The weekend’s events in Iran have sparked military tension and supply chain issues that go well beyond regime change and oil prices.

As the United States and Israel launched a joint military operation across Iran, its Supreme Leader, Ayatollah Ali Khamenei was killed in the strikes. Within hours, Iran fired missiles at U.S. military bases across Qatar, Kuwait, Bahrain, and the UAE, and Iran’s Revolutionary Guard (IRGC) broadcast transit bans through the Strait of Hormuz.

Spot gold topped $5,278 on Saturday, up from pre-strike levels. Brent settled Friday at $72.48 and WTI at $67.02.

Now, oil is dominating the commodity headlines, followed by gold, for physical chokepoint and geopolitical reasons. Silver futures prices leapt from $87.58 at Friday’s close to $93.29 on Saturday, for similar reasons.

As two of our top five focus commodities for 2026, we expect gold and silver to continue to outperform oil during this unfolding situation.

Yet another major impact from the conflict now deserves attention - because these strikes will impact the nuclear fuel supply chain and uranium prices in particular.

Strikes Targeted Enrichment Infrastructure

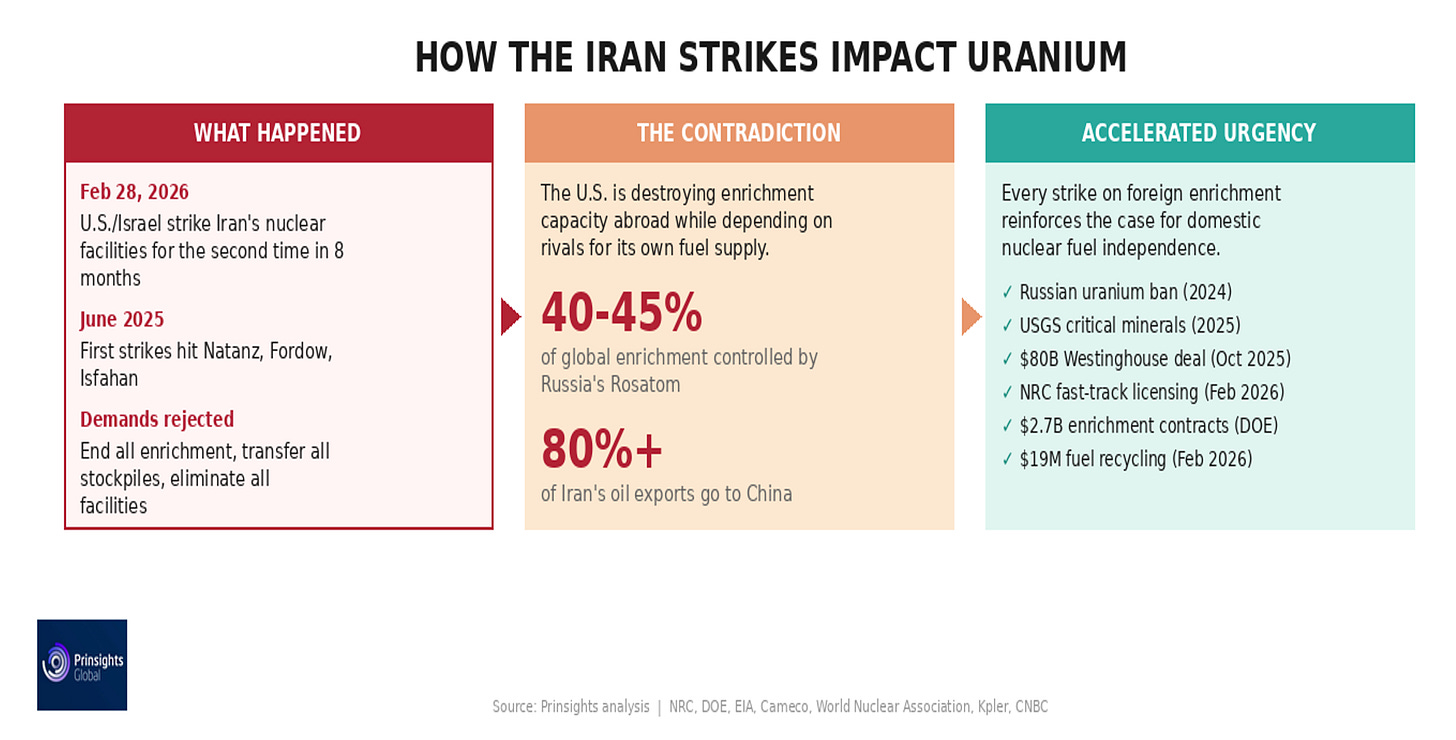

This is the second time in eight months that the U.S. has struck Iran’s nuclear facilities. The June 2025 operation hit Natanz, Fordow and Isfahan. The White House at the time claimed to have “totally obliterated” Iran’s nuclear program.

However, U.S. intelligence assessments that emerged in February told a different story. Iran had spent the months since June rebuilding and fortifying its enrichment infrastructure, repositioning centrifuge halls under 80 to 100 meters of granite and fortifying its sites against the same kind of bunker-buster strikes the U.S. had already used.

The core U.S. demands that Iran rejected leading up to the February 28 strikes included a permanent end to all uranium enrichment, the transfer of all enriched uranium stockpiles to U.S. control and the elimination of its remaining nuclear facilities. Iran refused all three.

