Remember when late-night TV used to be funny and entertaining? In 1962, Johnny Carson began a 30-year run as host of the Tonight Show. Millions of Americans tuned in nightly for late-night entertainment before bedtime, and Johnny delivered.

Sadly, current late-night TV is generally unfunny, hateful political trash and much of America ignores it. No one I know wants to head off to bed angry!

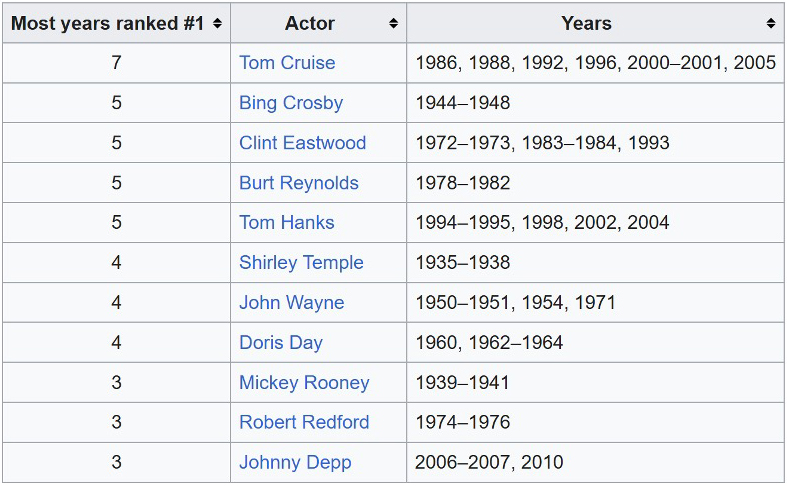

Many of Johnny’s shows and guest appearances are still legendary. One I have never forgotten is an interview with Burt Reynolds. Reynolds did well in the Top Ten Money Making Stars Poll, which determined the bankability of movie stars. He still ranks high today:

Johnny started the interview discussing the money movie stars were being paid and how lucky they were to be in such a financial position. Burt recounted the dinner when he was offered his first starring role. They offered $10 million. Burt explained he was immediately on the floor, hyperventilating. He was overwhelmed; what happened was beyond his wildest dreams.

The discussion about wealth that followed was something most people would only dream about- what things incredible money could buy – yachts, planes, mansions, you name it. In typical Johnny Carson fashion, he concluded with something down to earth,

“The main benefit of having money is not having to worry about money!” |

As I progressed through the next several decades, like many, I’ve fantasized about what we would do if we won the lottery. Yachts, jets, homes, fancy cars – dreaming about all the things that having a lot of money would buy.

Now, in my mid-80’s, my perspective has changed – a lot. Living in the world’s largest retirement community, we are surrounded by thousands of seniors really enjoying life while living in homes they would have once called “starter houses.” Many travel regularly, eat out frequently, and certainly don’t seem to be worrying about money.

World Population Review tells us, “The Villages’ average per capita income is $30,806. Household income levels show a median of $77,622. The poverty rate stands at 4.69%.”

In 2024, Forbes explained What It Means To Be Wealthy In The U.S.:

“The Census Bureau put the average American household income at $80,610 from 2023 figures, and to be in the top 20% of income, you’d have to earn almost double the average, bringing in an income of above $130,500 a year.

To be considered a really top earner in the U.S., we could take the IRS’ benchmark on what the top 1% of Americans earn—above $540,009 puts you in the top 1% of earners from a tax perspective.”

Stuff versus peace of mind

It took me decades to fully grasp what Johnny Carson meant. I’ve had my share of cool things, cars, boats, homes and even a plane. While they were fun, I still had to pay for them. The ultra-rich can own those assets and have so much left over they don’t have to worry.

Our lifelong journey provides many choices, one being expensive stuff versus peace of mind and sleeping well at night. You can have both, to a degree, if you do the right things along the way.

Here’s 8 of the habits we’ve learned about how regular middle-class folks managed to become wealthy enough to retire without constant money worries.

Set priorities. The single best advice I ever received was the old axiom, “Pay yourself first, and learn to live on the rest.”

Before the days of 401k-type retirement plans, many people had to save for their retirement in after tax dollars – quite a challenge. Like many, I went through the “buy now, pay later” phase where every raise I received was at in terms of monthly payments. Too many times, money burned a hole in my pocket, and I spent it. I had to do something different.

My compensation plan helped me make a transition. In addition to a monthly salary, each quarter I received a performance-based commission check. I forced myself to save by taking ½ of each commission check to pay down our mortgage. I was saving in a manner that didn’t allow me to easily buy more stuff.

In today’s world, I’d go further with the axiom. With the 401k-type programs, make it automatic so you never see the money. Maximize your contribution each month. The earlier the better as compounding over decades creates amazing results.

Get out of debt. For years, brokers touted getting rich using other people’s money. That’s how bankers get rich, renting out other people’s money.

