The Yen Carry Dump

Weak employment data, the simmering Middle East, election jitters, and many other factors are taking the blame for rattling the markets. Those are important issues, but the infamous yen carry trade is the culprit. How do we know? Some of the assets most popular with short-term speculators are getting hit the hardest. Furthermore, the sharp declines in those popular assets align with surges in the yen.

The following example of the yen carry trade is from our article, Japanese Inflation – Liquidity Crisis In The Making. The article is from 2022.

For example, you go to a Japanese bank and put down $100,000 in assets to borrow 1,000,000 yen for one year at 0%. You convert the yen to dollars and buy a one-year U.S. Treasury note at 3%. Assuming the yen’s value doesn’t change versus the dollar, the return will be 30% (3% * 10x leverage). If the yen appreciates by 1% over the year, and you did not hedge the currency risk, the return falls to 20%. A 5% appreciation of the yen results in a 20% loss.

The article’s example was a conservative version of the yen carry trade using a low-volatility Treasury note and comparatively minor yen moves. Now, consider that yen carry traders have been leveraging much more volatile assets like crypto, mega-cap US stocks, and Japanese stocks. Moreover, the yen has appreciated 15% in the last few weeks, as shown below. As the yen appreciates, the Japanese banks demand more collateral to support the loans. The investor then must put up more collateral or reverse the yen carry trade. Reversing, or forced liquidation, pushes the yen higher and said assets lower.

For now, the carry trade victims appear limited. We presume the Bank of Japan and the Fed have been on the phone constantly and will intervene in the currency markets before the problem spreads to a broader array of assets.

