Compared to almost all other assets, precious metals are the undisputed stars, – not only this year, but also over the last five, the last ten, and even more years. If you delve deeper into the archives, you will see that you have to go back to November 1, 1998, to find a performance comparable to that of Gold – since then, the Nasdaq Composite has been shining, long before the internet bubble burst. Gold has been outperforming the S&P 500 since September 15, 1996.

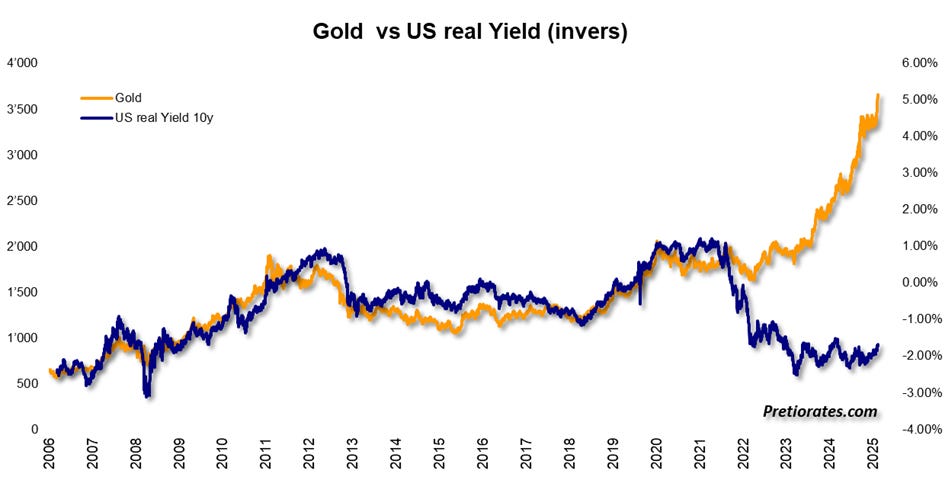

The media and experts juggle all kinds of explanations as to why the price of Gold may rise. Falling interest rates? A fairy tale. Remember the 1970s: while interest rates climbed to historic highs, Gold experienced its true heyday. In the end, there are only two factors at play: real market returns – i.e., returns after inflation – and confidence in one's own government, with emphasis on the word ‘own’ and thus also one's own currency.

Since spring 2022, however, real market returns have ceased to set the pace. The trigger? Hardly coincidentally, it was the war in Ukraine, which began in 2014 with the Maidan, but only came to the attention of the world public with the Russian invasion in 2022. Since then, the price of Gold has moved largely independently of real returns. The decisive driver remains confidence in one's own government.

And what about the annual production of around 3,300 tons of Gold, the relationship between supply and demand? Its influence is marginal. Several thousand tons change hands every day in London, and even more on the COMEX via futures. More importantly, Gold is not consumed, it does not disappear. Global reserves – now standing at 216,265 tons – are simply growing by around 1.5% per year. A drop in the ocean. The higher the price of Gold rises, the stronger the urge to take profits becomes. For the price of Gold to continue to rise, demand must therefore increase. The same applies to the downward trend.

However, a weakening currency drives up the price of Gold in its own currency – investors in Zimbabwe, Venezuela, or Turkey can attest to this. This also applies to the US dollar. Confidence in the United States is eroding, and not because of the current administration. The growing national debt is weighing heavily – a legacy of several presidents. At the same time, geopolitical fires are raging, in which the major powers are becoming increasingly entangled. Swiss investors, on the other hand, benefit from political and monetary stability—at least so far. Even if they too are increasingly worried. Nevertheless, the percentage performance of Gold in Swiss francs is correspondingly weaker.

