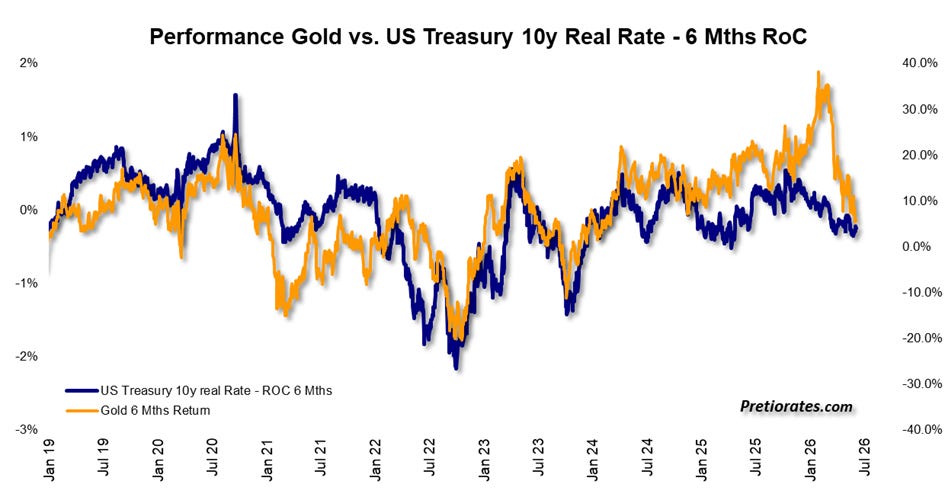

The real market return—typically calculated as the yield on 10-year U.S. Treasuries minus the inflation rate (i.e., the CPI)—continues to show a very high correlation with the price of gold, as measured by the percentage change over the past six months. This confirms our view: interest rates play a very significant role in the gold market. And not just since the outbreak of the Iran war.

In fact, it has become clearer again since the start of the Iran war: higher oil prices fuel inflation fears, which in turn drive interest rates higher. A chain reaction that doesn’t exactly bode well for precious metals.

The stock market has so far weathered these fears and higher market yields remarkably well—the S&P 500 Index has just reached a new all-time high. Behind this, however, lies a healthy dose of confidence that the problem in the Strait of Hormuz will soon be resolved. Then the many tankers blocked in the Persian Gulf could finally resume supplying the global market. The price of oil would fall again, and with it, inflation fears and interest rates.

That sounds like a very nice idea. But there are other factors influencing the development of U.S. interest rates. The U.S. economy itself, for example. When the economic engine is humming, interest rates usually rise as well.

In the high-tech sector, business continues to thrive—thanks to AI. The virtually immeasurable investments in the high-tech sector now account for a significant portion of U.S. GDP. Other sectors are also benefiting from this: utilities, mining companies, and other suppliers to the digital gold rush. With fossil fuel exports from the Middle East blocked, the U.S. has also emerged as an energy powerhouse, much to the delight of the major U.S. energy companies.

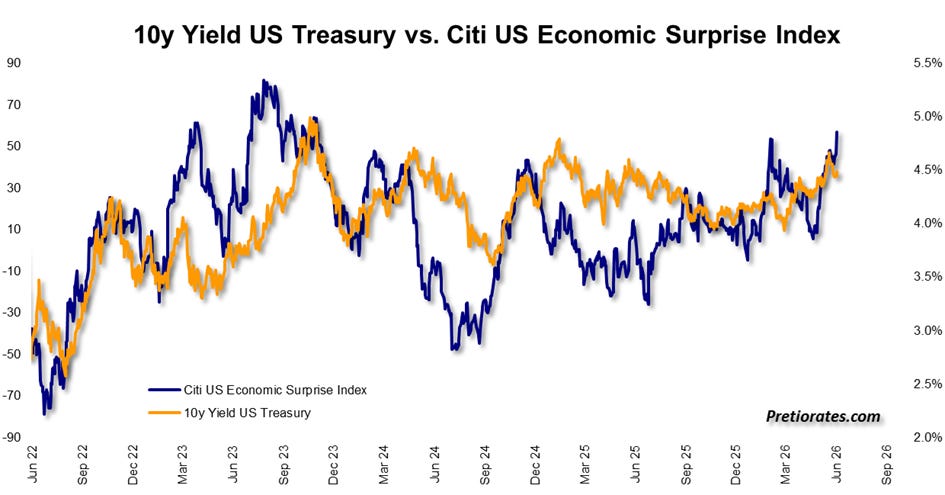

In fact, the latest development in the Citi U.S. Economic Surprise Index shows that recent economic data has almost without exception come in better than expected. This pushes market yields higher and doesn’t bode well for precious metals.

