Not surprisingly, the Fed cut rates by 25 basis points at yesterday’s meeting. With the cut, the Fed Funds rate sits at 4.00-4.25%. While the market was nearly certain of a 25bps cut, it is less clear about what the road ahead holds for Fed policy. To help us start thinking about how policy may change at the upcoming meetings, we share a few comments from yesterday’s FOMC meeting.

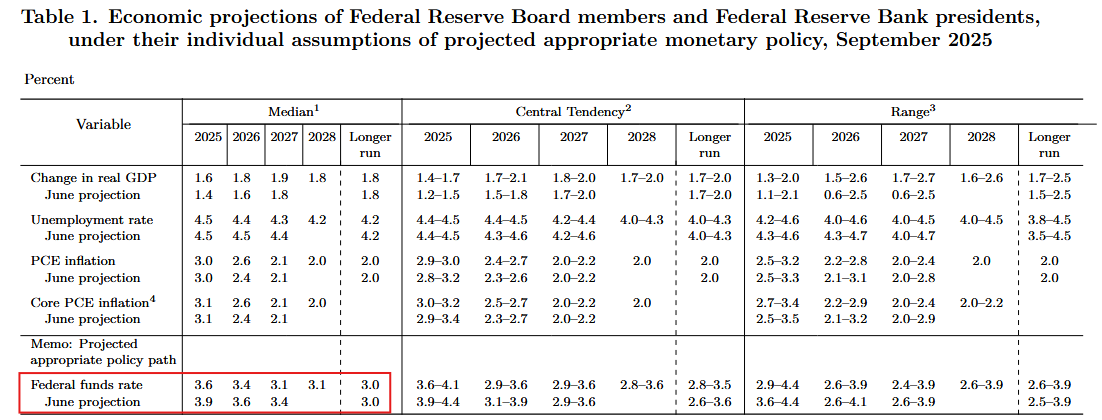

- The Fed economic projections, shown below, quantify the changes in the forecasts of FOMC members over the last three months. Their expectation for real GDP increased from 1.4% to 1.6%. Despite recent weakness in employment data and an uptick in CPI, their forecasts for unemployment and PCE inflation are unchanged. Its Fed Funds projections fell from 3.9% to 3.6%, reflecting the 25bps rate cut.

- Every member voted for a 25-basis-point cut, except the newest member, Stephen Miran. He dissented and voted for 50 bps. Based on the dot plots, he believes Fed Funds should be 2.875% by year-end.

- The FOMC statement alludes to recent weakness in the labor markets but notes that “inflation has moved up and remains somewhat elevated.” They claim that “downside risks to employment have risen,” which explains why they all voted to cut rates.

- “Since April, the risks of higher and more persistent inflation have become a little less.” Powell’s less troubling inflation outlook, coupled with worsening employment data, makes him more comfortable cutting rates.

- Powell anticipates that increases in goods prices will be “one-time” in nature, but will closely follow. “The case for a persistent outbreak in inflation is less.”

- He noted on numerous occasions the unique tension between its employment and inflation mandates and how it complicates its forecasts for the Fed Funds rate.

- Powell deems Fed policy is “more moderate” but still restrictive.

- The Fed was expecting the employment revisions, but is concerned about the low response rates in the BLS survey.

- The Fed believes that the company’s importing goods are largely paying tariffs, not consumers or the exporting countries.

- “It’s not obvious what we need to do.” Based on that comment and other similar comments, the Fed is not confident in answering our question of what comes next.

(Click on image to enlarge)

