AgMaster Report - Wednesday, April 17

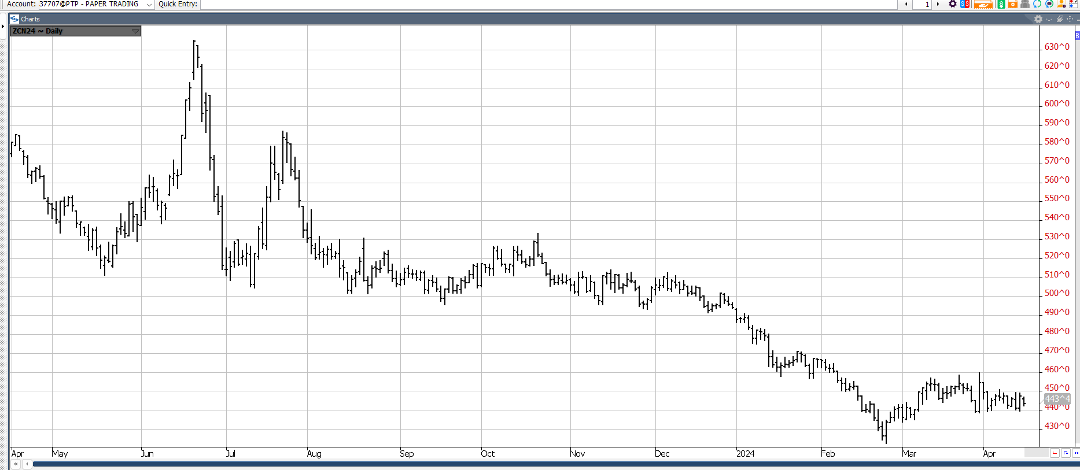

JULY CORN

(Click on image to enlarge)

For the past 6 weeks, July Corn has been locked in a tight 20-cent range (440-460), as headwinds such as planting pressure, rains in the dry areas, the Iranian airstrike & the April WASDE Report push it down to the 440 level & tailwinds such as today's export at inspections 1.333 mmt & todays flash sale of 165,000 mt to Mexico lift it to the 460 level! Traders were generally disappointed by the wide disparity in the South American estimates tssued last Friday between the USDA (124) & CONAB (112) & feel the May WADSE will correct it! Common sense would say Brazil has a better handle on their crop size than the USDA!

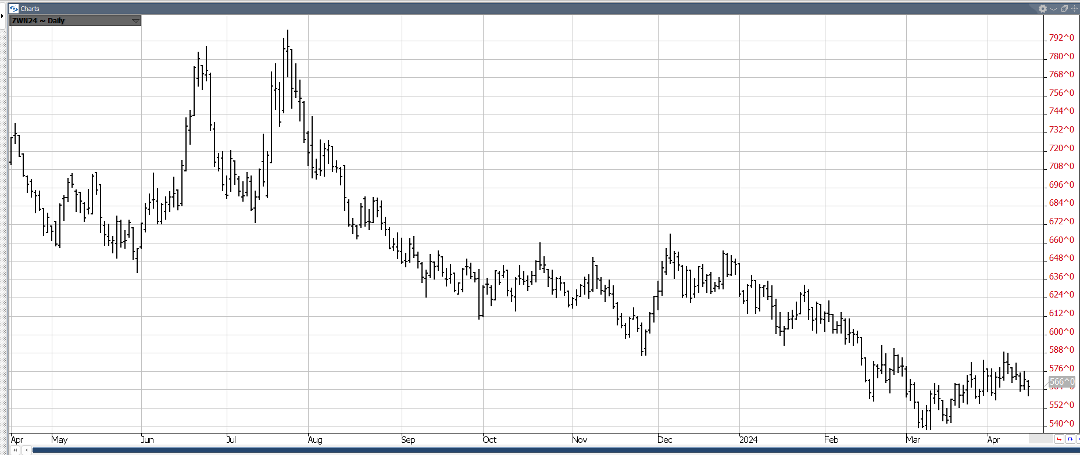

JULY BEANS

(Click on image to enlarge)

1155 to 1230 has confined July Beans since Mar 1 as it also labors in a tight range buffeted by both positives & negatives! This past week, 3 export flash sales were reported to unknown destinations – 124,000, 254,000 & 124,000! But offsetting that was the USDA report last Thur at 11am CST – keeping the Brazil Beans at 155mmt vs the Conab estimate of 146mmt! This is a very wide discrepancy for this late in the growing season & we expect it to be rectified in the MAY WADSE REPORT! Meanwhile, the mkt is closely monitoring the early planting progress – with corn at 6% & beans at 2-3% complete – due out today at 3pm! With the mkt $2.50 under last Summer & a still sizeable short fund open interest, we feel the mkt leans to an upside bias – when it finally emerges from its sideways, consolidation pattern!

JULY WHT

(Click on image to enlarge)

July Wheat was able to back-and-fill its way higher for about a 40 cent rally – before the mkt’s negative reaction to last Thur’s WASDE forced a correction! However, we feel Russian’s recent export woes, the escalating Middle-East conflict, recent Russian military strikes & general dry conditions of their emerging wht crop all favor less production & more exports – and therefore higher prices!

JUNE CAT

(Click on image to enlarge)

Since late March, June Cattle has plummeted $16 (186-170) – mostly off the impetus of a bearish March Cattle-on-Reportwhich reported placements at 10% over 2023 (est-6%)! The downswing was then exacerbated by the Bird Flu Epidemic which cast serious doubt on beef demand! However, this incident was later mitigated – leaving the mkt sharply over-sold! So, a fierce short-covering rally (170-176) ensued – sparked by our entry into the Spring Grilling season – the best demand period of the year! We look for the mkt to continue to recoup part of the $16 loss – triggered by the fateful March 22nd Cattle-on-Feed Report!

JUNE HOGS

(Click on image to enlarge)

On April 10th, a major Key Reversal occurred – with new contract highs scored early in the trading session – followed by a precipitous decline of nearly $5.00 & a close well under the previous 2-wk lows! The mkt continued down another $4-5.00 to last week’s low of about $101 – as heavier slaughter & pork production fueled the down! But after nearly an $8.00 drop, the mkt became quite oversold & being amidst the best demand period of the year, has rallied back $3.00! We look for all the outdoor grilling to push the mkt back up toward it early April highs! Helping that rally is the fact that China’s 1st Qtr pork production declined to 15.8 million tons – the first qtly fall in 4 years! This seems to indicate that they are finally getting their excess production under control – a positive for pork exports!

More By This Author:

AgMaster Report - Wednesday, April 3

AgMaster Report - Monday, March 18

AgMaster Report - Tuesday, March, 12