Market Analysis

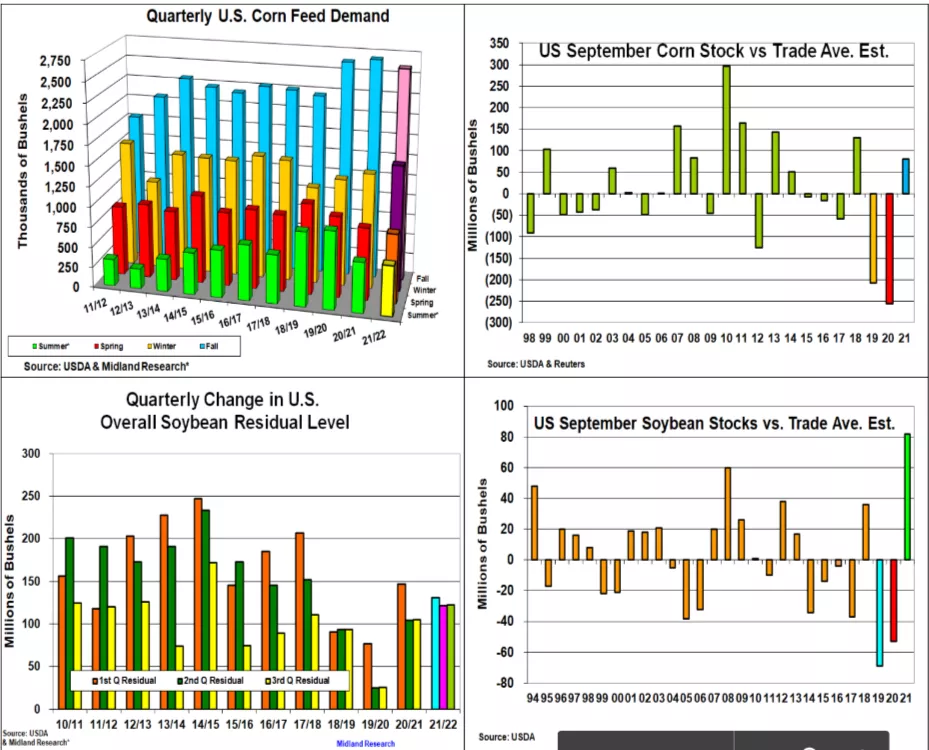

September’s US grain stocks have been quiet events in many years. These reports generally confirmed the USDA’s corn & soybeans old-crop ending stocks that were posted earlier this month. This began changing in the last decade with US crop quality, crop size, and shifting feeding levels impacting the US final stocks. This has caused some dramatic corn & soybean ending stocks changes vs expectations over the last 4-5 years. Corn’s US final carryovers have swung from 250 million less to 125 million more than trade estimates while soybeans stocks have fluctuate from 60 million lower to 80 million bu higher than the trade average. Modest increases in the US soybean crop aren’t uncommon given the need to cover soybean’s hard demand dispersals & a small residual in the past. Corn crop changes are unusual with the feed/residual being its catch-all. After quality issues in 2018 & 2019 crops, we expect a return to corn’s traditional front-loaded feeding pattern because of hefty harvest time purchases, a strong 2021 quality crop & larger DDG supplies from expanded ethanol production. However, Friday’s Cattle-on-Feed report showing summer numbers staying at or above 2021 levels because of the US Plains drought suggests higher cattle corn use. The Black Sea War elevating wheat prices & reduced HRW supplies could shave 60-70 million from cattle wheat feeding. Reduced pork & poultry numbers do counter higher corn feeding. Sluggish August exports could up 21/22 stocks to 1.555 billion bu. However, this year’s high cash basis could also be masking a smaller US corn carryover. Similar to corn, a late summer slowdown in overseas shipments could further reduce this demand by 10 million bu from the USDA’s earlier adjustment. This projects a 250 million 2021/22 ending stocks. However, this year’s high residual levels on previous 2021/22 quarterly stocks updates and this summer’s strong cash basis until just recently could be signaling an overestimate of the 2021 crop. ½ to 1 bu soybean yield changes haven’t been uncommon after the final stocks to clarify the size of crop & carryover.

What’s Ahead

Macro concerns have dominated ag prices recently, However, the upcoming US corn & soybean ending stocks remain important along with this fall’s US yield reports & China’s US purchases. La Nina has already impacting Argentina’s wheat & Brazil’s soybean seedings are just beginning. Be prepared to up 2022 sales 20% on strength into the $6.90, $14.75, and $9.75(KC) price areas.

(Click on image to enlarge)

More By This Author:

September US Crop/S&D Reports - Lower Midwest Yields Pulled US Crop Outputs Down

Western Midwest Heat/Dryness Vs. The ECB Moderation - The Big Question

US ECB Corn & Bean Counts Couldn’t Cover WCB Heat/Dryness

Comments

Log in or sign up to join the conversation.