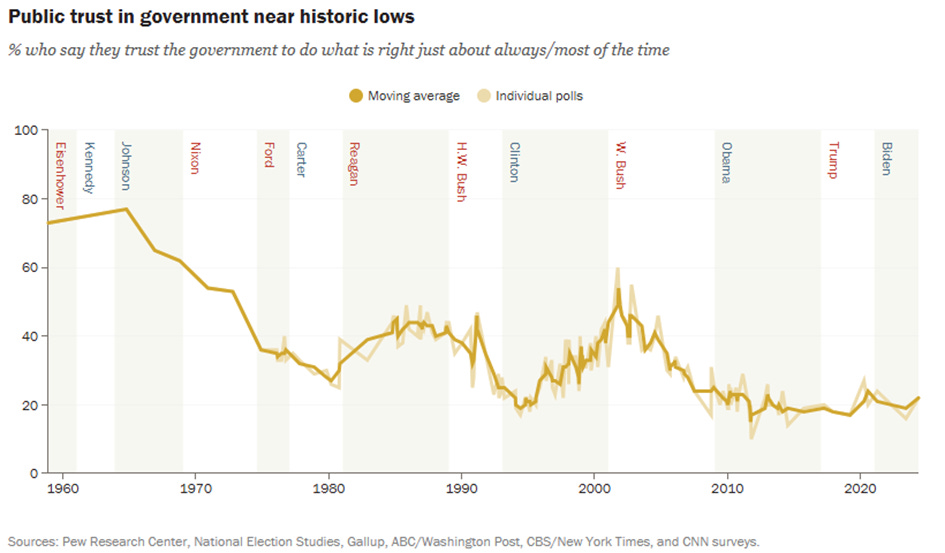

The fundamental question of the future trend for Gold is therefore quickly answered: as long as mistrust of one's own government increases, so does the price of Gold – in the respective currency. Confidence in the US government has reached an all-time low. And history teaches us that long-term bull markets usually end with a spectacular finale, in which panic and greed drive the market skyward.

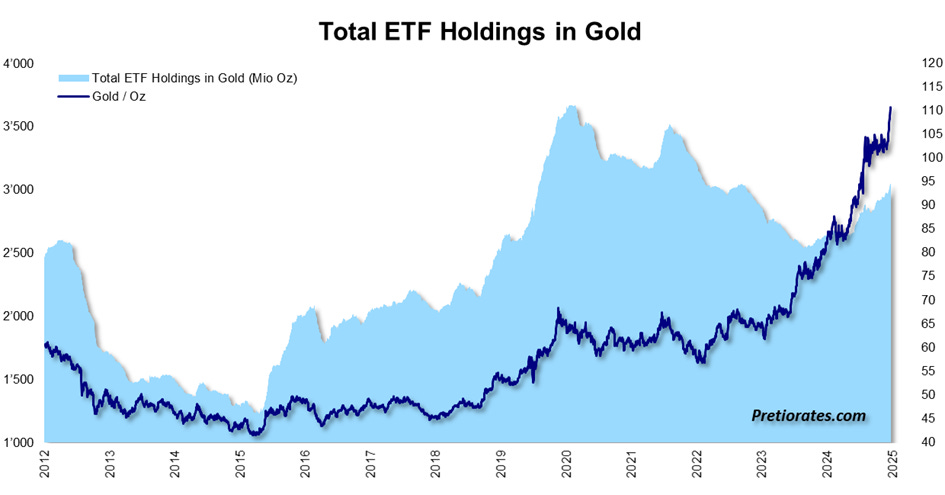

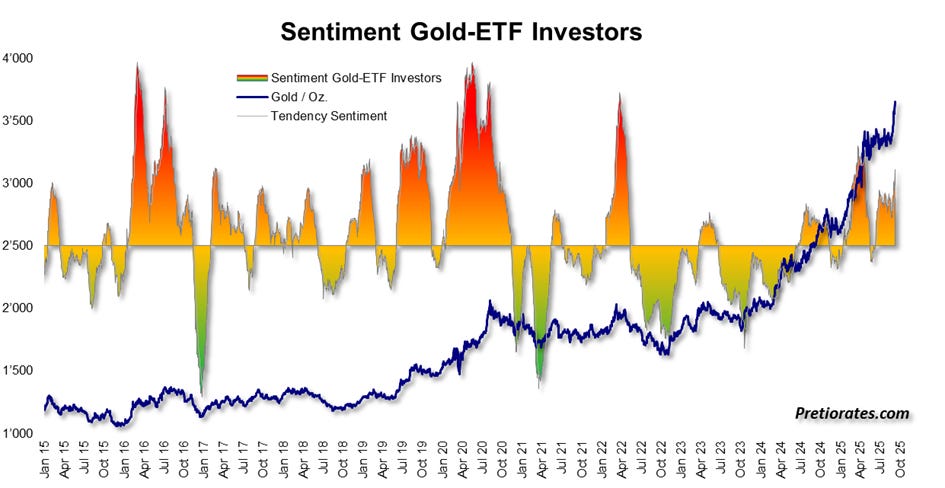

But we are not there yet. In the short term, the number of ETFs issued with physical Gold backing is a good indication. Recently, this has been steadily increasing, but is still well below the peak of 2020.