What To Watch Today

Earnings

Economy

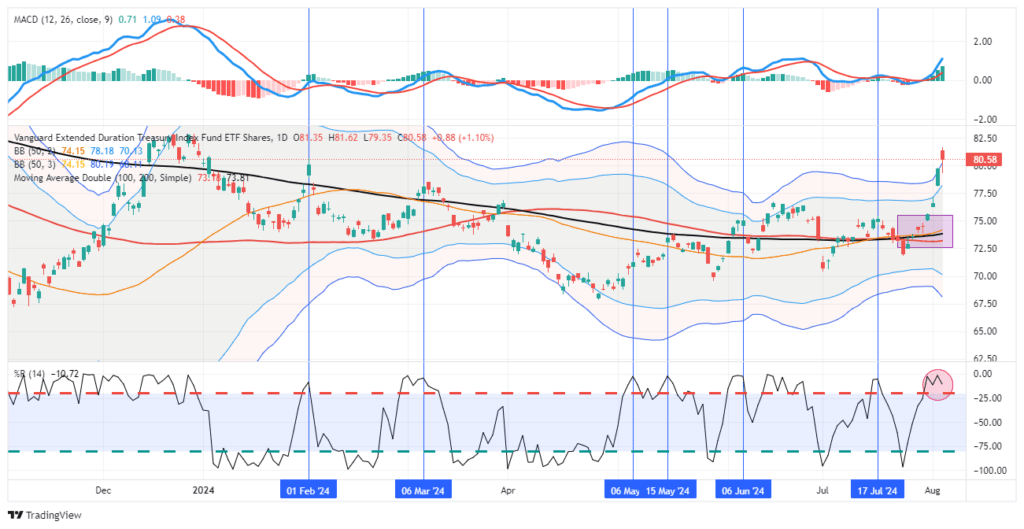

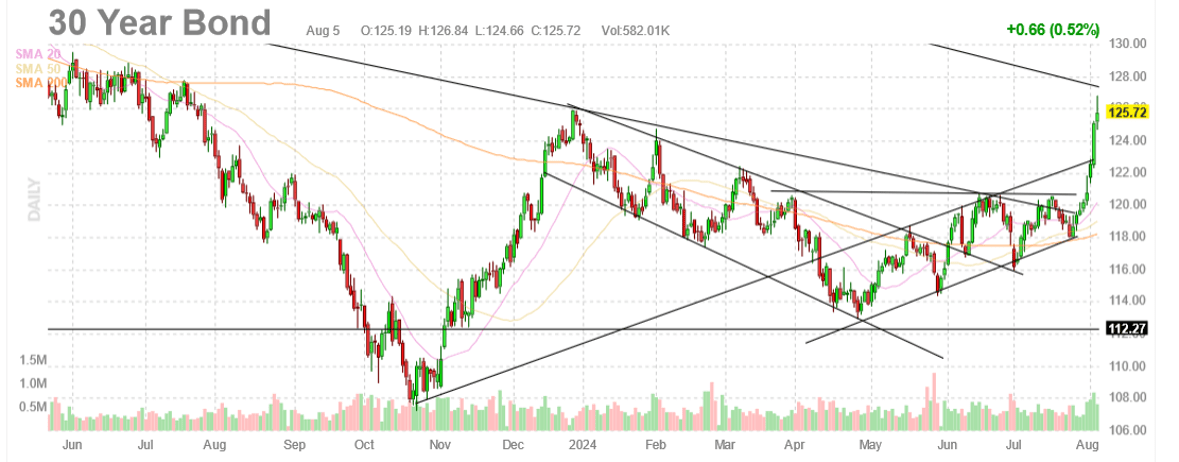

Market Trading Update

As discussed yesterday, the market selloff caused by the “yen carry trade” certainly surprised traders. However, while stocks sold off, bonds rallied as the “risk off” trade continued recent momentum. From a trading perspective, bonds are now extremely overbought, and we will likely see a pullback in the next few days as potential profit-taking sets in. The ISM Services report was stronger than expected on Monday and was back in expansion territory. Given that services comprise nearly 80% of the economy, such suggests a near-term recession is unlikely.

The good news is that Treasury bonds have cleared all previous resistance levels, confirming the recent breakout. However, given the extremely overbought conditions, a retracement of the recent gains should be expected. Key support is the cluster of moving averages that coincides with the downtrend from the end of 2023.

We have previously warned that bond movements would be rapid. This is because Treasury bonds are the “risk-off” trade and become “in demand” when an event occurs. If you want to add bonds to your portfolio, remain patient and wait for a reversal of some of the more extreme overbought conditions. If you are long bonds, this isn’t a bad place to take some profits and rebalance holdings to target weights.

(Click on image to enlarge)

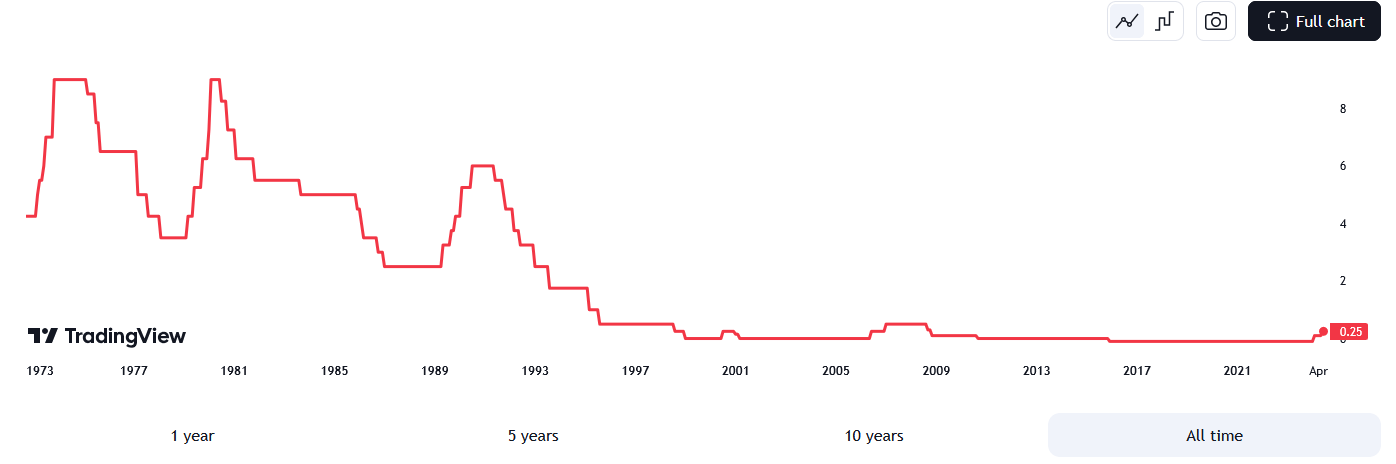

The BLS Is the Unlikely Driver Of The Yen Carry Dump

A few days ago, as shown below, the Bank of Japan raised interest rates to 0.25%, a 15-year high, and released a detailed plan to slow its bond-buying program. Higher interest rates and more prudent monetary policy are positive for a currency. Conversely, Friday’s weak BLS employment report and other poor economic data make Fed rate cuts more likely. Moreover, the Fed may slow down QT. Simply, the BOJ and Fed are moving in opposite directions. The result is a strengthening yen versus the dollar.

