Some Thoughts On Gold & Idaho Strategic Resources

Image Source: Unsplash

I started getting very bullish on gold in November of 2023. I pitched my gold predictions and my favorite gold producer, Idaho Strategic Resources (IDR), to my readers. You can read the time-stamped report here.

Since then:

- Gold has increased by ~$200/oz

- Idaho Strategic is up ~34%

Is it me? Or did gold go from $1,650 to $2,060 without anyone noticing? Sure, there are gold bugs saying, “I told you so.” But has the real money even found its way to the table yet? No.

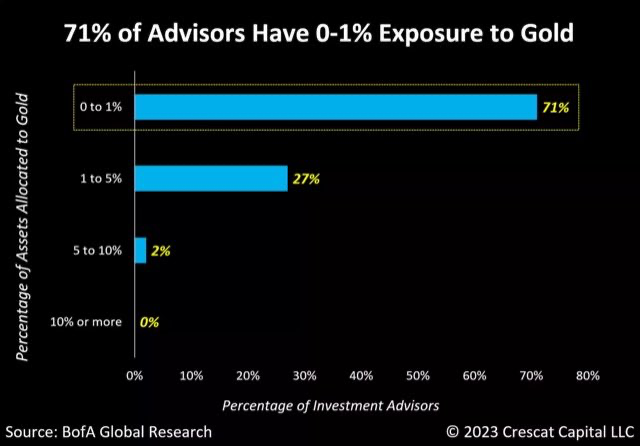

I saw a chart this week illustrating that 71% of financial advisors have 0-1% gold exposure (could be gold instruments like GLD, GDX, GDXJ, etc.).

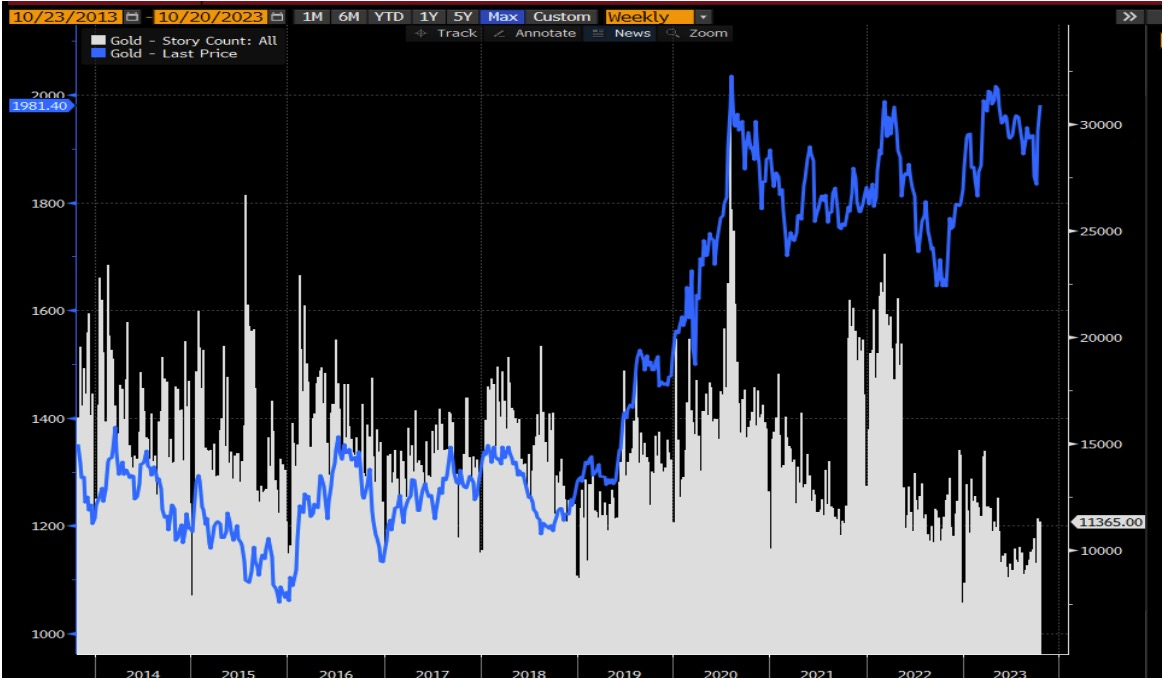

And a month ago, I tweeted about the inverse relationship between the price of gold and the number of gold-related news stories (see below, with a tip of the hat to Kuppy).

(Click on image to enlarge)

In a follow-up tweet I said, “There’s a ton of money to be made from executing the following formula: 1) finding high relative strength price action combined with 2) total investor apathy." Gold fits that formula.

Check out the gold chart provided below. I like monthly charts because they show long-term trends. There have been three substantial breakout trades seen in gold since 2008:

- Inverse H&S breakout in September/October 2009

- Inverse H&S breakout in July/August 2019

And the third one is happening now, with November likely printing a breakout bar from a three and a half year rectangle (see below).

