The Energy Sector Is Now The Way To Go

First, some definitions...

When analysts say or websites report “oil prices are falling,” that does not necessarily mean oil and gas firms will all fall in sync. These pundits are typically looking at the price of WTI Futures for the Front Month. What does this mean? Is it significant?

Let’s take a look at how the future of energy companies may be decided and whether “WTI” is a realistic benchmark for investing:

WTI Crude Oil

West Texas Intermediate (WTI) crude oil also is known as Texas light sweet crude. It refers to a particularly favorable grade of oil that has both a relatively low density and a low sulfur content. Because of these qualities, WTI is quite well suited for refining gasoline and other much-in-demand consumer and industrial uses. WTI is primarily refined in the US Midwest and Gulf Coast.

The Front Month and Per Barrel

As you might expect, the Front Month means the next calendar month for delivery of a product. In the case of oil the price is x dollars for a barrel of unrefined product.

Is This the Global Price For Oil and Gas?

No. First of all, natural gas and oil do not move in lockstep. They have both fallen from their highs recently, but that will not always happen. Even when it does happen it will not always happen for the same duration or at the same pace. Each marches to its own drummer.

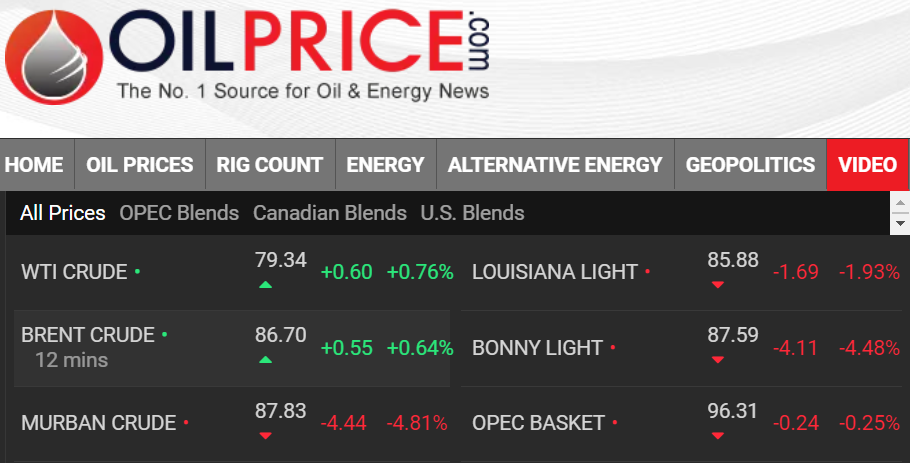

Even within the oil universe, a cursory visit to www.oilprice.com, which I try to visit daily when not traveling, will show there are six major types of oil, all with different prices based upon their density, sulfur content, and more.

(Click on image to enlarge)

oilprice.com

What Determines Oil Prices?

Crude oil is a commodity. It's also a product that trades based on many factors, current emotion being one of them. It's also influenced by politics, as when President Biden accused the industry of making windfall profits at the expense of American consumers.

Some of those profits ensued, of course, from the administration’s own actions to limit supply. On inauguration day, one of the first executive orders issued was to shut down ongoing pipeline construction and remove acreage for drilling on federal lands.

Less supply + constant or increased demand = higher prices.

Other factors influencing the price of oil and gas include higher or lower production costs, the value of the US dollar, sanctions, the degree of market speculation, and global economic conditions. Even the weather plays a role. Hotter weather means more demand for air conditioning in businesses, manufacturing, homes and vehicles, especially in summertime. Colder weather means more demand for heating in all these areas.

What Comes Next?

We have reached the end of summer driving season in the US and air conditioning is being used less and less. The from-the-2020-lows consumer spending binge that made for more shipping, more rail, more trucks on the road, etc., has now begun to abate. It's only natural that we're now in a phase of needing less oil and natural gas.