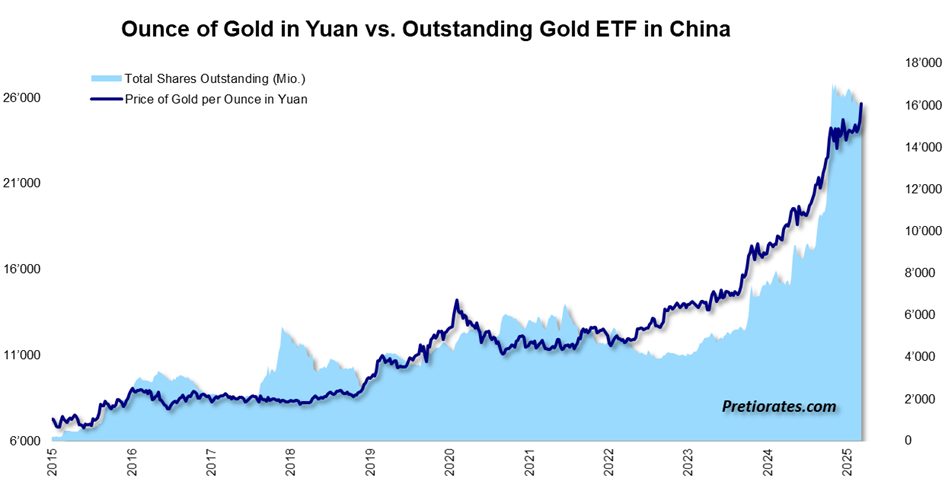

Chinese investors are particularly interested in physical Gold. However, this only covers about 10% of daily trading volume – but is generally traded at the same price. So-called ‘Paper Gold’ is therefore still responsible for setting the price. Nevertheless, it is interesting to note that Chinese investors have not increased their exposure to Gold ETFs in recent months following last year's rush.

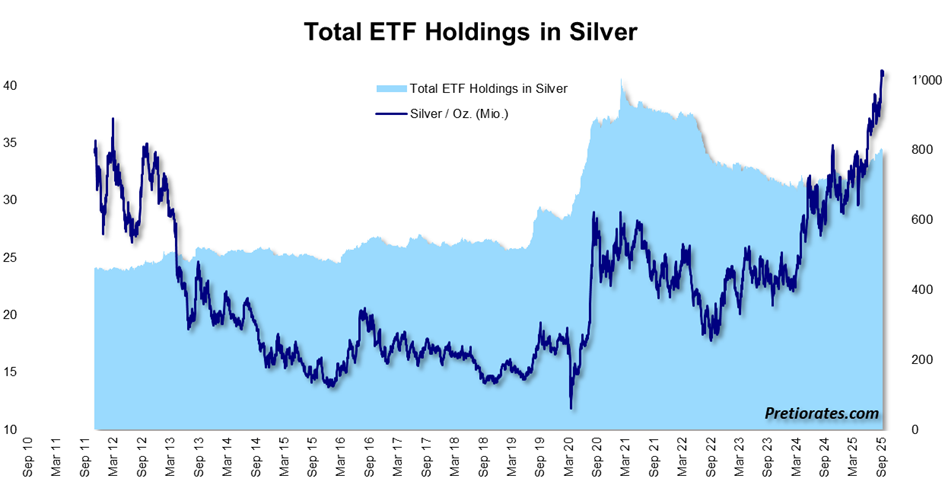

The same applies to the number of Silver ETFs outstanding worldwide. Despite the massive advances in the price of Silver recently, interest in Silver ETFs can still be described as ‘limited’...

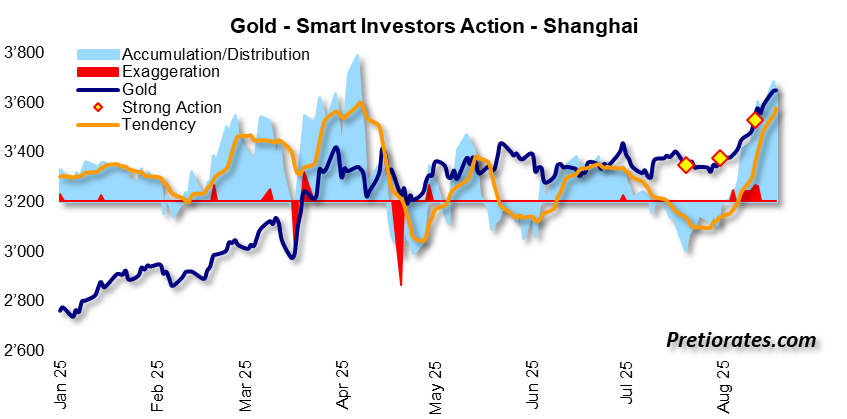

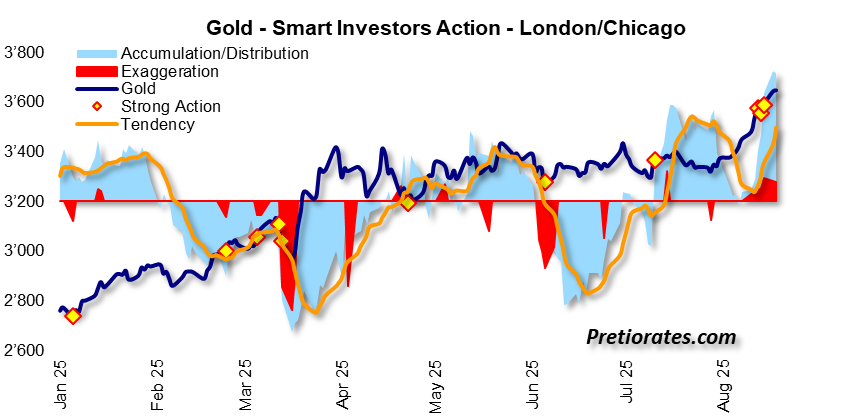

However, smart investors have been buying Gold heavily again in recent days and weeks. The accumulation, shown in the chart by the light blue area, has increased significantly in Shanghai,