(Click on image to enlarge)

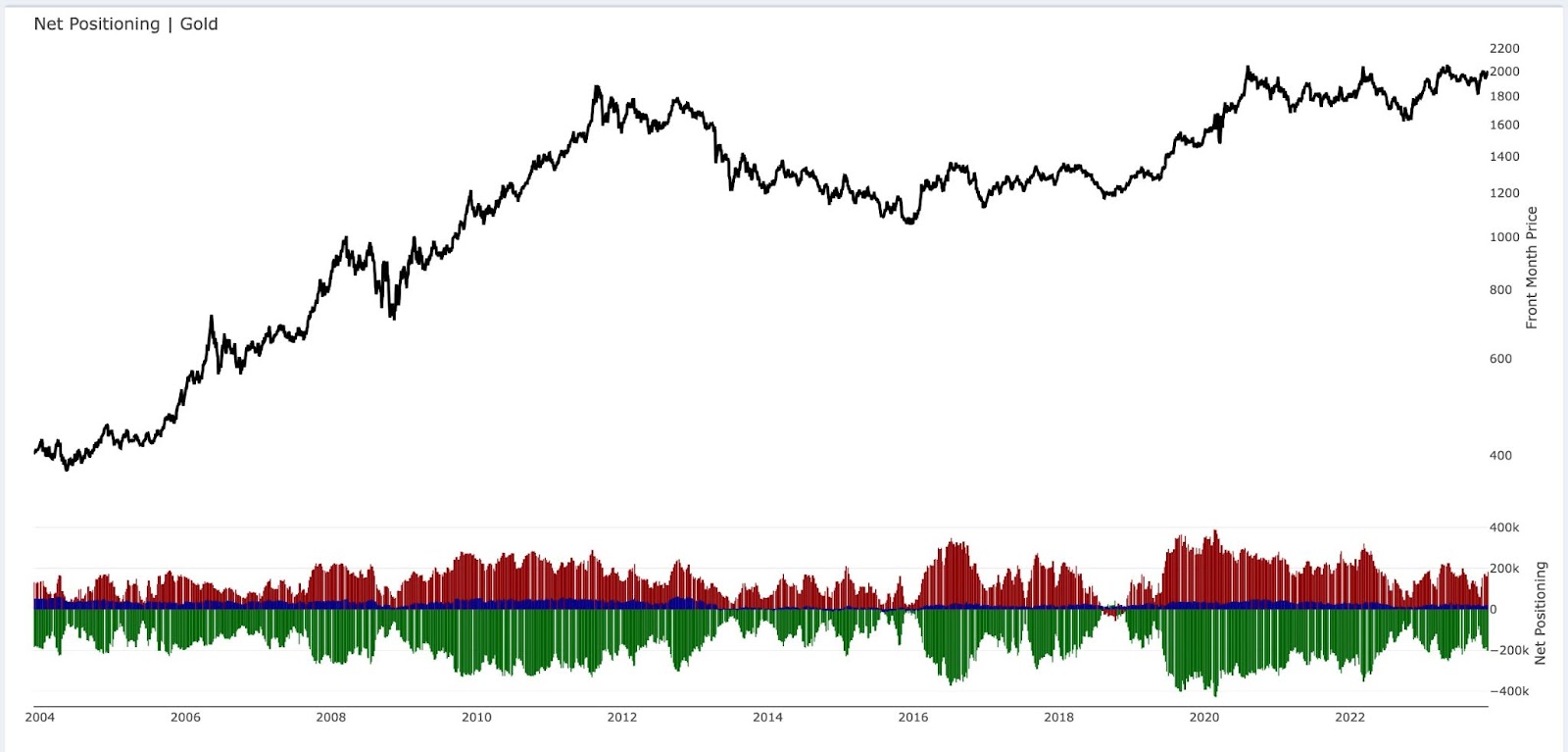

The measured move for this breakout is $2,362/oz. Here’s the thing, sentiment and positioning aren’t that overstretched. Let’s start with positioning.

(Click on image to enlarge)

Large speculators are long, but not that long relative to history (see August 2019 and February 2020). Small speculators, however, are only 5% long, which most recently marked the bottom around November 2022.