What To Watch Today

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

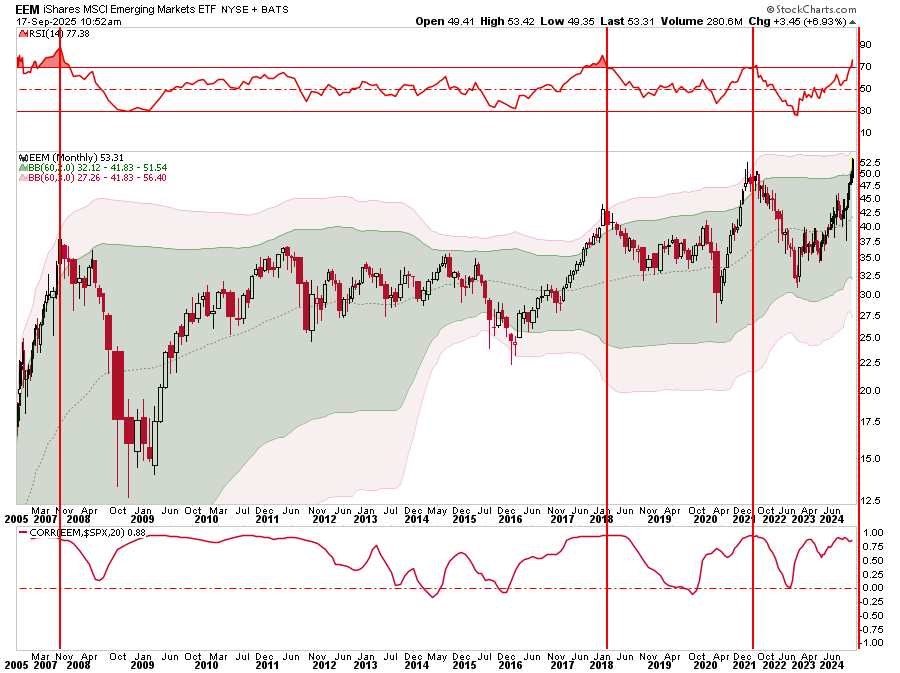

Yesterday, we discussed the breadth of the market and the divergence between market and equal-cap weighted indexes. One other note discussed yesterday was the fact that many markets are now becoming correlated to the stock market, ranging from gold to emerging markets. We are seeing a sharp increase in the money flows into assets across various markets. For example, emerging markets have become parabolic recently as Chinese technology stocks soar. However, the reversion was not kind to investors in the three previous instances where emerging markets deviated from their 5-year moving average and were highly correlated to the S&P 500.

(Click on image to enlarge)

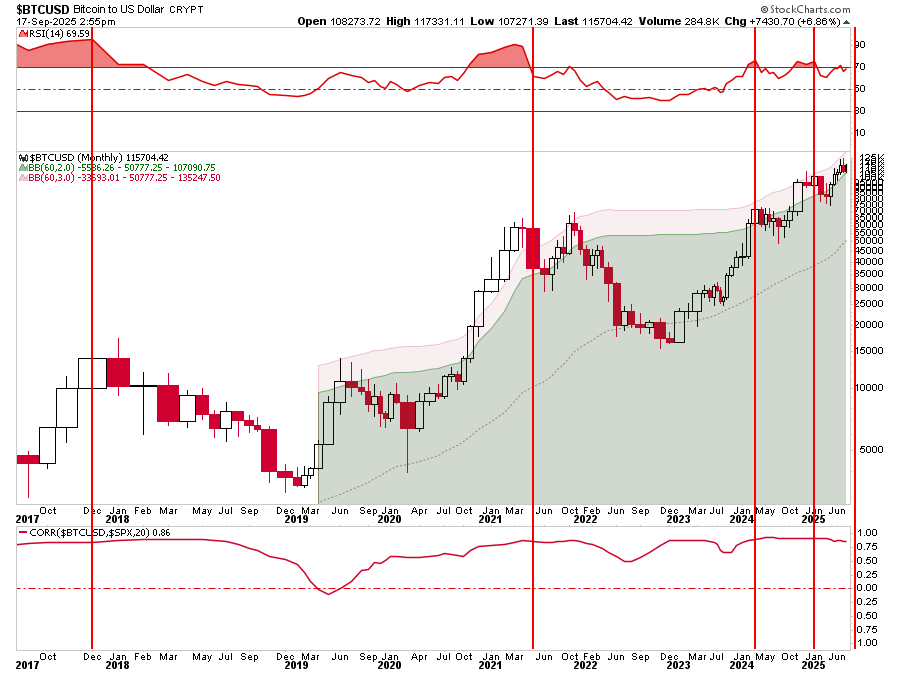

The same exuberance is seen in Bitcoin. The correlation to the S&P 500 and risk assets has always been high, but the current deviation from the 5-year moving average is certainly noteworthy. Previous extensions were precursors to a corrective move, coinciding with a correction in the S&P 500 index.

(Click on image to enlarge)

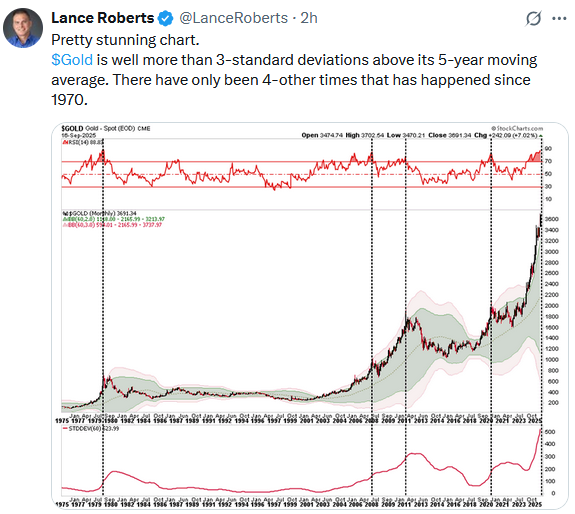

Gold is also massively extended, and its correlation to stocks is beginning to approach one. The excessive overbought condition on a monthly basis and deviation from the 5-year moving average have previously coincided with corrections of 20-50%.

(Click on image to enlarge)

Of course, the momentum chase is evident in the stock market, as well as in gold, bitcoin, and emerging markets.

