.jpg")

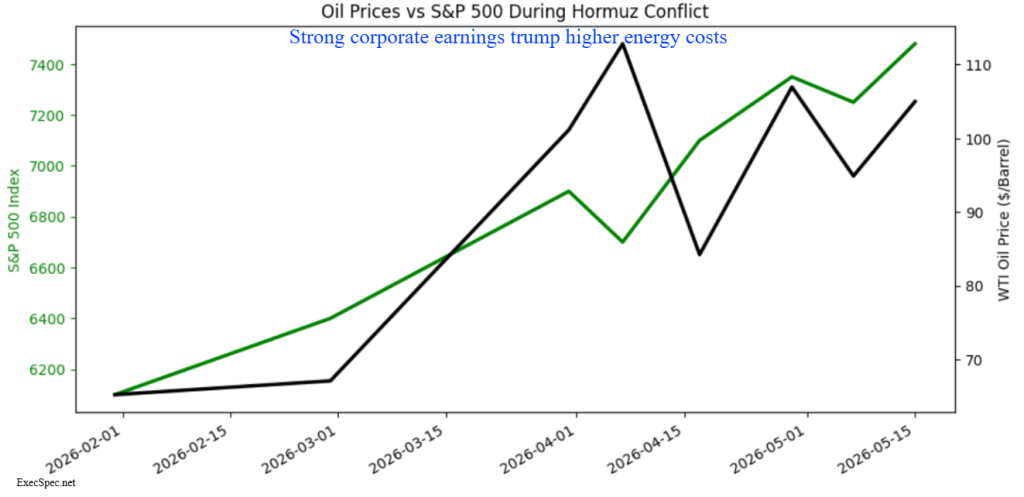

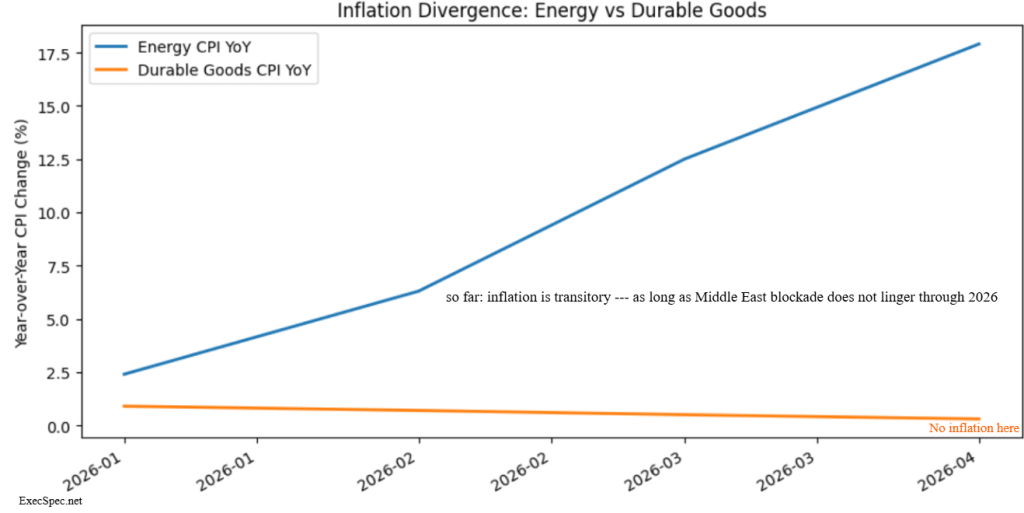

Wall Street’s capacity for selective hearing remains one of modern finance’s most reliable constants. Oil remains above $100 a barrel ($105 today). More than 10% of global oil production and export flow has now been disrupted or stranded by the widening Iran conflict and the continuing paralysis of the Strait of Hormuz. Inflation has jumped to 3.8%, the highest since 2023, while energy prices are up 17.9% year over year. Yet investors continue behaving as though this entire affair is little more than an inconvenient summer thunderstorm interrupting an otherwise cloudless secular Bull market.