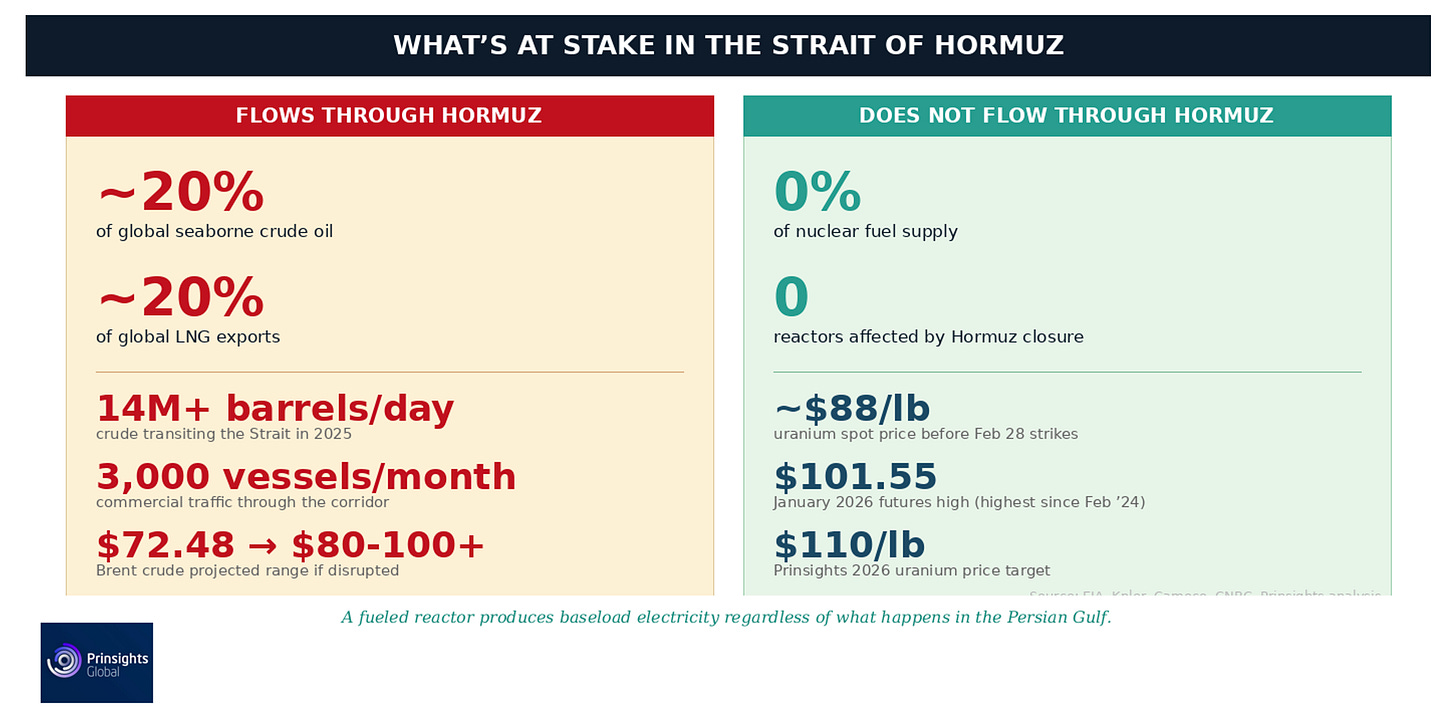

The obvious ramification stemming from the stalemate is energy disruption. That’s because the Strait of Hormuz carries roughly 20% of the world’s seaborne crude oil and a fifth of global LNG exports.

If the Strait stays closed, the world’s spare production capacity, nearly all of it sitting in Gulf states on the wrong side of Hormuz, gets sealed off with it.

But the reality is that the oil story will fade when the Strait reopens. Meanwhile, the structural commodity supply chain deficit story won’t. The U.S. just deployed significant military resources, both in dollars and defense supply buildups, to work to destroy uranium enrichment infrastructure abroad while remaining deeply dependent on adversarial nations for its own civilian nuclear fuel supply at home.

The Lingering Supply Chain Contradiction

Russia’s Rosatom still controls roughly 40-45% of the world’s uranium enrichment capacity. Kazakhstan, a largely Russian-allied state, is the world’s largest uranium producer. Together with Uzbekistan, these three countries account for a commanding share of the global primary supply. It’s the same structural vulnerability we detailed in our February rare earths research. That’s because, while it might be a different commodity, what we’re seeing is the same playbook. The West has outsourced the majority of its critical fuel supply to geopolitical rivals and is now scrambling to rebuild domestic capacity.

As we’ve pointed out, the difference is that uranium now has direct policy momentum behind it, and the pace is rapidly accelerating because of legislation and White House directives – along with catalysts like licenses restructuring and funding initiatives.

In our 2026 commodities outlook, we ranked uranium second on our list of assets with upside momentum this year and set a price target of $110 per pound.

The developments since have only reinforced this.