...and has even reached record levels in the Western Hemisphere. If it is so strong, a consolidation must also be expected. No asset shows a one-way direction in terms of performance.

In the long term, however, sentiment is far from the euphoria we saw in the market during previous peak prices...

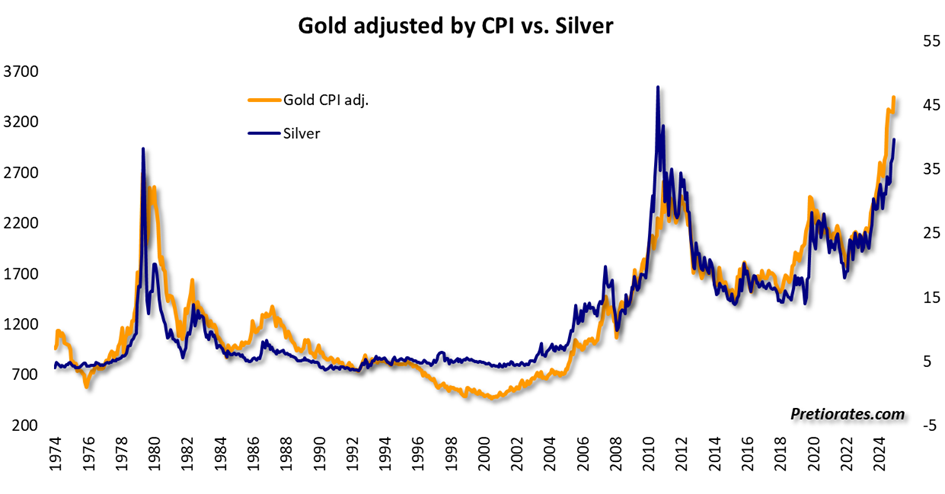

At the same time, Silver remains the eternal laggard – with plenty of catch-up potential. In purely mathematical terms, based on the inflation-adjusted price and compared to the price of Gold, the price of Silver should have reached around US$45 per ounce long ago.

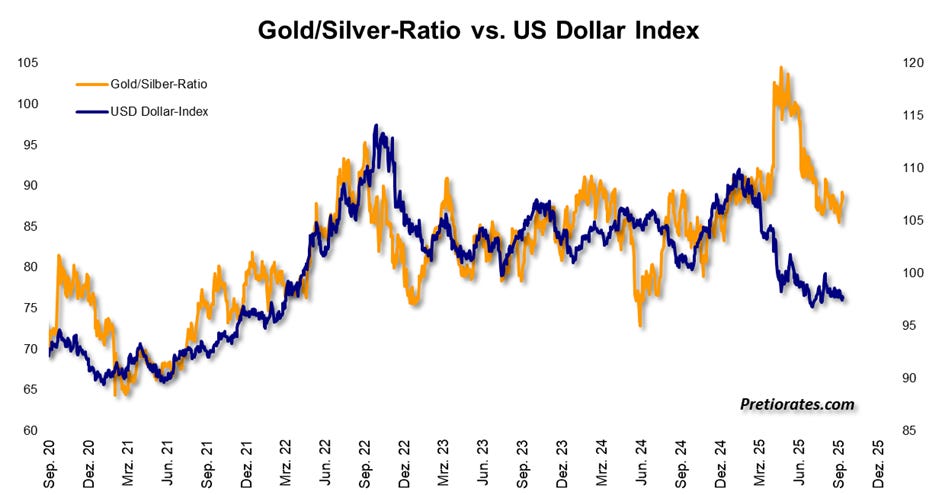

And if the Gold/Silver ratio were to fall to a level of 77, where it should actually be at present in comparison to the development of the US dollar, then the price of Silver would indeed be above US$45 per ounce...

Bottom line: In the short term, precious metals may appear overheated – consolidation is always in the air. But in the medium and long term, the compass clearly continues to point upwards. As long as mistrust in governments continues to grow, Gold will remain the safe haven into which capital flows.

More By This Author:

In Autumn When The Leaves Fall...

Decoding The Nonsense: Trying To Find Logic In Trump’s Puzzle

Jackson Hole, Market Hold Their Breath

Comments

Log in or sign up to join the conversation.