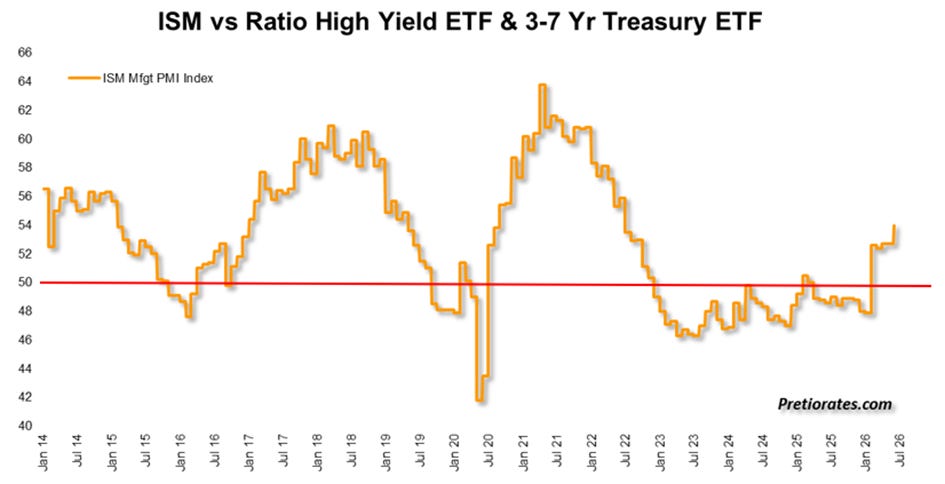

But it wasn’t just the Citi Surprise Index that delivered a strong surprise recently. The ISM Manufacturing Index, released on Monday, has also made a significant jump above the critical 50-point mark in recent months and now stands at 54 points. When this index is above 50, it signals growth in the U.S. economy. Below 50, the outlook is less favorable.

An end to the Iran conflict does not necessarily have to lead to falling market yields. With the strong U.S. economy, there is a factor that should not be underestimated and that could prevent the Fed from cutting interest rates. A strong U.S. economy also usually leads to a stronger U.S. dollar.

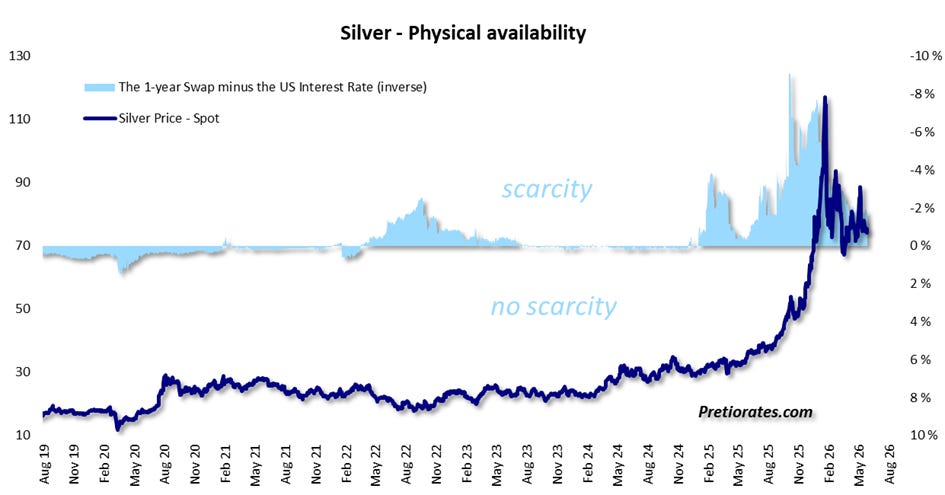

For gold and silver prices, this is, of course, anything but supportive. The consolidation has now lasted over four months and is testing the patience of gold and silver investors. In fact, the situation in the silver market has long since fully normalized: as recently as the turn of the year, there was far too little physical silver in the market. Currently, this no longer appears to be an issue.

