Image Source: Pexels

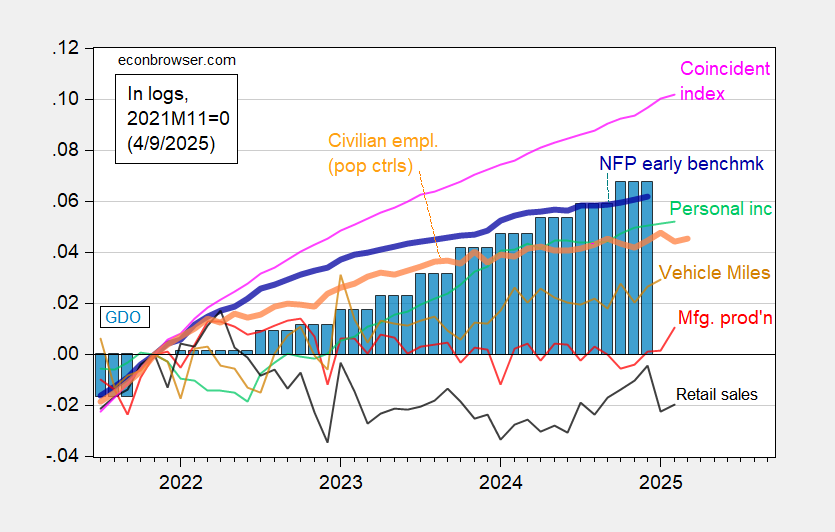

Coincident index growth slows from 4.1% m/m AR to 1.7% in February.

Figure 1: Implied Nonfarm Payroll early benchmark (NFP) (bold blue), civilian employment adjusted smoothed population controls (bold orange), manufacturing production (red), personal income excluding current transfers in Ch.2017$ (bold green), real retail sales (black), vehicle miles traveled (tan), and coincident index in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2021M11=0. Source: Philadelphia Fed [1], Philadelphia Fed [2], Federal Reserve via FRED, BEA 2024Q4 3rd release, and author’s calculations.

No apparent recession start as of February preliminary data, but retail sales look somewhat pessimistic.

More By This Author:

The Recession Start Predicted (Post-Pause)Stay Tuned For Dollar Share Of World FX Reserves

The Yield Curve: Steepening And Inverting

Comments

Log in or sign up to join the conversation.