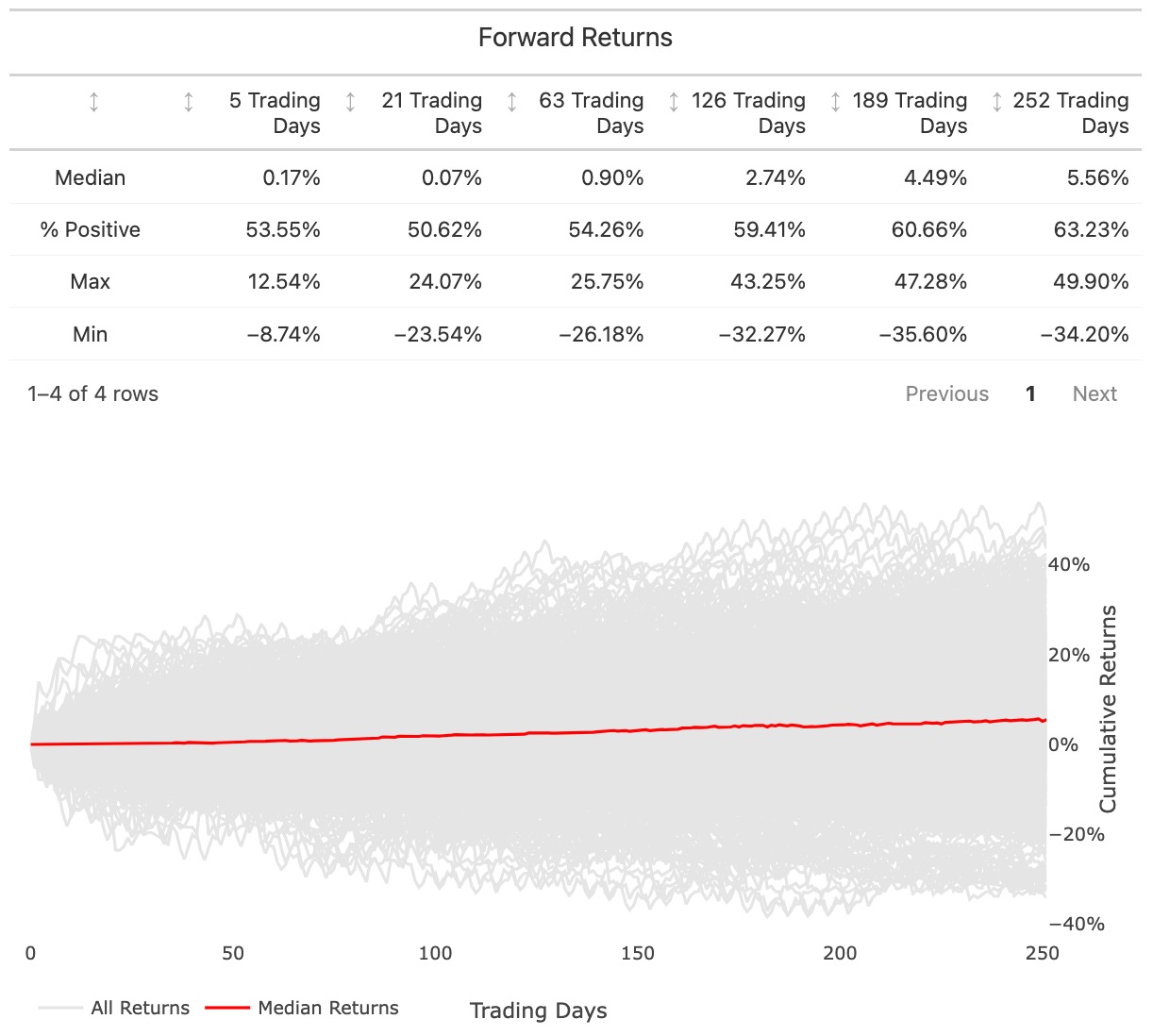

(Click on image to enlarge)