Even when investors lend out their physical holdings, they no longer earn much from it. After the lease rate briefly exceeded 30% at the end of the year, it has since returned to its usual long-term level of just under one percent. So the former silver fever has cooled back down to a lukewarm room temperature.

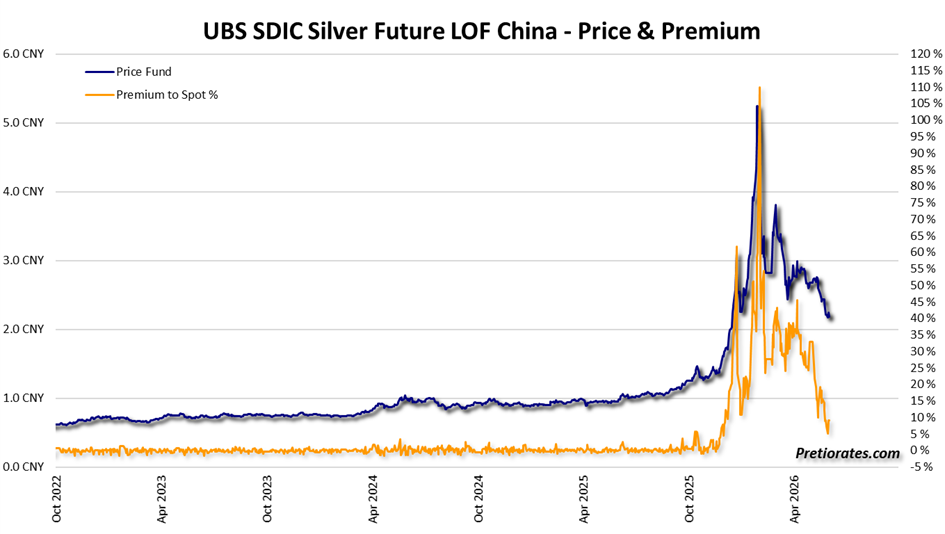

Even in China, the picture is similar: Chinese investors have only one silver ETF at their disposal. After a premium of over 100% was paid at times for the silver held in this ETF—and the ETF manager himself had to warn against further investments—this premium has since settled back down to well below 10%.

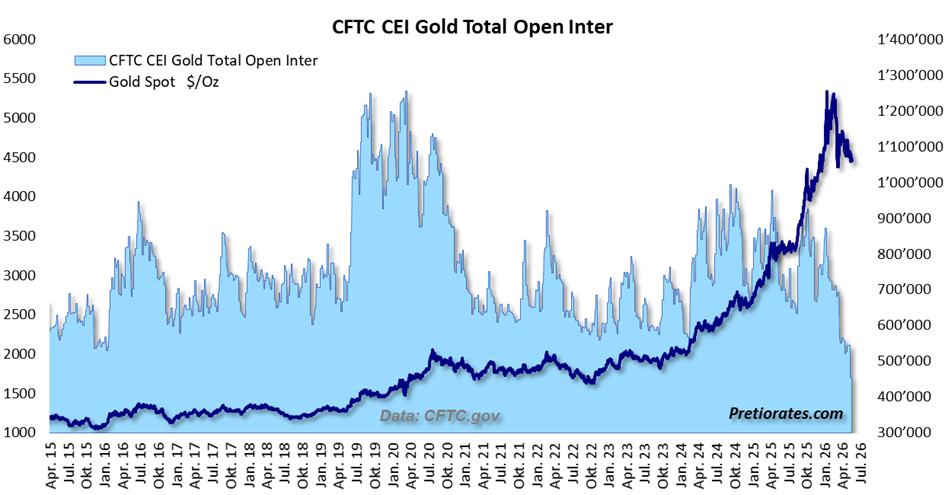

It thus appears that the bullish days for gold and silver are over. In fact, many market participants have already turned away from the two precious metals. Open interest shows how many futures contracts are open across all maturities. For gold, this figure has recently fallen to 455,000 contracts. The increased margin requirements in recent months are likely partly responsible for the lower number. We have now reached the lowest level since 2008.