(I use the terms “natural gas” and “gas” interchangeably. For the stuff that powers cars and trucks and other vehicles, I will use “gasoline,” “diesel,” “kerosene” or whatever the distillate is.)

I believe this decline in oil – and gas – pricing is a temporary occurrence.

Oil and especially natural gas will see more demand in the coming autumn weeks and winter months. I have been buying shares of oil and gas companies in recent weeks as their prices have declined. Based upon last week’s action, do I wish I would have waited? Of course. But I cannot invest, or advise anyone else to invest, for what happens today or this week.

I'm looking over this valley to the next climb in energy prices.

It's important to note that, while most investors panic and emotionally sell when they see the Front Month WTI futures fall, what happens the very next month’s (or months’) futures trading is not nearly as important to oil and gas companies as what might happen in three months, six months, a year and five years. Their capital expenditures budgets and their decisions to drill or to pump slowly or full-out are where they make their money and, by proxy, where you make your money via your share prices.

At this point, Europe has enough gas to handle demand for the next month or two. Beyond that, I see these nations being starved for natural gas to create electricity. A cold winter in Russia, along with Putin’s desire to punish European nations for their support for Ukraine, will mean these countries will be desperate for gas to power their electricity grids.

Besides Russia, Europe does receive gas from Africa, from Azerbaijan, and the Middle East. It also has some providers, especially the UK and Norway, that have existing pipelines to the rest of Europe – though not in the quantity that will be needed. In addition, all these providers have other clients as well. The amount flowing through these pipelines will not be able to avert disaster in one of Europe’s particularly cold winter years.

Some shortsighted nations in Europe shut down their clean and readily-available-for-power nuclear power generation plants. They also eschewed contracts from the above in favor of Russia.

I believe Canada and the United States will do their best to step in and replace this deficit, but these two do not currently have the ability to significantly compensate a likely shortfall in the availability of natural gas to Europe.

Many nations with at least some profitable natural gas fields are building or have built liquefaction plants and terminals. These plants compress natural gas from a gaseous state to a liquid. This Liquified Natural Gas - LNG - is compressed as much as 600 times, then transported across the globe everywhere a pipeline would be impossible to place. Once these purpose-built tankers arrive with their load of LNG, the receiving nations must have regasification plants to convert the gas back to a gaseous form to be distributed via pipelines. The United States is the world’s largest exporter of LNG – and growing.

Less gas than needed + more demand than currently = higher prices for gas.

Russian oil is currently being sold around the world, primarily to its two largest customers, India and China, at a hefty discount. Going forward, if Russia saves its oil in winter for its antiquated oil-burning manufacturing base as well as for all those military vehicles it keeps bringing out of mothballs and sending to Ukraine, I see the price of oil rising, as well.

The US is the world’s biggest oil producer, followed by Russia (with much-antiquated equipment only kept going by pre-sanction Western technology,) Saudi Arabia, and Canada. But the US uses much of the oil it produces. In addition, US energy firms have been hamstrung by various federal government mandates in the past couple of years.

Since much of the Middle East has oil and gas as their only real exports to keep their autocracies in power, I also can see a floor under both commodities. These nations may look as if they are in the catbird seat when it comes to energy export sales, but they walk a thin line between keeping restive citizens in line by ensuring a steady, rather than an erratic or unstable, flow of income.

I foresee a willingness among the Middle East and other OPEC nations to lower production markedly in order to keep the price of oil and gas from declining much further below current pricing. Better to keep the money flowing in and sell less product. After all, oil and gas in the ground is a better piggy bank than many currencies they would receive in exchange right now. I don’t know where this floor is right now, but I believe it's near.

Less supply + more demand = higher prices.

Summing up my case for oil and gas, I believe…

* Autumn is here, winter is coming. Food distribution via transportation (two-thirds of all petroleum consumption in the US goes to transportation,) residential and business heating, and electricity will be rising very soon and very steadily.