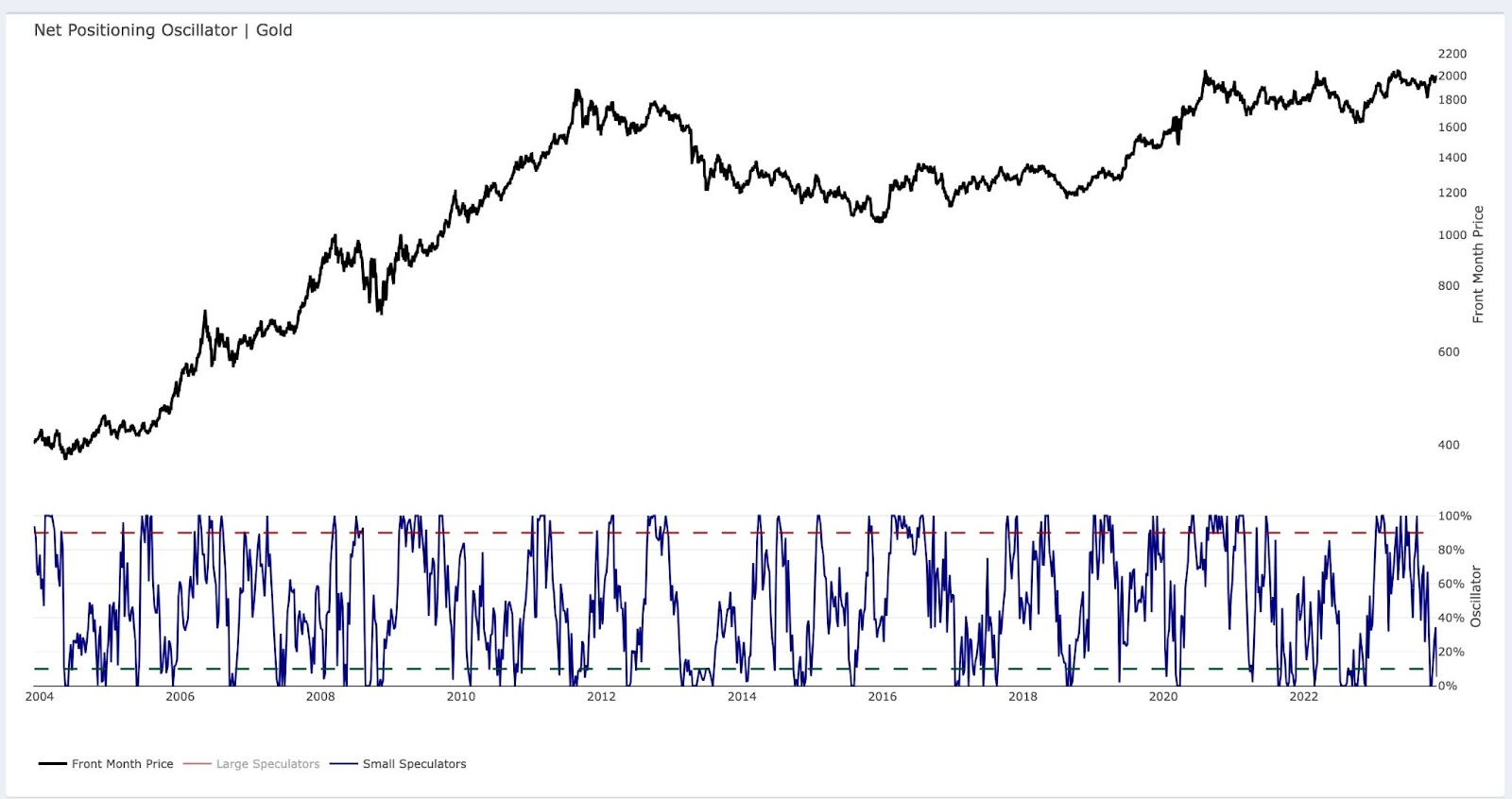

Using our HUD Backtester tool, we can see that forward returns are historically good whenever small speculator positioning is in the 10th percentile. Average 252-day returns are +5.56% with a 63% positive expectancy (see below).

