The Federal Reserve’s FOMC voted to keep its target range at 3.5% to 3.75% this week, in a unanimous vote. Notably, it was the first time the FOMC had voted without any opposition in a year. And while the Fed Chairman Kevin Warsh was never going to open his time as chair with a rate hike, the front end was already priced for patience.

The decision itself was the least interesting part of the meeting. The place to watch moving forward was what Warsh indicated about inflation, liquidity and how much support the Fed is still willing to provide Wall Street beneath the surface.

Warsh claimed that he is still concerned about inflation, emphasizing that the Fed "will deliver price stability." Yet he wants to see changes at the central bank, with more selective data and targeted analytics, before the Fed changes course.

The new Fed chair also refused to submit any projections for the widely-followed “dot plot,” which serves to offer general guidance over where the policymakers at the Fed might be headed.

The reluctance only added to the questions over what the path forward could be for rates. That move keeps the Fed in a holding pattern that hasn’t ended with a total shift away from Powell’s leadership.

Video Length: 00:07:46

Instead, it acknowledges the inflation risk without forcing a move, which is the bind he is in. To be sure, inflation has risen since the Iran war broke out, with May CPI levels hitting 4.2%, resulting in the fastest pace in three years along with a U.S-driven ceasefire that may take some pressure off oil for now.

The reality is that holding rates steady, hiking them, or buying bills will not create supply-chain stability. Yet, the market is still sensitive enough that one hawkish sentence from the Fed can set off another round of forced selling.

Today and moving forward, the tightrope Warsh has to verbally walk is to sound vigilant about inflation without signaling that the support the market is leaning on is about to be pulled.

And while the financial media might be focused on Warsh’s vow to revamp how the central bank does its job, it did little to shed light on his plan for how to bring inflation down.

The Front End Was Not the Test

The federal funds rate is the most visible part of the Fed’s monetary policy. That is where the headlines are focused and what most of the markets track. Yet the front end is only part of the story.