* Russian gas to Europe will be curtailed even further in a typical Russian winter. Russian oil will be hoarded at home for the same reason. There will be less available globally.

* The OPEC nations mostly have little to offer the world except oil and gas. I believe they will curtail production rather than accept lower prices.

* Less supply + increased demand = higher prices.

What could render my analysis moot? If the entire world entered a deep and lasting recession where very few people fly for business or pleasure, cruising passengers stop cruising, most people no longer take road trips, manufacturing declines significantly because very few are buying manufactured products, and truck and rail delivery are severely diminished.

What I'm Buying

I'm buying energy across the board. You can easily review my previous purchases in this area so I will list only two that I have just added - one company and one ETF.

I'm a particular fan of natural gas at this point. The price on the futures market for October has fallen by one-third in just the past 30 days.

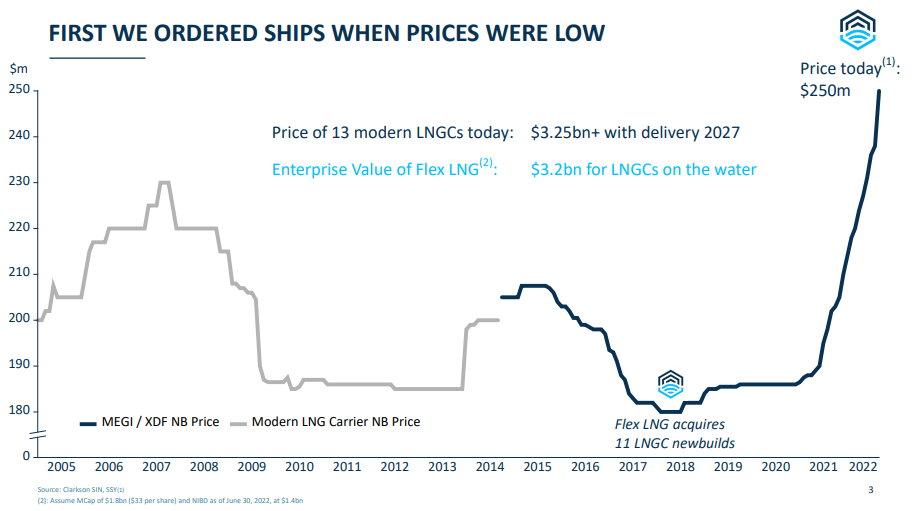

The company I just added to is based in Norway but traded in significant volume on the New York Stock Exchange. FLEX LNG (FLNG) is nominally headquartered in Bermuda (those darned Norwegian taxes!) and is a global LNGC (LNG Carrier.) The global integrated oil companies like Exxon (XOM), Chevron (CVX), Shell (SHEL), Total (TTE) (TOT), and BP (BP) are the biggest players in LNGCs and the biggest drivers of newbuilds. But FLEX is one of the top independents and a very special company.

FLEX just did an updated presentation at a global brokerage energy conference. I will let their words speak for themselves…

(Click on image to enlarge)

FLEX presentation

2018 was clearly the best time to buy in many years.

(Click on image to enlarge)

FLEX presentation

By “fixed,” FLEX means fixed-price contracts. All vessels but one are now on fixed contracts. According to Øystein Kalleklev, CEO of Flex LNG Management AS, "After these new contracts, our firm minimum backlog is 54 years with another 28 years of possible extension options."