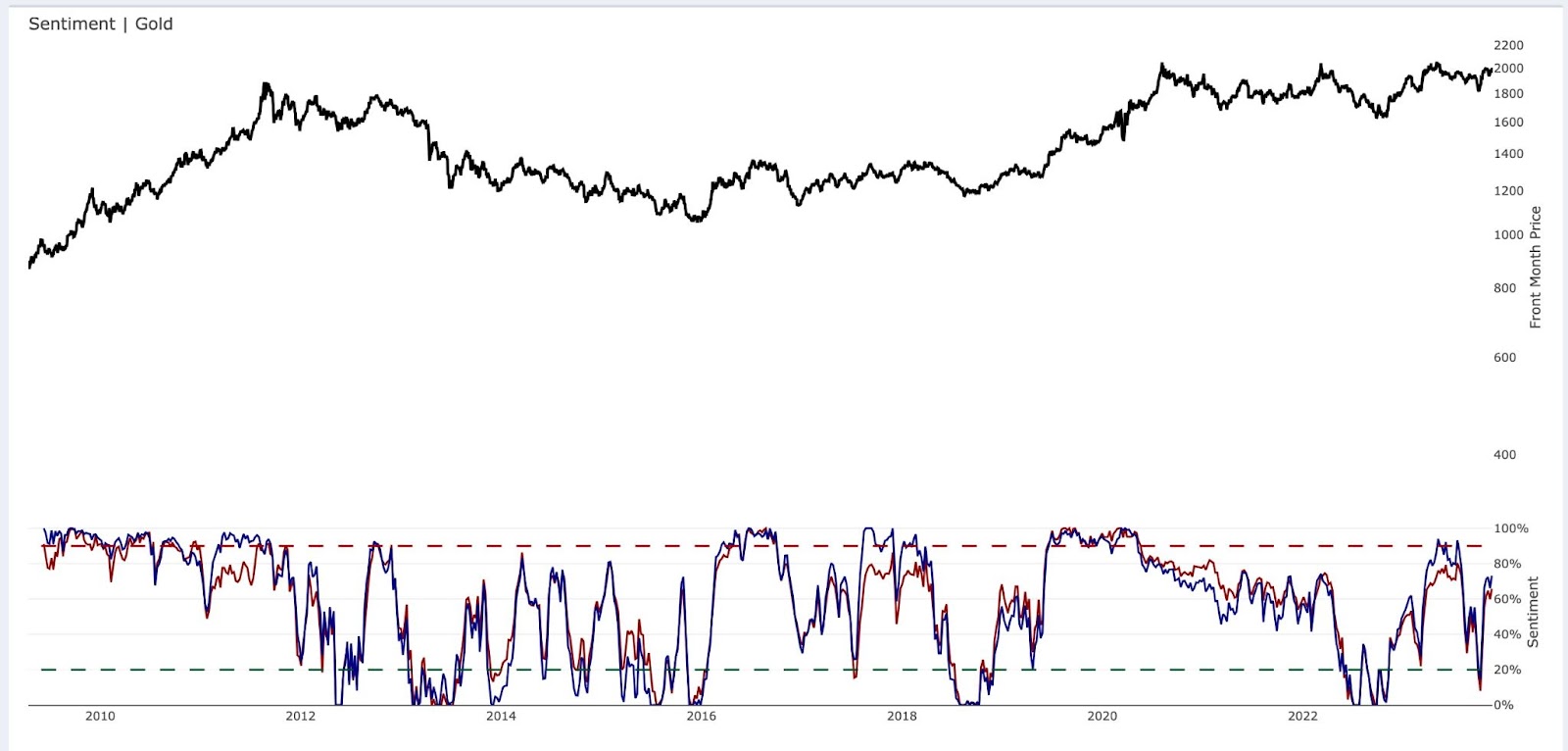

Then there’s sentiment. Which, at 65-70%, doesn’t signal overbought conditions and pairs well with the charts above that highlight general investor apathy.

(Click on image to enlarge)

And despite breaking out this month, gold is still around one standard deviation above its 200-day moving average. In other words, there’s still a lot of room for gold to run.

(Click on image to enlarge)

So, we’ve got a compelling sentiment, positioning, and technical case for higher gold prices over the next 12-18 months. What’s the best way to play it? Traditionally, you may take a "you only live once" risk with a small portion of your account on a basket of junior miners. Junior miners, of course, have the most leverage/torque to higher commodity prices. But they also incur the most risk.

I’ve written about this before with uranium. Junior miners face myriad risks, including geopolitics, fundraising/financing, lower grades, constant share dilution, increasing AISCs, etc.

I’ve also written about how much I like Idaho Strategic Resources for the opposite reasons. Idaho Strategic is a profitable, founder-led gold mining company based in mining-friendly Idaho. Here’s how I explained the company in my June 2023 write-up:

“IDR is the opposite of almost every mining stock I’ve researched. They prefer to hide under the radar. They avoid mining conferences. They don’t overpromote and promise five billion production ounces. Instead, they show up daily without fanfare and execute their business plan.

"Oh, and they only have 12M shares outstanding.”

The company recently updated its investor deck and did a business deep dive podcast with MicroCapClub founder (and friend), Ian Cassel.

With gold approaching $2,100/oz, I wanted to update my thoughts on the company and provide a bull case valuation thesis on Idaho Strategic's gold production business. I also want to explore the company’s Rare Earth Element (REE) package and value more deeply.