(Click on image to enlarge)

None of this should be surprising. There is always a “narrative” as to why “this time is different,” yet it never is. The reality is that the technical deviations will eventually be corrected for some reason that the most bullish of analysts can’t predict. But it happens…every time. As Thomas Thorton recently noted, the warning signals are piling up.

- DeMark exhaustion sell signals are lighting up like a Christmas tree.

- Bullish sentiment is extreme while market internals are diverging lower.

- Every valuation metric is historically in the 100th percentile overbought.

- Retail traders and CTA trend-following funds are all-in, betting the house.

- Speculation is running wild – think late-night Vegas tables.

- Everyone’s convinced the Fed will cut rates and save the day… while unemployment rises and inflation still lurks like an uninvited guest.

As the legendary trader, Art Cashin, might say, “The markets look like they’ve been at the punch bowl a bit too long.”

Risk management is key in a late-stage advance as we are in now. Trade accordingly.

BBB and AA Corporate Spreads Show Investors Have Extreme Confidence

At first glance, the red-highlighted corporate spreads, courtesy SimpleVisor, reading 0.00% appear to be an error. It’s not! Corporate bond yield spreads versus US Treasury yields for BBB and A-rated bonds are at their tightest levels in the last 20 years. In other words, corporate bond investors are willing to accept a record-low premium to assume default risk.

The data below makes it clear that corporate bond investors are largely unconcerned about an economic slowdown or recession, which could lead to downgrades and defaults. Corporate bond yield spreads parallel equity sentiment. While corporate spreads are incredibly tight, the stock market is at an all-time high. Both markets seem to be ignoring weakening economic data. Clearly, both the bond and stock markets indicate that investors are highly confident that Fed rate cuts will stave off a recession, should one occur.

(Click on image to enlarge)

Job Security Worries Should Worry The Fed

The latest University of Michigan Consumer Sentiment survey sits near 50-year lows. Surprisingly, it’s below the trough reached during the 2008 financial crisis and just above the pandemic lows. The Conference Board’s Consumer Confidence Index is not as dire, but it too is not far from the Pandemic lows. While political affiliations are certainly influencing the results more than usual, we must still acknowledge that low confidence, regardless of the reason, negatively affects personal consumption. Moreover, personal consumption accounts for about two-thirds of GDP.

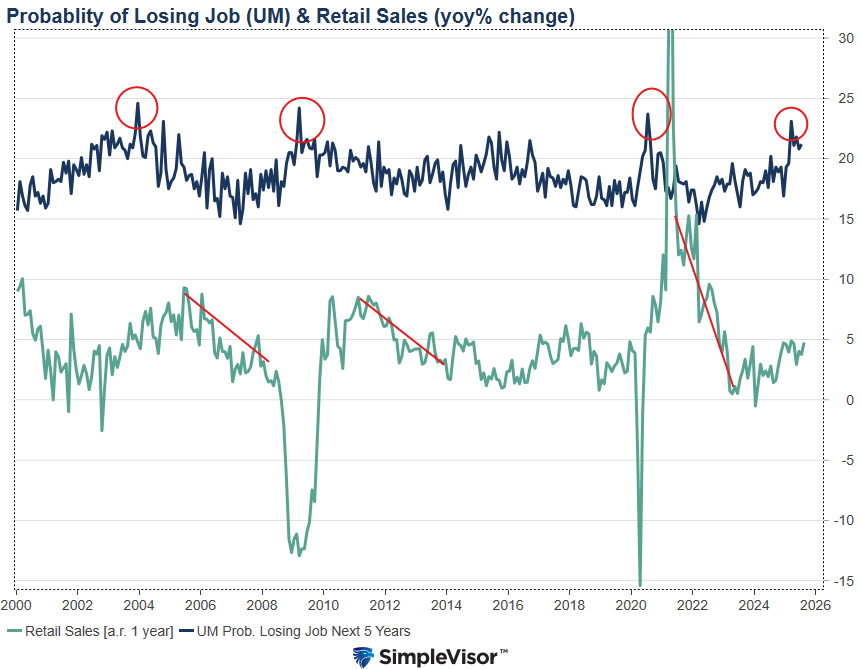

Today, we focus on confidence in one’s employment as it is probably the most critical subcomponent of confidence in relation to consumption. The first graph below shows that the percentage of people expecting higher unemployment in a year is near a 30-year high. Similarly, those expecting to lose their job in the next five years are also very high. In the second graph, we compare the percentage of those expecting to lose their job with retail sales. As we highlight, following each peak, retail sales trend downward. Given that the current level of retail sales is decently lower than the prior peaks, a similar downtrend could push retail sales negative, something that typically coincides with a recession.

Tweet of the Day

More By This Author:

Semiannual Reporting Requirements Are Overhyped

Trump’s BLS Reform Faces Steep Obstacles

Invest Or Index – Exploring 5-Different Strategies

Comments

Log in or sign up to join the conversation.