Central bankers' hawkish response to indications of ever-stickier inflation has struck a nerve with markets which continue to ramp up rate expectations. But it is seen as the right medicine, with market-based inflation expectations dropping further while risk assets are holding up fairly well for now.

Markets are increasingly bracing for the Fed to up the pace again

The US jobs data remains the key data point looming large at the end of this week, but that hasn’t kept markets from further raising their expectation for a 50bp Fed hike yesterday. We think markets will need to see material evidence from Friday's report to row back after Fed Chair Powell opened the possibility of increasing the hiking pace again in his testimony.

Data in the meantime chimes with the narrative of a still tight labour market

Data in the meantime chimes with the narrative of a still-tight labor market. The ADP payrolls estimate beat expectations, and job openings were reported in excess of 10.8 million yesterday, meaning that there are still around 1.9 openings for every unemployed worker. Today’s eyes are on the initial jobless claims where a number below 200k would also give little evidence of the labour market cooling.

The US market is in the driving seat into the payrolls. While the front end has pushed higher, the back end is resisting to get back above 4%, thus further inverting the curve which is now stretching towards -110bp. That is not to say that investors are eager to pick the close to 4% in 10Y US Treasury yields. Yesterday’s 10Y auction was in stark contrast to the stellar results of prior bond sales this year, highlighting some unease ahead of the payrolls and also next week’s key CPI data.

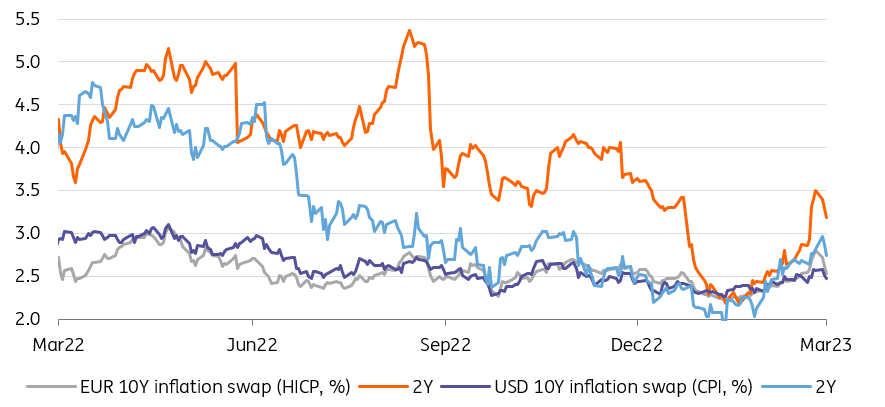

What the doctor ordered: Hawkish central banks are having the desired effect on inflation expectations

Image Source: Refinitiv, ING

Risk sentiment does not stand in the way of higher rates for now

If data does not stand in the way of higher rates, the other factor potentially capping the rise in longer-dated yields especially remains risk sentiment. Clearly, the deep inversion of curves is already a reflection of concerns that central banks are overdoing it, but risk markets themselves are proving remarkably resilient in light of tightening already delivered and still expected.

Italian spreads have withstood rising volatility and hawkish comments

In the eurozone markets the key spread of 10Y Italian government bond yields over German Bunds withstood rising volatility and hawkish comments. It has actually tightened and now resides below 180 bp. This is even more impressive as just this week the European Central Bank’s Holzmann has broken with the unwritten rule of not discussing the ECB’s forward guidance on the reinvestment of the Pandemic Emergency Purchase Programme portfolio, where a full reinvestment is currently still signalled at least until the end of 2024. Holzmann had suggested including PEPP in quantitative tightening this autumn. Recall that the possibility to flexibly reinvest PEPP maturities still is the ECB’s easiest-to-activate first line of defence against any spread of turmoil. Rolling off the portfolio could be seen as diminishing this firepower.

While measures of (implied) rates volatility have started to tick up again since late February, spreads that have before shown to be quite sensitive to such dynamics have indeed budged very little.

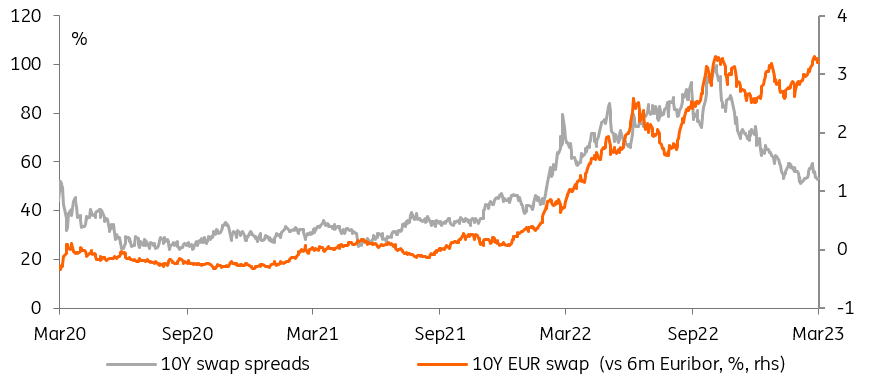

Collateral scarcity fears are no longer holding back Bunds

Image Source: Refinitiv, ING

The Bund spread versus swaps can also be subsumed under market risk measures, though it has become more of a measure of collateral scarcity fears since the ECB’s pandemic interventions. And collateral scarcity really became an increasing concern with rising market volatility at the start of the broader market sell-off in 2022, driving also the directionality of the Bund asset swap spread – Bund yields had struggled to keep pace with the quick rise in swap rates.

Since then a lot has changed: The ECB and the debt agency have made more collateral available for lending, and especially last month the ECB has shown its sensitivity to the issue in the handling of government deposits on its balance sheet. Add to that the ECB's quantitative tightening is underway since this month as well. What we now see is that the directionality of the spread has been broken, and it is also budging with the latest uptick in implied volatility measures.

Today’s events and market view

Today’s data calendar is fairly light with the highlight being the US initial jobless claims. The market is looking for a small increase in initial claims to 195k, which would still leave it below the pre-pandemic average of around 219k for 2018 to 2019. The key to validating current market pricing remains tomorrow’s US jobs data.

After the European bond supply from Ireland and the BTP Italia sale to institutional investors today, the focus in primary markets should be tonight’s 30Y UST auction. It follows yesterday’s weaker 10Y sale, although past 30Y sales have already stood out weaker compared to the strong sales metrics in the other maturities this year so far.

Late in the night, attention will turn to Japan for the last Bank of Japan policy meeting under governor Kuroda. Our economists note that he is well known for surprising markets, but believe that he will leave a decision on the future of the bank's yield curve control policy to his successor Kazuo Ueda.

More By This Author:

The Commodities Feed: First US Crude Draw This YearIndonesia: Looking To Consumption To Carry The Load

Stagnating Eurozone GDP Is Worse Than It Seems

Comments

Log in or sign up to join the conversation.