As the yen strengthens against the dollar, the yen carry trade becomes less rewarding. Therefore, if the BOJ continues to raise rates and reduce QE and if the Fed embarks on a rate-cutting policy, the yen will appreciate further. If it can do so relatively calmly, the risk to asset markets should be minimal. However, if the currencies move abruptly, so will the markets. Ergo, if there is central bank intervention, it will likely involve the currency and not emergency Fed rate cuts.

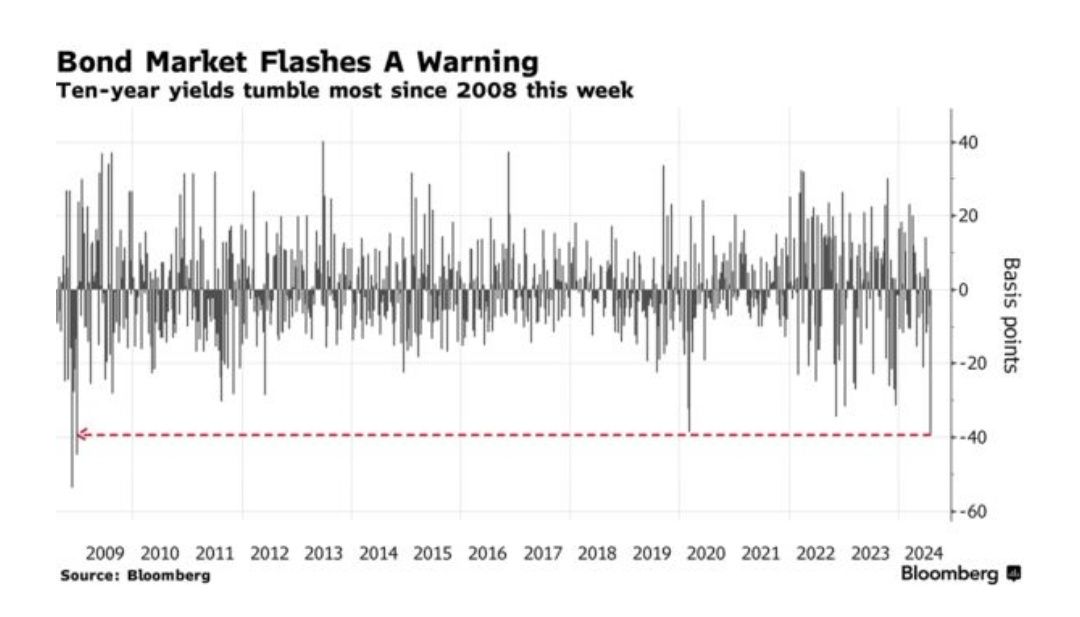

Bond Yields Tumble

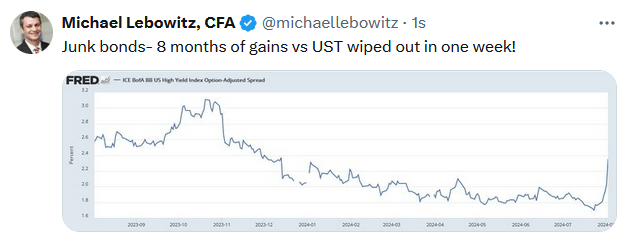

The bond market sent a clear warning last week. As shown below, last week’s 40bps decline in ten-year yields was the largest since the financial crisis. To be fair, yields fell by slightly less than 40bps during the start of the pandemic. Such a sharp drop in yields so suddenly is what the market calls a flight to safety. Typically, investors sell risky assets in times of turmoil and flock to safer ones.

The second graph shows the 30-year futures price of treasury bonds. Over the last week, bond prices broke out of a wedge pattern and briefly surpassed the December 2023 high. Furthermore, its price is closing in on a longer-term resistance line dating back to mid-2020 when yields were at record lows. We suspect that will hold as resistance until evidence of a recession becomes more significant. However, further yen carry volatility may push it higher temporarily. When the markets calm down, we suspect the price will fall back to prior resistance, between 120-123. From that point, a more sustainable rally will be possible.

Tweet of the Day

More By This Author:

Yen Carry Trade Blows Up Sparking Global Sell-Off

Why The Carry Trade Matters

Are The Credit Markets Cracking?

Disclaimer: Click here to read the full disclaimer.