CoCo Pops: Only Half Price? Some Thoughts On Bank Capital

I did not devote any time to the Credit Suisse ‘take-under’ by UBS in my weekend note. A wry smile passes the lips of the 🐿️ as, for most of my career on the sell side, it was typically the ‘other Swiss bank’ that was having close shaves with the Grim Reaper. I wish friends and former colleagues at both shops well.

Source: woolworths.com.au. 🐿️ Annotation

For me, the most interesting thread to pull on from the CS news is the debate around bank capital. Specifically, the fate of the bank’s AT1 (“Alternative Tier 1”) or CoCo (“Contingent Conversion”) bonds which were zeroed on Sunday afternoon with a sweep of the Swiss National Bank’s pen.

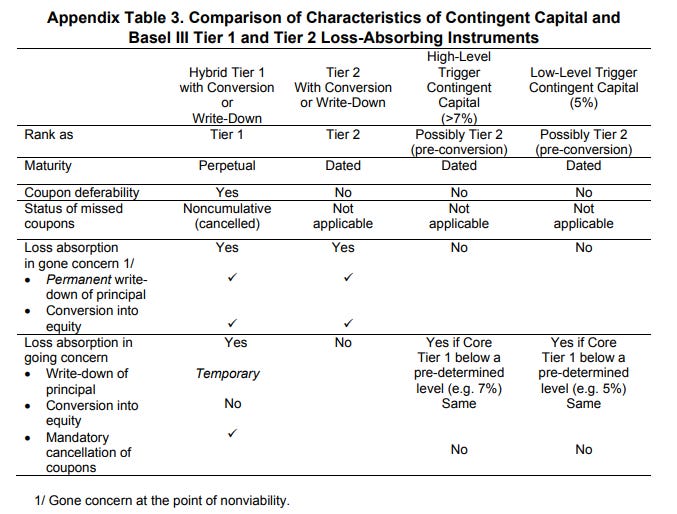

Bank capital is a nerdy topic but one with which your favorite 🐿️ has a degree of familiarity. Hybrid equity capital for banks takes a whole alphabet soup of different forms. If you are short of sleep, you can read more from the IMF here. Actually, don’t click the link. The extracted table below should be enough to scare you off!

Source: IMF

It’s a bit like Eskimos and their different names for snow. Except it’s not. I looked it up. According to the Canadian Encyclopedia (and I guess the Canadians should know):

It is often said that the Inuit have dozens of words to refer to snow and ice. Anthropologist John Steckley, in his book White Lies about the Inuit (2007), notes that many often cite 52 as the number of different terms in Inuktitut. This belief in a high number of words for snow and ice has been sharply criticized by a large number of linguists and anthropologists.

Sorry to bust that particular urban myth for you. Anyway, the whole bank hybrid market was basically made up ‘on the fly’ in response to past banking crises. These instruments are designed to create layers of loss absorption in bank balance sheets that allow financial institutions to run with as little (very expensive) common equity share capital as possible. Let’s face it, bank returns without leverage are pretty uninteresting.

My own dealings with bank hybrids date from my time as an equity-linked / convertible bond banker in the early 2000s when, as a structure of bond instruments that converted to equity, you would have thought I would be front and center. However, I was typically told by my wide-elbowed colleagues in debt capital markets that bank contingent convertibles for financials were “none of your goddam business”. Nevertheless, given the job description on my business card, I attended endless lengthy meetings on the topic.

The hybrid instrument structuring debate revolved 100% around the satisfaction of arcane legal, accounting, and ratings agency treatment outcomes. The value of any embedded put or call option on the common shares of the issuer was completely and utterly irrelevant.

Ambiguities in the structure of these instruments are embedded everywhere. I suspect that this is a deliberate ploy to give regulators maximum flexibility when the proverbial should happen to hit the fan (just like last weekend).

In this case, and to cut a long story short as it is not always the case, CS's bank hybrids were (very) junior bonds. In fact, they were so junior that they were subordinate to the interests of the [Saudi sovereign and Swiss retail] owners of the bank’s ordinary shares. We will pick up that [very interesting] thread another time.

In an ordinary world, investors might expect to be compensated royally for that degree of subordination. However, at the tail end of a 40-year bull market in bonds it was getting pretty tough for fixed income investors to find any high-grade paper that could offer them any income at all.

Silly question. This Austria deal was a blowout success!

So, junior bonds of high-grade banks were a way in which fixed income investors could eke out a bit more yield while praying that nothing existential happened (once again!) to the global banking system. The history went and did that rhyming thing again:

Of course, these AT1s and CoCos - supposedly intended only for professional investors / ‘consenting adults’ found their way in to retail hands via the ETF / UCITs market. This little gem of a collective investment from Invesco. Chart: Tradingview.

As interest rates started going up last year, less risky alternatives (ie proper senior bonds) started to offer a positive yield. The hybrids sold off aggressively in line with the broader fixed income market. However, note that the duration of these bonds (and therefore the amount by which they would go down with rising rates) was still being calculated by reference to their expected life (more on that below).

Now that this fixed income (no equity upside or growing dividends for the risk here) paper has proven its juniority, it is tough to know who the natural buyer for these instruments will be in the future. If you are an institutional money manager, you now certainly need a very good excuse to have these sitting on your pad at quarter end.

Remember also that these AT1 / CoCO bonds are typically structured as perpetual instruments with no fixed redemption date. They were valued by the market on the basis of a yield to their earliest “call” date at which the issuer could redeem the notes in full. But what is the real duration of these instruments now?

Given that the market for new issuance of bank hybrids is now probably on ice for a while, bank treasurers don’t really have to keep a new issuance market happy by honoring the ‘handshake’ agreement to redeem the hybrid paper at the earliest call date. Issuers might be tempted not to call them at all. You could even argue that now that this type of paper has been proven to be subordinate to common equity, bank treasurers in fact have a fiduciary obligation not to call them!! Roach Coco Motel time??!!

Source Raeside Cartoon. 🐿️ amendments.

Implications. Just as banks are discovering that they need to be more competitive with their deposit rates, another key tool to manage bank cost of capital just got - at the very least - a whole lot more expensive. Returns will suffer. We sold 100% of our European financials exposure last week and are in no hurry to get back in.

More By This Author:

Disclaimer: Please see full disclaimer at https://www.blindsquirrelmacro.com/disclaimer

Good read, thanks.

Thanks Duanne

What is with the squirrel pictures? I don't get it.

Hi Harry. Even a blind squirrel finds an acorn (in my case a decent investment hopefully!) from time to time.