A recent Employee Benefit Retirement Institute (EBRI) study reported:

“Debt remains a major obstacle, especially for workers. Sixty-five percent of workers said debt is a problem for their household, and one-quarter described it as a major problem. Half of workers have credit card debt, and nearly 1 in 3 have more than $25,000 in non-mortgage debt. About 3 in 5 workers and 3 in 10 retirees said debt negatively affects their ability to save for or live comfortably in retirement.”

Our recent Visa statement required a minimum payment of 1% of the outstanding balance. Credit card interest rates average 24% annually. Pay it off monthly or you are going down the drain quickly.

Live below your means. If you are in debt, you have lived beyond your means. To get out of debt, and accumulate wealth, you must reverse the process. Credit card and non-mortgage debt is a good place to start.

Stick to a realistic budget. Budgeting is difficult, particularly in the early stages. Commit to living within the guidelines. All too often we pay too much attention to “the emotional perspective of the moment.” “Screw it, I deserve it!” becomes very expensive, and can set you back for years.

Make the time for financial education. The first step is understanding the basics, money, interest, debt, and investing. This is often misunderstood. Abdicating the responsibility for managing your wealth to a broker is fraught with risk. If they make a mistake, they lose a client – while the client can lose much of their life savings.

Don’t be talked into investing into anything you don’t understand.

Understand appreciation, depreciation and spent. I’m appalled by a recent credit card commercial. A young woman, frustrated by the winter weather, dreams of nice, warm sunny beaches. Using her credit card, she takes a luxury vacation and heads to the Caribbean – buy now, pay later. Unless she has the ability to pay off the vacation immediately, by the time she adds the interest it was a very expensive getaway.

When my children were young, our only family vacation time was around the Christmas Holidays. I was very tired, had a good year, and called a travel agent. I surprised the family; the day after Christmas we headed to the Bahamas for a couple weeks. It was fun, but very expensive. My justification was we all deserved it!

Soon after, a loving mentor sat me down and explained the difference between appreciation, depreciation and spent. He began with the idea that I spent the money for the Bahamas trip, it was gone – a nice memory. The sun tan quickly faded away.

Using a motor home as an example, he explained the difference between depreciating and appreciating assets. Assets that appreciate were much more appealing; your money is working for you.

We investigated buying a small condo in the Florida Keys. The down payment was less than I spent on our Bahamas vacation. I could afford the monthly mortgage payments and investing in an appreciating asset. In a nutshell, the amount we spent for family vacations didn’t change much, but it was spent on an appreciating asset. We had many fun vacations in the Florida Keys and finally sold the condo when the kids were out of school, more than doubling our money.

Review and adjust when necessary. This works both ways. If your savings and investments didn’t do as well as planned, the sooner you make adjustments the better.

On the flip side, things can also go better than planned. Jo and I owned boats and toured the country several times in a motor home. Yes, they were depreciating assets; however, only after maximizing our retirement contributions, then double checking the numbers, did we make the decision that we could afford to further enjoy the fruits of our labor. The old saying, “The two happiest days in a boat owner’s life is the day he buys it and the day he sells it” is absolutely true.

Keep a realistic perspective. The goal isn’t to accumulate stuff and win the “keeping up with the Joneses battle.” If you can afford the yachts, jets and luxuries, good for you. George Carlin warns:

“We have multiplied our possessions but reduced our values. We talk too much, love too seldom, and hate too often. We’ve learned how to make a living but not a life. We’ve added years to life, not life to years.”

Don’t lose sight of the goal – accumulate enough income generating wealth to be able to enjoy your golden years without constantly having to worry about money.

Your neighbor, who also dines out regularly, may also be sleeping without financial worry every night, without owning all the luxury toys. Johnny Carson was right; it’s not the accumulated stuff; but rather the ability to enjoy life with minimum stress that really matters.

On The Lighter Side…

Memorial Day weekend in Jo’s hometown is Alumni Weekend. It began Friday night with a big get-together at the American Legion, Saturday the banquet, followed by a Sunday morning brunch.

The class of 1976 had a big shindig, celebrating their 50th reunion. This year is Jo’s 60th. Those around Jo’s table lamented how quickly the last ten years flew by. Lots of laughs; the hugs and warmth are very special. Many nice people enjoying life and each other’s company. I appreciate them making us “non-classmates” feel like part of the family.

Jo and I chuckled to ourselves. 20 years ago, after the banquet, we went to the street dance and stayed out late. 10 years ago, after her 50th reunion, we went to a house party. This year, after the banquet, we went home…. The joys of aging!

Quote of the Week…

“If plan A fails, remember there are 25 more letters.” —Unknown

And Finally…

Lifelong friend Tom G. shared some “petrol pump wisdom,” apparently supplied by a Johannesburg, South Africa filling station:

|

|

|

|

|

|

|

And my favorite:

|

Until next time…

Comments

Log in or sign up to join the conversation.