market narratives.

Trade accordingly.

Betting Markets Bet On An End To QT

Before the FOMC meeting, the betting markets, not derivatives or securities markets, were betting with 100% certainty that the Fed’s QT would end at the May meeting. We think ending QT will come sooner rather than later. Moreover, as we wrote in Never Let A Crisis Go To Waste, the dwindling RRP program informs us that excess liquidity is drying up. However, with the debt cap resolution, it’s a stretch to price-ending QT in May as a certainty.

If markets continue to weaken and economic data slow further, ending QT becomes more likely. However, neither of those two circumstances is guaranteed. It’s worth adding that even if the Fed ends QT, the odds of them shifting to QE in the near term are minimal. Jerome Powell made it clear in mid-February that they would not do QE until Fed Funds are down to 0%.

Growth To Value: Which Rotation Is Next?

Shifting investor preferences to large-cap value from large-cap growth and high beta provides an excellent example of sector and factor rotations. Investor rotations between sectors and factors are constantly occurring. Successfully navigating these rotations is one way to beat the market. This, of course, makes a big assumption that you can successfully gauge sector and factor rotations before most other investors.

This article highlights several SimpleVisor tools we use regularly to track sector and factor rotations. These models help us better forecast tomorrow’s possible rotations and try to stay a step ahead of the market.

(Click on image to enlarge)

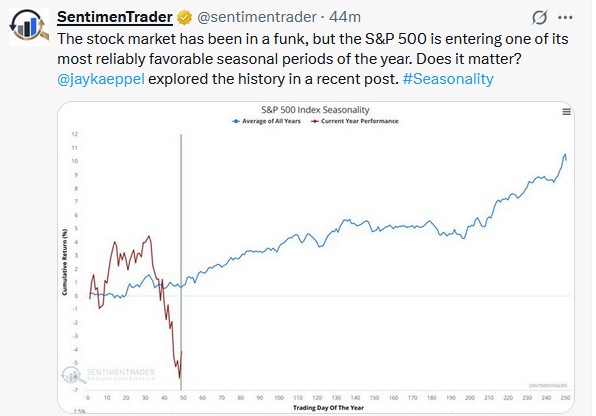

Tweet of the Day

More By This Author:

The Sentiment Bark Is Worse Than The Market’s Bite

Transportation Stocks Continue To Lead Markets Lower

Retail Investor Buys The Dip Despite Bearish Sentiment

Comments

Log in or sign up to join the conversation.