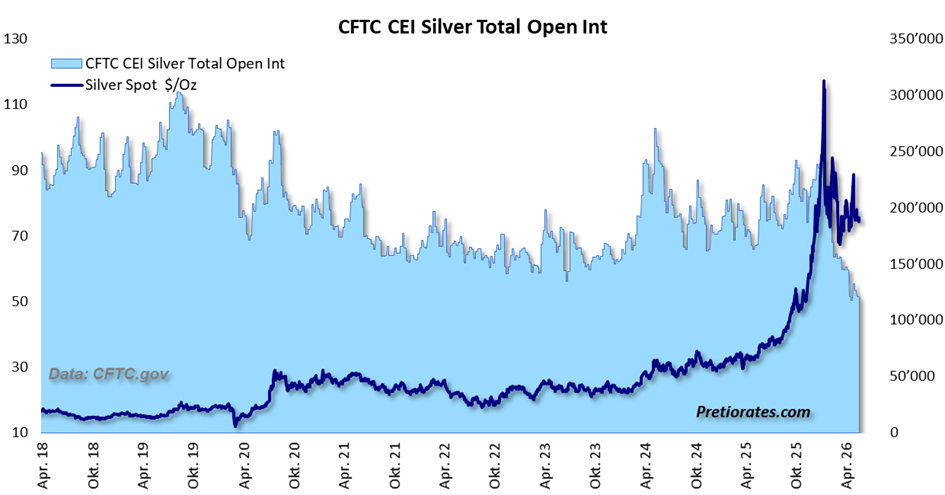

The same picture emerges for silver futures: Open interest has now fallen to just under 120,000 contracts—the lowest level since 2009. It certainly seems as though investors have given up on this market. Lights out, doors closed; the silver bugs appear to have lost their optimism.

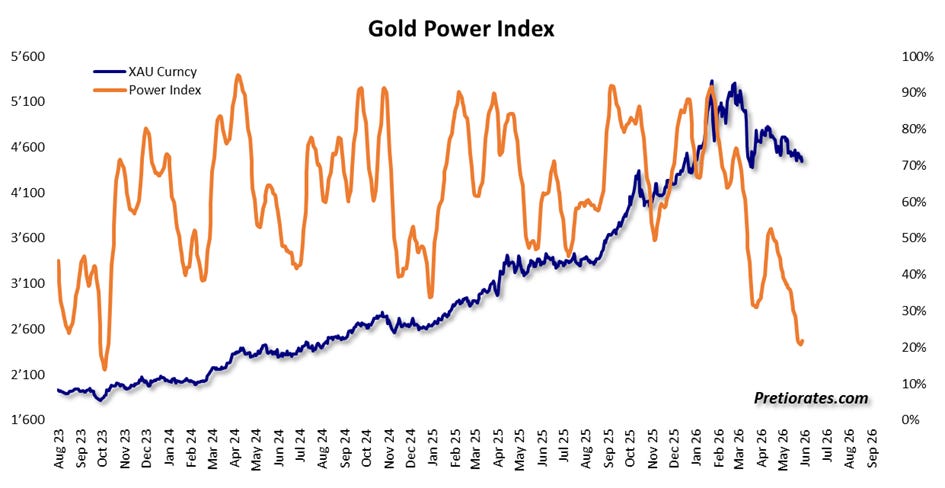

But whenever interest in an asset class is particularly low, contrarian investors’ interest rises. In fact, gold’s Power Index has also fallen to its lowest level since October 2023. October 2023—that rings a bell, doesn’t it? Oh yes, that’s right: that’s when the gold price began to rise at a significantly faster pace. So don’t give up too soon…

Comments

Log in or sign up to join the conversation.