Current AISCs include REE Exploration

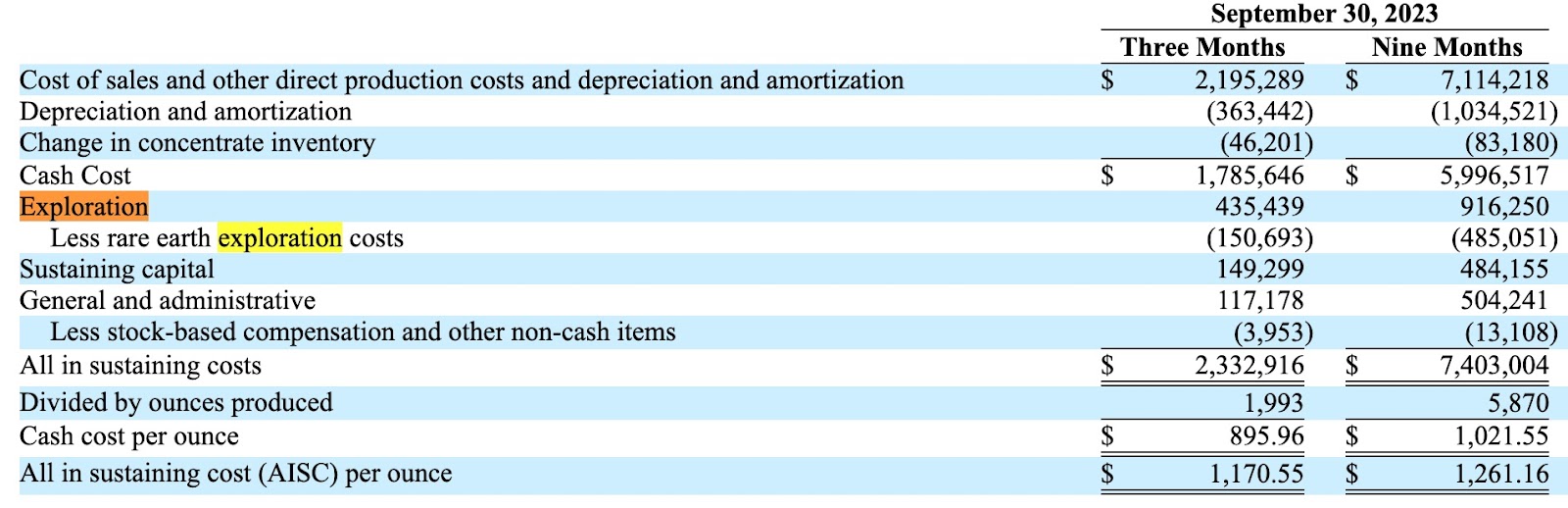

Idaho Strategic adds its REE exploration costs into its gold production AISCs. So when it says its gold production AISCs are ~$1,300/oz, that number includes whatever it spends exploring the REE land package. The most recent 10-Q shows that Idaho Strategic used 52% of its exploration budget on REEs (see below).

We can recreate the company’s gold-only AISCs by removing the $485,000 in REE expense. That gets us AISC of $6.92 million or ~$1,178/oz versus the reported $1,261.

(Click on image to enlarge)

Thinking About Valuation (Again)

I want to revisit my initial valuation case with gold firmly above $2,000:

“IDR can reach 12,000oz by the end of 2025, well within its target growth rate. Assuming a $2,000 gold price and $1,300 AISCs, IDR would generate $8.4M in cash flow and trade at ~7x.

"So you’re paying ~7x 2025 gold production cash flow and getting a massive rare earth element deposit for free.”

Let’s assume Idaho Strategic reaches 12,500/oz per year over the next few years, with AISCs around $1,250 net of any REE exploration costs. Now here’s the fun part. Suppose gold hits its measured move target of $2,362/oz.