For now, the market’s verdict is unambiguous: this inflation shock and idled energy flows are still being treated as transitory. Transitory became a bad word when Fed Chair Powell used it during the Biden inflation spike of 2021 and 2022, but there is evidence supporting that optimism. Core inflation is still far below the headline number, and durable-goods inflation remains tame enough to suggest that the energy shock has not yet metastasized into a full 1970s-style wage-price spiral. New vehicles, communication, and medical care were among the categories that declined in April, even as fuel and transportation costs surged.

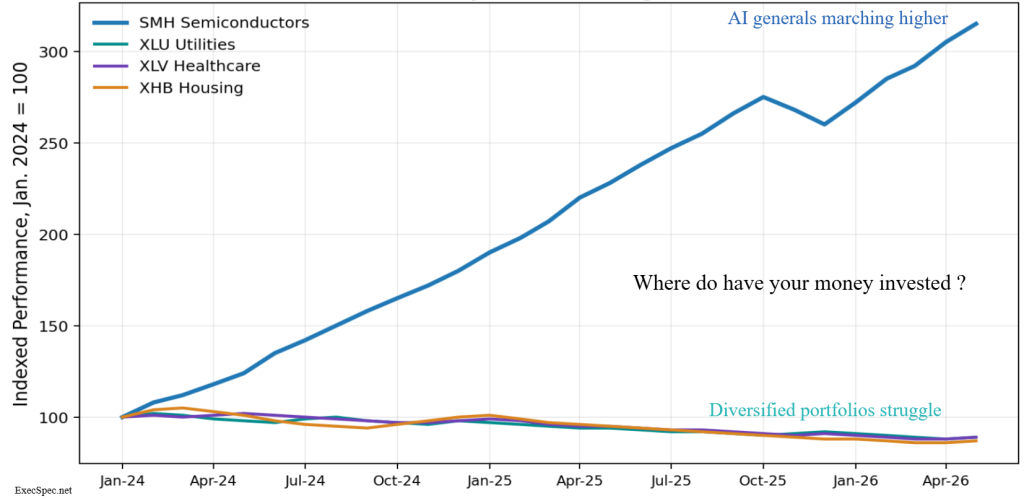

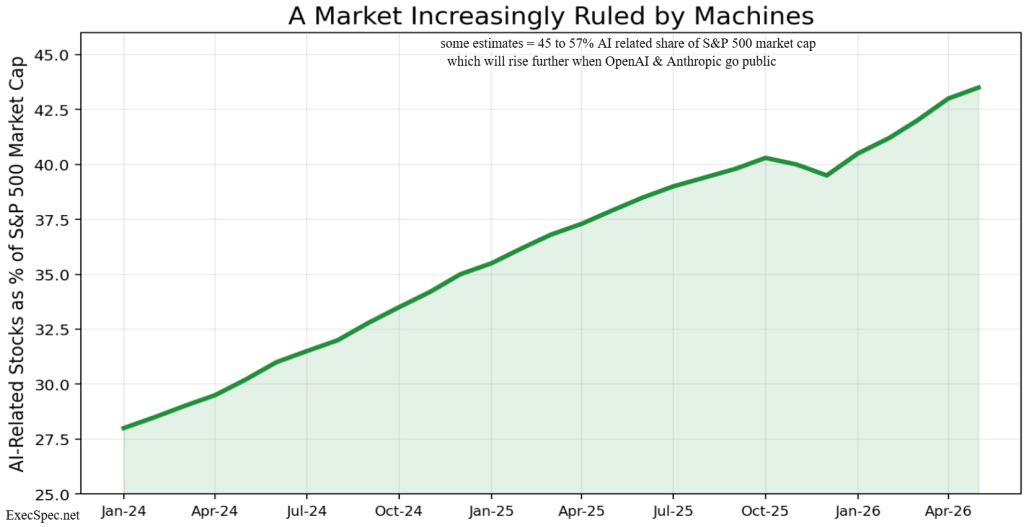

The stock market’s internal arithmetic reveals the strangest feature of this Bull market: narrowness. The cumulative line of advancing minus declining issues on the broad New York Stock Exchange is lagging the more tech heavy S&P 500 (SPY) and Nasdaq (QQQ) that keep pushing to new highs. Large-cap technology rockets higher while much of the average stock drifts sideways or lower as investors embrace the mantra that the future is artificial intelligence.