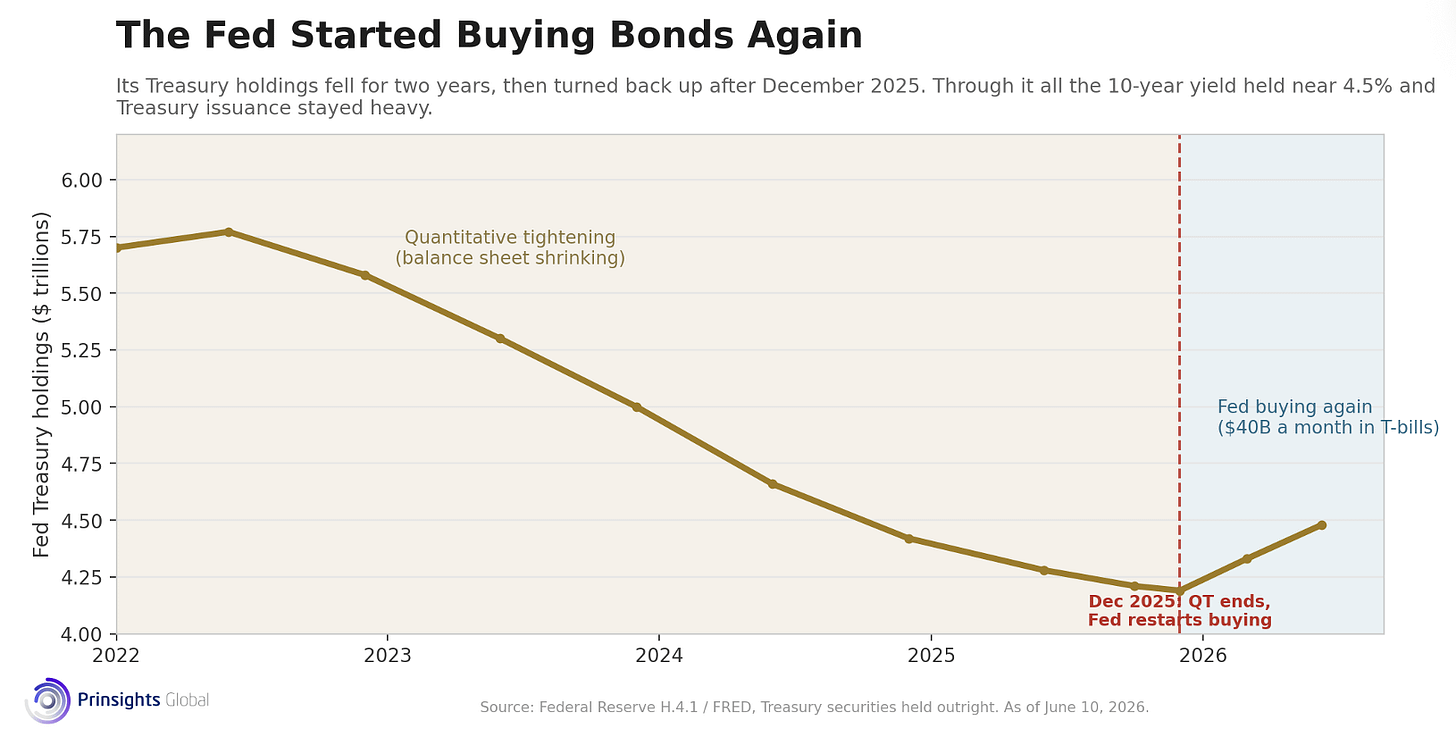

The real issue is how the Fed uses its balance sheet to manage liquidity beyond the rate line. The U.S. central bank ended its quantitative tightening (QT) on December 1, 2025, after shrinking its holdings for more than two years. Eleven days later, on December 12, it started buying Treasury bills again, initially about $40 billion a month, under a program it calls “reserve management purchases.”

The Fed calls it reserve management. I call it QE. The label does not change the effect.

The Fed’s balance sheet is growing again. Its Treasury holdings stand at about $4.48 trillion as of June 10, up by more than $200 billion since the buying began in December.

What you should know is that it is not buying the 10-year note directly from the U.S. Treasury through this program, but through open market primary dealers and the secondary market. That distinction matters. The purchases still put reserves back into the banking system and ease short-term funding costs, even as the government keeps auctioning heavy new supply across the curve. So far, the 10-year yield has held near 4.5% even as that supply keeps coming.

But, as most things in life, there is always a catch. The Fed front-loaded that buying, running $40 billion a month from December through mid-April to get ahead of the spring drain on bank reserves, then cut the pace to $25 billion and now about $10 billion.

So, the support that helped keep Treasury-market pressure contained is already fading, right as Warsh takes hold of the chair position he coveted. Whether that taper keeps running or the Fed steps the buying back up is his first real balance-sheet test. And it will be one that market watchers, talking heads on the financial networks and leaders throughout the halls of the White House are all paying close attention to.

Why This Matters for Hard Assets

As Prinsights detailed on Monday, certain hard assets have sold off because of liquidity pressure, fund redemptions, algorithms, and paper-market stress, all related to war, inflation and anticipation of the new Fed chair’s impact, but not because the physical supply and demand realities.

Even with this week’s data, including the FOMC’s results, and some positive Iran war developments, the fact remains that volatility and fiscal realities are in play and can periodically run in opposition to each other.

The Fed can choose to try to ease inflation pressure through rate decisions, but its balance sheet is a bigger tell for the long-end, U.S. debt and debt servicing burden.

Meanwhile, gold, silver, copper, uranium, and rare earths each react differently to Fed policy, despite the fact that none of them can be created by it.

The metals that took the worst of the selloff have already started to bounce as war tensions began to let up, with their oil and inflation pressures letting up with them. Instead of getting caught in the noise though, the signal is that those moves offer the clearest signal yet that the drop was about sentiment and liquidity, not a break in the physical setup.

What the Fed Still Cannot Print

That’s why the FOMC under Warsh can hold the front end steady for now. And Warsh can move future expectations with a sentence or his tone. Meanwhile, the Fed can buy Treasury bills, manage liquidity and reserves, talk about inflation and the data, and put pressure on the dollar and the 10-year.

Yet it cannot print commodities, magically fix supply chains or dictate geopolitical outcomes. That was the limit former chair Powell never fully understood or accepted.

Comments

Log in or sign up to join the conversation.