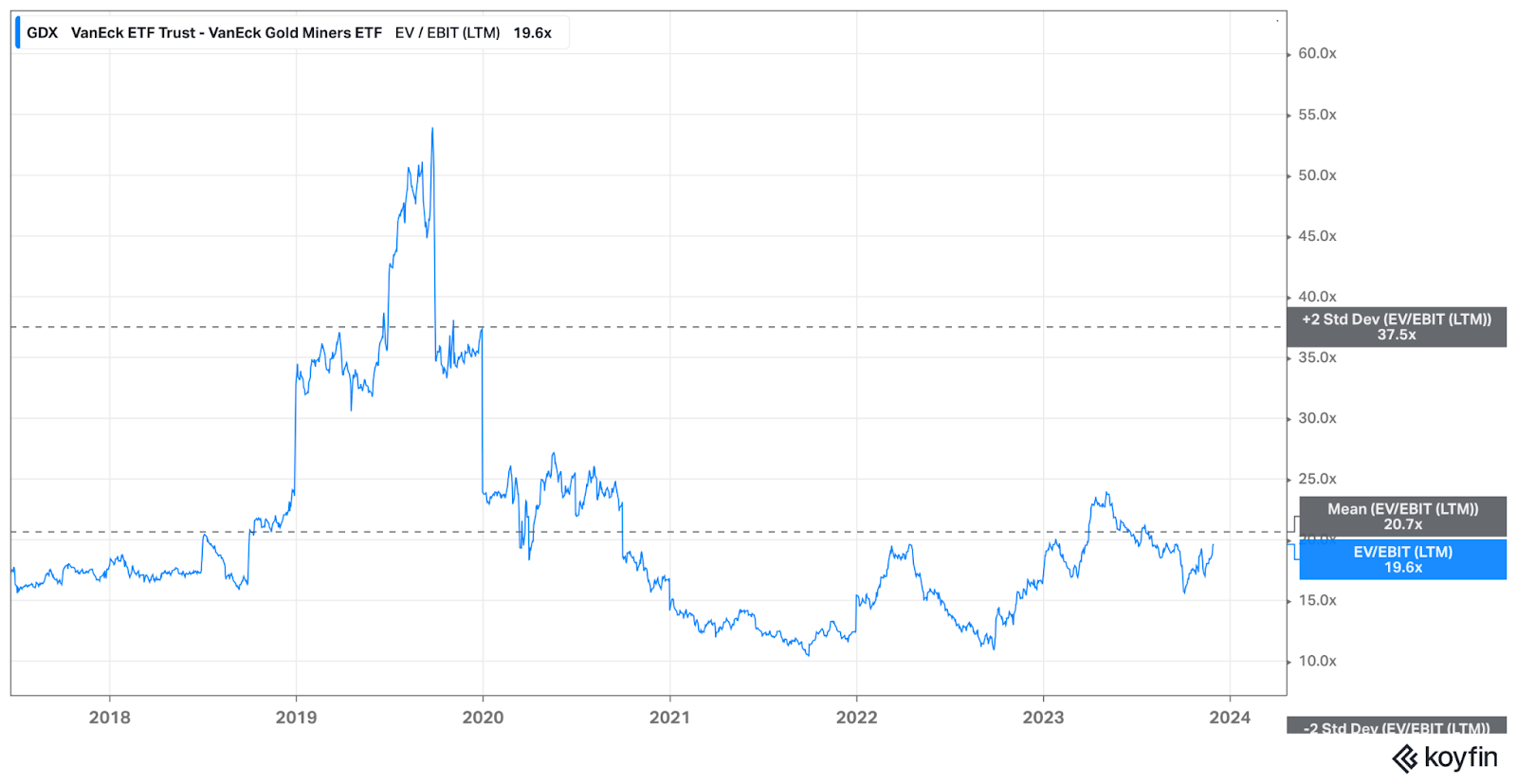

Idaho Strategic's gold business would generate $29.5 million in revenue and $14 million in operating profit for ~$1.10/share in that pricing environment. The stock trades at $6.14/share. The Vaneck Gold Miner ETF (GDX) has historically traded around 20x EV/EBIT since 2017 (see Koyfin chart below).

Does Idaho Strategic deserve to trade at a 20x EBIT multiple? Probably not. But they have no debt (outside equipment), a profitable gold production business, a great mining jurisdiction hometown, and an owner/operator that owns 12% of the company.

(Click on image to enlarge)

Let’s say there's between 12-15x EBIT. That still gets us a valuation range of $166 million and $209 million, which is 250% higher than the recent market cap.

Trying to Value the Rare Earth Package

In my previous write-up, I basically left the REE valuation discussion with, “don’t worry, you get it for free anyways.” Which is true, but it’s also somewhat lazy. I want to provide a less lazy approach now.

I asked Ian Cassel how he valued the REE land package. Surprisingly, his answer was similar to my first write-up: “You get more for free.” But he also described another instance where a coal company, Ramaco Resources (METC), popped over 100% on the news that it was turning some of its coal waste into REEs.

Here’s part of Ian’s text:

“The National Labs put money into coal waste technologies first, but these are likely higher cost alternatives to sourcing a real resource (i.e., something like IDR). IDR has a similar relationship brewing with the National Labs [as well].”

You can learn more about Idaho’s National Labs here.

Here’s where I stand on the REE assets. One day, investors will hear that Idaho Strategic is partnering with National Labs to use its REE land package for national security/energy, independence/Green Energy transition purposes. And the stock will pop.

Ramaco Resources went from $500 million to a $1 billion market cap company on the news. Why can’t Idaho Strategic double to $12/share and a $157 million market cap? That’s not unreasonable. Especially given Idaho Strategic's low share count and float.

