Image Source: Unsplash

Market Analysis:

Last year’s drought in Argentina & S Brazil, the Black Sea conflict reducing its oilseed trade, last spring’s wet US soil conditions curtailing plantings & the W Midwest drought combined to reduce the world’s protein supplies in 2022.

These smaller supplies and Argentina’s dryness impacting their seedings again this year have elevated the soy complex’s values entering the new year. These higher prices have limited our overseas demand, particularly in China which has had a very restrictive Covid policy until it was moderated 4-6 weeks ago. Strong US soybean crushing margins have been supportive to prices, but reduced US pork and poultry numbers being reported recently are a noted concern going into the final half of the crop year.

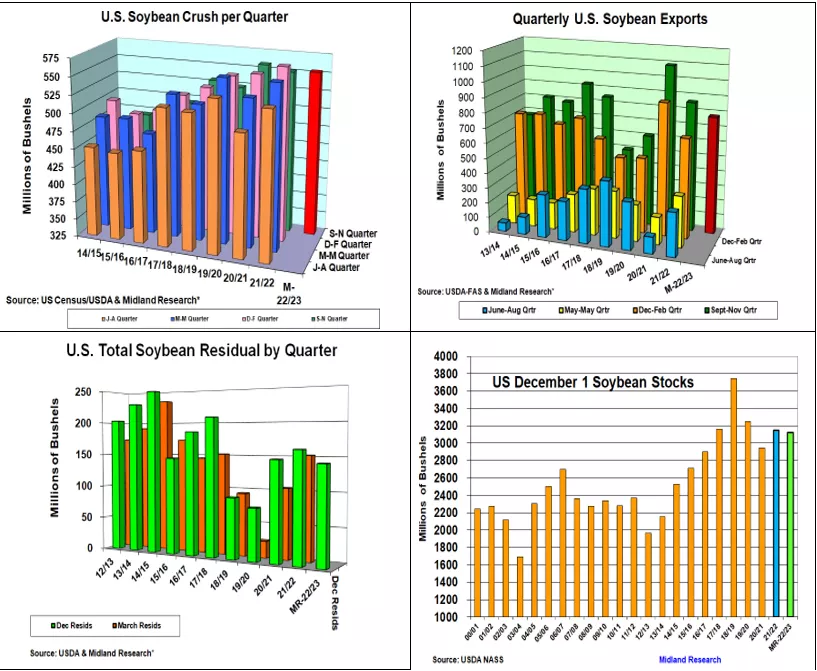

November’s slight 28,000 bu daily slowdown and 1 less processing day led to last month’s 500,000 bu shortfall in the US crush at 189.5 million bu vs the trade’s estimate. However, slightly higher Sept & Oct output advanced this year’s fall quarter processing rate to 554 million bu, up 2 million over 2021. Given the current strong crushing margins, the USDA isn’t likely to change its current record of 2,045 billion bu yearly domestic demand this month.

The combination of high old-crop prices, limited Chinese demand because of their restrictive covid policies, and a dry central US weather pattern curtailing the US Mississippi River barge shipping system lead to a sluggish initial 4-6 weeks in last fall’s exporting program. Overall, we anticipate 785 million bu were exported vs 861 million last year. After hefty Chinese purchases last month and current sales 63 million ahead of 2021’s pace, no downward adjustment in the US export demand of 2.045 billion bu is anticipated.

Given last fall’s moderation in exports & curtailed barge shipments because of low river levels, we expect a slight decline in soybeans’ seed & transit residual to 142 million vs 2021’s 161 million level. Utilizing our anticipated 22 million smaller final US bean crop, Dec 1 US stocks could be 3.12 billion bu; 32 million bu lower than last year because of a possible 125 million smaller beginning supplies.

What’s Ahead:

Despite last fall’s 74 million in reduced US demand, the USDA’s quarterly stocks will likely be modestly lower than in 2021 because of a smaller US crop. This means South America’s weather & China’s market actions will remain price factors heading into 2023. Hold 2022/23 crop sales at 65%, but be prepared to advance sales to 80% in the $15.75-95 March range & begin 2023 marketings at $14.40 for 15%.

More By This Author:

Pre-January Snapshot: 2022 US Corn & Soybean Output

December US/World S&D Reports - Ending Stocks Had No To Little Changes This Month

US Dec S&Ds Don’t Change Much, But Slow Exports May Up Corn Stocks

Comments

Log in or sign up to join the conversation.