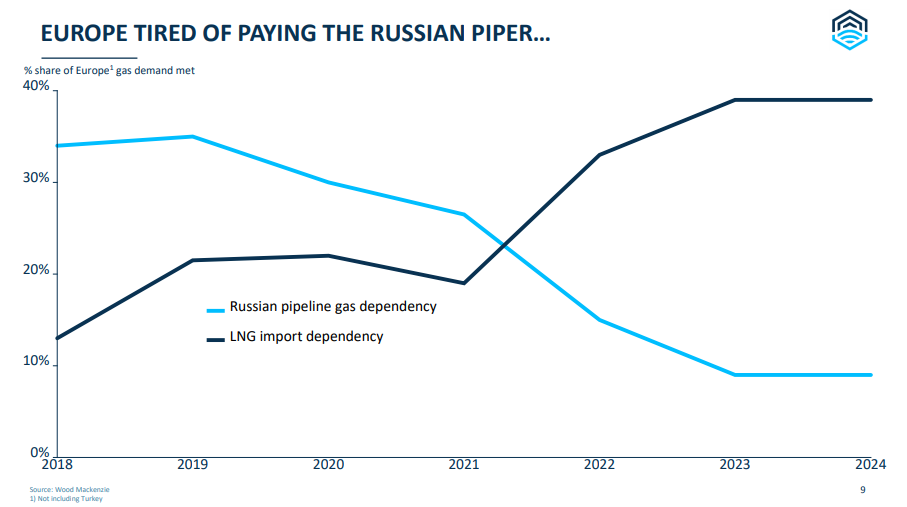

(Click on image to enlarge)

FLEX presentation

From a purely geopolitical viewpoint, this increases earnings for the US, Canada, Norway, and the big internationals in democratic free-market nations. It also decreases earnings in the totalitarian government-owned production and distribution economy of Russia.

(Click on image to enlarge)

FLEX presentation

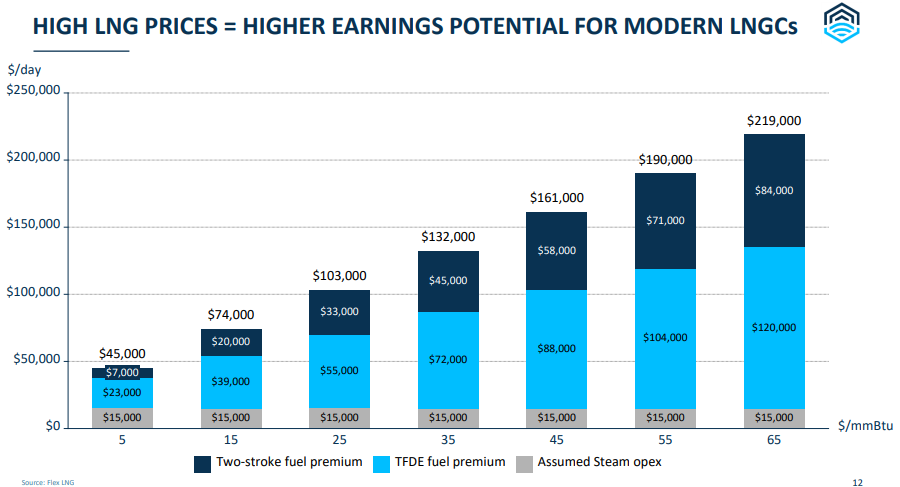

FLEX’s average fleet age is less than three years! One of the most modern in the business.

(Click on image to enlarge)

FLEX presentation

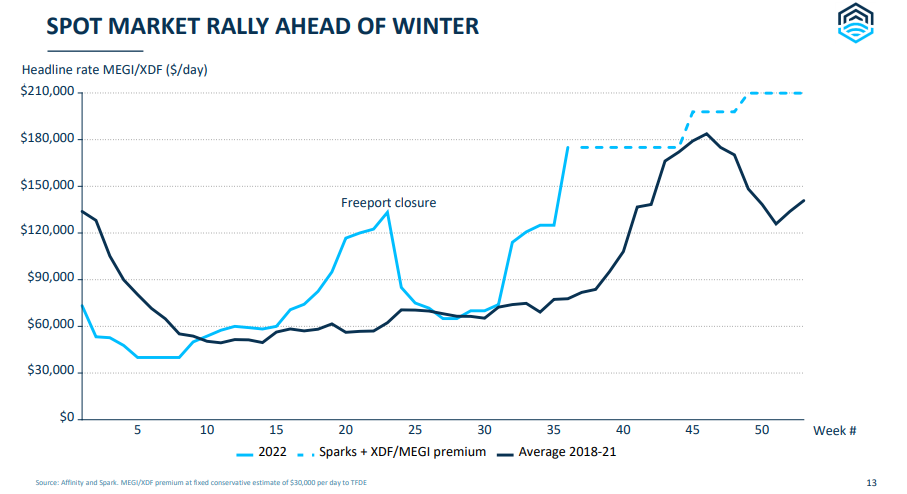

To my earlier point, “winter is coming.” Note the trend of seasonal pricing.