Idaho Strategic's (Other) Hidden Asset – Its People

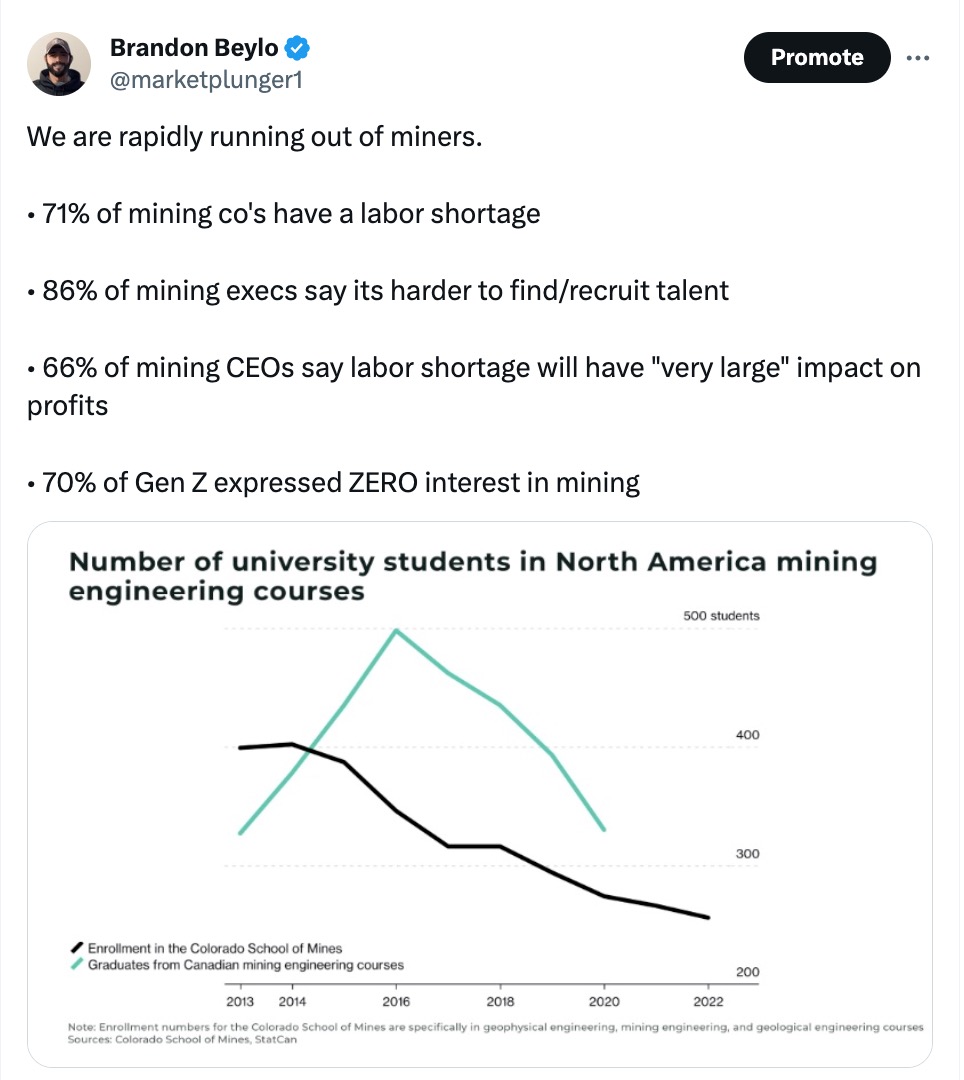

Every company says, in some form, “our people are our biggest asset.” Sometimes that’s true. Most of the time it’s not. But if you’re a mining company, it is definitely true. I’ve written/tweeted before about how the mining industry is quickly approaching a labor crisis.

Labor is like any other supply/demand market. Lower labor supply increases the value of the existing labor. Combine that with Net Zero 2050 goals and increased demand for mining labor, and you get a supply crisis.

There are two ways to think about this. One way is that mining companies will pay more for labor tomorrow than they do today. The other way is that companies with young, talented, and multi-generational/familial labor should be worth more than companies without such endowments.

Idaho Strategic has a young, talented, and multi-generational/familial workforce. CEO John Swallow mentioned it in a presentation (which I’ll paraphrase below):

“We’re a multi-generational business here. We live where we work. The people that work here can go home to their families. They don’t have to miss football games or dances or special occasions.

"My son works here. We have brothers that work here. We’ve got a few husband and wife couples that work here, that even met here. We’ve got guys that started here, had sons, and brought them into the company.”

GAAP doesn’t have a “there’s a ton of people that love working here so much that they’ve had children, brought them to work one day, and now they work here” line item on the balance sheet.

We can try to estimate the value of Idaho Strategic's workforce using Michael Mauboussin’s research on intangible asset accounting.

“Academics who study this topic seek to understand the impact of capitalizing investments from the income statement for a large sample of companies. As a result, they frequently use 100 percent of research and development (R&D), and 30 percent of non-R&D SG&A, to estimate investment.

"They also assume a standard asset life. This is a step in the right direction but is a blunt tool.

"Business analysts recognize that the investment component of SG&A varies widely by industry and company. Investors buying and selling companies based on their fundamental outlooks must reflect these differences in their assessments.”

The main idea is that investors should capitalize some of SG&A and R&D expenses as tangible investments with useful lives. Using this framework, something like payroll wouldn’t be a 100% expense, but rather part of the income statement expense and balance sheet asset.

Mauboussin references a study documenting what percentage of Main SG&A and R&D were “Investments” versus “Expenses,” with average useful life calculations. For precious metals and mining companies, 80% and 72% of Main SG&A should be adjusted as “Investments,” with an average useful life of 3.3 and 3.6 years, respectively.

I eventually want to write a longer piece on adjusting mining company income statements and balance sheets using Mauboussin’s framework. But we can think about it conceptually with Idaho Strategic.

If $0.80 of every dollar of Main SG&A is an investment, then the longer the useful life of said investment, the more valuable. An asset you can use for 10 years is worth more than an asset you can use for only 3.3 years.

Idaho Strategic's workforce (i.e., its Main SG&A) is significantly undervalued compared to its peers. The magnitude of this undervaluation is for another post.

Conclusion

Idaho Strategic is a profitable gold producer with a strategically important national resource, a founder with 12% insider ownership, and a competitively advantaged workforce.

At today’s gold prices, Idaho Strategic generates nearly $10 million in operating profit at run-rate capacity (12,500/oz per year). If gold hits its measured move, profits jump to $14 million or $1.10/share on a $6 stock.

Historically, profitable gold producers have traded around 15-20x EBIT, putting Idaho Strategic at a $150-$209 million market cap or 250% higher than its recent price.

More By This Author:

Specs Short SoybeansThoughts On Hedging Uranium Exposure

Keep It Bullish Stupid

Disclaimer: All statements are solely opinions and are for educational purposes only.