Semiconductors, memory producers, data-center infrastructure providers, power-management firms, cooling specialists, fiber-optic suppliers, and electricity enablers continue to absorb an outsized share of global investment capital. The market increasingly resembles a digital gold rush where only the shovel makers, railroad owners, and explosives suppliers matter.

Meanwhile, large portions of the market quietly retreat. Utilities have weakened under rate pressure. Healthcare continues to lag. Housing struggles beneath elevated mortgage rates. Traditional energy shares — paradoxically — have failed to fully capitalize on triple-digit oil because investors continue to believe today’s shortage is temporary rather than structural.

Yet despite narrow participation, the Bull case remains persuasive because earnings are doing the heavy lifting. FactSet reports that 89% of S&P 500 companies have reported Q1 results, with 84% beating EPS estimates — the highest beat rate since Q2 2021 if sustained. Companies are beating estimates by an aggregate 18.2%, more than twice the 5- and 10-year averages. Q1 blended earnings growth has jumped to 27.7%, up from only 13.1% expected at quarter-end.

This is not a market rising on vapor. It is rising on earnings.

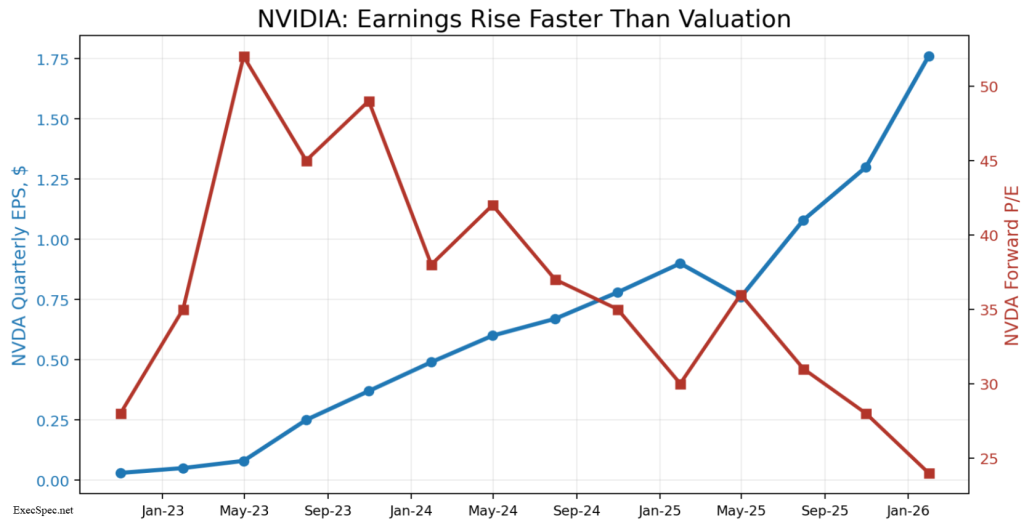

The Information Technology sector is reporting 50.7% year-over-year earnings growth, with semiconductors and semiconductor equipment up 99%. FactSet notes that Nvidia (NVDA) and Micron (MU) are the largest contributors to technology-sector earnings growth; without those two, the sector’s earnings growth would fall from 50.7% to 28.5%.

That is narrow, yes. But narrow does not mean irrational exuberance.

Nvidia’s forward P/E recently stood near 24.4, below the semiconductor industry median of 32.7, despite the company’s dominant AI position and exceptional earnings growth. Micron’s forward P/E was even more striking near 7.8, roughly 76% below the semiconductor industry median, even after a spectacular stock advance.