Here’s where the uranium structural story connects to the strikes that began on February 28 directly. More than 80% of Iran’s oil exports went to China, averaging roughly 1.38 million barrels per day, in 2025. If the Strait of Hormuz is disrupted for a sustained period, China’s energy supply can take a direct hit. This matters because China also controls the rare earth supply chain that the West is determined to break free from.

This pressure on Chinese energy imports will only strengthen China’s incentive to weaponize its own supply chain leverage in response, or at the very least, work to harden it. That’s why the rare earth and uranium stories are not separate. They are two fronts of the same strategic standoff, as we detailed in the February Pulse Premium issue last week.

What Investors Should Watch

Over the weekend, oil, gold and silver dominated the headlines, with oil as the obvious disrupted commodity. Meanwhile, gold and silver will likely continue to rally on the back of safe-haven trading.

Yet nuclear energy doesn’t need to flow through the Strait of Hormuz. The same is the case for uranium fuel rods that don’t need to sit on tankers waiting for Iranian naval clearance. A reactor that’s fueled and already operating can produce baseload electricity regardless of what’s happening a world away in the Persian Gulf. That’s precisely the logic that should be driving the U.S. nuclear buildout – and why every escalation in the Middle East only strengthens the long-term case for domestic nuclear energy and the fuel supply chain behind it.

Uranium spot prices had already risen to $88 per pound before the February 28 strikes, which was down from futures briefly touching $101.55, the highest level since February 2024, and the end-of-January spot price was sitting at $94.28. Yet, the structural deficit hasn’t changed. What has changed this weekend is the geopolitical urgency surrounding it.

We’ll continue watching the uranium market closely when it reopens. For now, the takeaway is that the events starting on February 28 did not create the investment thesis for domestic uranium and nuclear energy, but they accelerated it. The acceleration is happening on a timeline that was already moving faster than most investors had priced in.

Comments

Log in or sign up to join the conversation.