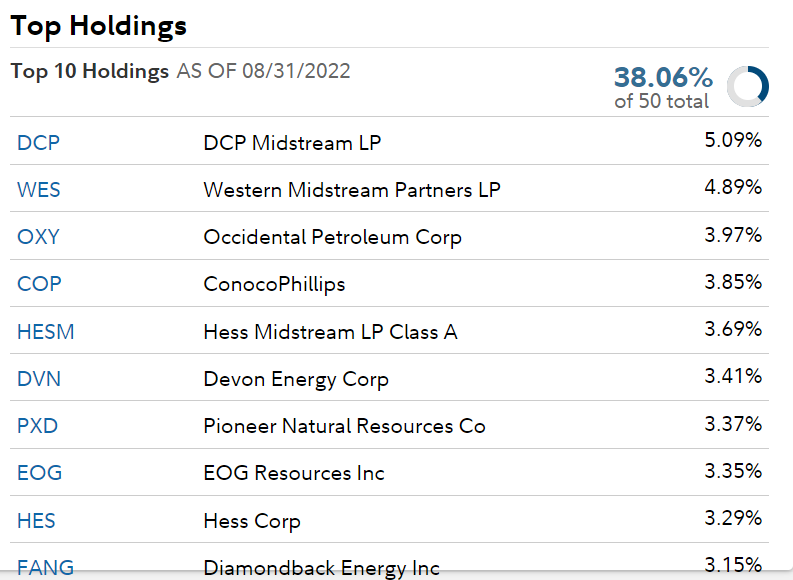

My ETF choice is the First Trust Natural Gas ETF (FCG). FCG’s website uses the usual blah-blah-blah mandated by the SEC to describe itself: “The fund invests in public equity markets of the United States. It invests in stocks of companies and MLPs operating across energy, oil, gas and consumable fuels, oil and gas exploration and production, oil and gas exploration services, oil and gas production sectors. It invests in growth and value stocks of companies across diversified market capitalization.”

(Click on image to enlarge)

Seeking Alpha

The point to remember is that this is primarily a "natural gas" company fund, as demonstrated by its holdings. Since natural gas is still mostly delivered by pipeline, you will note a number of midstream companies. Many are LPs. However, this ETF provides a "no K1" dividend flow (currently 2.9%.) Its top holdings are:

Fidelity.com

My review of all 50 holdings shows zero LNG companies. There's no overlap between FLEX and FCG.

FCG, instead, primarily buys drillers, producers, and transporters of natural gas. The ETF is comprised mostly of large cap and mid cap firms, though it has a decent mix of all. Mid caps are just under 50%, so there's a lot of flexibility here – and a lot of smaller-than-giant firms that have fallen enough to make my decision to buy additional FCG shares very timely.

I have owned both FLEX and FCG at slightly higher prices. I have now averaged my cost basis lower and plan to continue to do so. I see the current energy malaise as an interruption in the resurgence of the need for oil and gas, not its death knell.

More By This Author:

Tesla And Volkswagen: Report From A Country With 64% BEV Adoption

The Real Story On Inflation: How It Affects Your Portfolio

Mercer International: This 'Strong Paper' Stock Is On A Roll

Disclosure: I/we have a beneficial long position in the shares of FCG, FLNG either through stock ownership, options, or other derivatives.

Disclaimer: I do not know your personal financial ...

more