In other words, these stocks have not merely risen because investors have lost their minds. Their earnings have risen faster than their share prices. Multiples have compressed even as business momentum has accelerated. In a rational market, companies growing far faster than the average stock should command premium multiples. Instead, some of the AI leaders still trade at average or below-average forward valuations relative to their own industry.

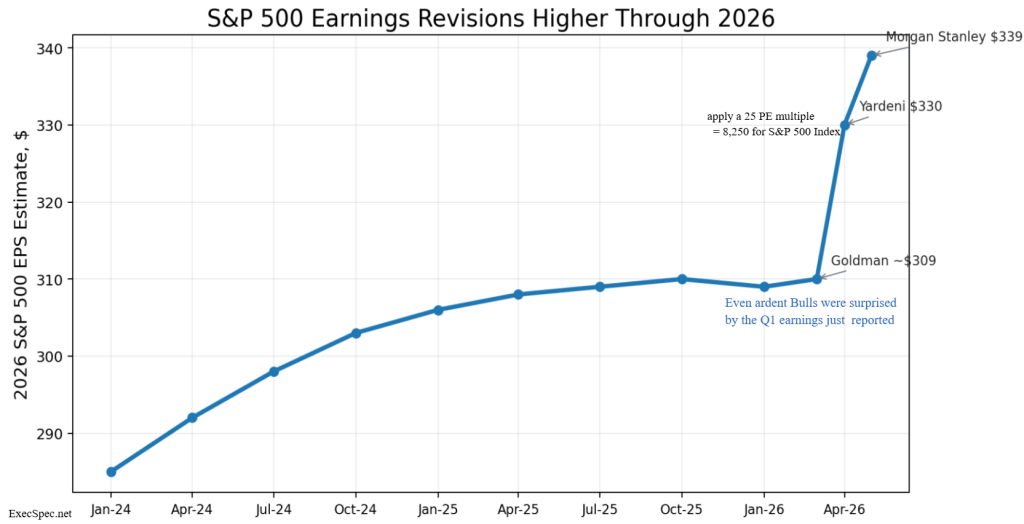

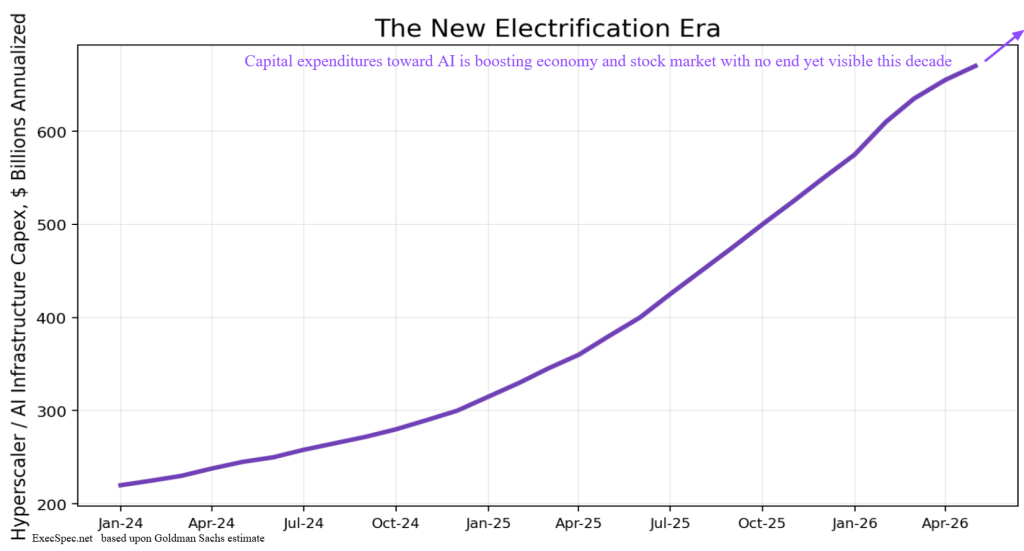

This is why S&P 500 targets keep rising. Goldman Sachs recently projected the S&P 500 at 7,600 by year-end and estimated that AI investment could drive roughly 40% of S&P 500 earnings growth in 2026, with major cloud companies planning about $670 billion in capital spending (likely to be revised higher). More bullish strategists are now discussing the 8,000–8,300 zone as earnings assumptions rise alongside the AI buildout.

Now enters another geopolitical variable that markets are beginning to interpret not as risk, but as opportunity.

President Trump’s visit with Xi Jinping in China carries an unusually visible corporate entourage — a modern commercial armada. Accompanying Trump are many of America’s most powerful chief executives, whose combined public and private market value approaches $19 trillion. It is less a trade delegation than a floating board meeting of the American economic empire.

Both nations can present the imagery favorably. China seeks respect and acknowledgement of its centrality to global commerce. The United States seeks leverage — industrial, technological, agricultural, and financial influence gathered into one negotiating bloc aimed at reopening markets and reshaping supply chains. Promises have already emerged to buy 200 Boeing (BA) planes (potentially 750) and U.S. soybeans and vital rare-earth exports are rising slowly, which add up to a modest tailwind for global growth and sock investors.

Against this optimism sits the increasingly unstable Persian Gulf.

Investors have become remarkably desensitized to the Iran conflict despite mounting evidence that the blockade may endure longer than expected. Shipping disruptions persist. Energy costs remain elevated. Inflationary pressure continues leaking into financing costs and industrial inputs. Yet markets continue to discount the future recovery rather than the present disruption.

This, too, is rational. The moment the Strait meaningfully reopens and tanker flows normalize, inflation expectations will cool rapidly. Oil prices would retreat. Bond yields will fall anticipating the Federal Reserve’s latitude to ease rates. A second-leg expansion in earnings and valuation multiples would emerge almost immediately. It’s difficult to say when a protracted lockdown of 10% of the global energy flows in the Middle East will begin to severely impact the economy and earnings.

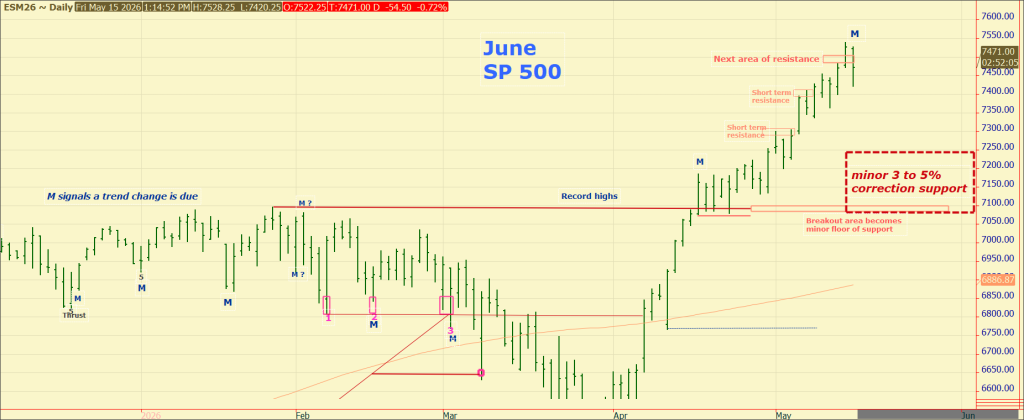

For now, the path of least resistance remains higher, even if punctuated by sharp and emotionally violent corrections. Those corrections should increasingly be viewed as opportunities rather than warnings in a world where AI demand continues vastly exceeding supply. The greater long-term risk to this Bull market is not recession, but eventual overcapacity — the day supply finally catches the extraordinary appetite for compute power, memory, electricity, and digital infrastructure.

That day will arrive eventually. But it does not appear imminent.

Until then, investors continue to ride a remarkably narrow but extraordinarily powerful wave — one propelled by silicon, electricity, diplomacy, and the persistent belief that today’s inflationary storm will eventually pass like ships once again flowing freely through the Strait.

Comments

Log in or sign up to join the conversation.