My Atlanta Braves are sitting atop the National League East right now, just ahead of the Phillies.

And here's the thing about a team in first place this deep into the season: everybody wants to talk about the big home run hitter, the flashy strikeout pitcher, the highlight reel play. But the teams that actually win divisions usually do it because of what's happening in the background.

The bullpen nobody talks about... The bench player who keeps grinding out tough at-bats... The unglamorous stuff that doesn't make SportsCenter...

(Speaking of the Braves, I may have picked up tickets to a game next week as a surprise for Angela. Angela, if you're reading this, I'm sorry for spoiling my own surprise 😆⚾🧢.)

I bring this up because the same thing just played out in the market this week, and almost nobody's talking about it the right way.

Everyone wants to talk about AI winners in terms of chips and hyperscalers. Nvidia, Alphabet, the usual names making headlines every single day.

But this week, some of the biggest AI-driven earnings beats came from a place most investors aren't even looking. The banks.

The Real AI Winners Don't Make Chips

Goldman Sachs and JPMorgan both posted record quarterly revenue this week, and the AI boom is a huge reason why.

Goldman's revenue jumped 39% to $20.3 billion. JPMorgan was up 27% to $58 billion. These aren't small beats. These are the kind of numbers that would normally be the headline of the week on their own.

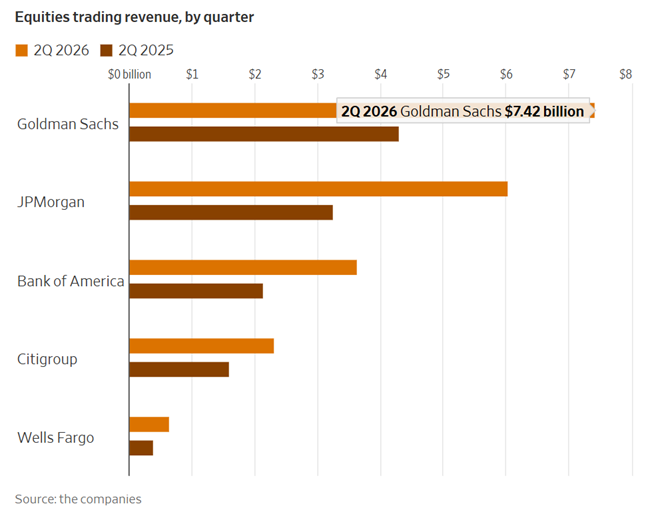

Here's where it gets interesting. Equities trading revenue was up 86% at JPMorgan, to $6 billion. Goldman's equities trading revenue jumped 72%, to $7.42 billion. Bank of America saw equity trading revenue climb 70%, to $3.6 billion.

This isn't just "the market went up so trading was good." This is a genuine surge in capital markets activity, and AI is the thread connecting almost all of it.

Think about everything that's happened in just the last few weeks:

The SpaceX IPO, one of the biggest ever.

Alphabet raising $90 billion through an equity issuance.

Active M&A, including Dominion Energy's sale to NextEra.

Goldman was the lead advisor on both the SPCX IPO and the Alphabet raise.

That's not luck. That's a bank sitting at the center of the biggest capital-markets moment in years, collecting fees on nearly every major deal tied to it.

There's also something happening inside the banks themselves. One Bank of America executive put it simply this week, noting that AI is helping streamline how the bank actually operates.

So it's not just that AI-related companies are raising money and trading actively, it's that the banks are using AI internally to do more of it, faster.

So here's my takeaway:

When you think "AI trade," widen the lens.

It's easy to only look at who's building the infrastructure. It's just as important to focus on who's financing it, who's advising it, and who's making a market for it.

This week, that group quietly outperformed a lot of the flashier names getting all the attention.

Speaking of Focus

I had an eye doctor appointment on Tuesday, and it turns out my contact lens prescription needs an update. Nothing dramatic, just enough blur that I hadn't noticed how much I'd been squinting to make things clear.

That's actually a pretty good way to think about this week's CPI report.

The headline number is easy to see. Inflation came in negative for the month, well below expectations, and well below last month's pace. On the surface, that looks straightforward. Good news, full stop.

But like my old prescription, the surface reading doesn't quite bring the full picture into focus. Here's the context that matters.

Bespoke Investment Group has pointed out something worth remembering. Negative CPI reports that happen outside of a recession have historically tended to be good for the market. That might sound counterintuitive, so let me explain why.

Negative inflation readings are often a warning sign when they're tied to weak demand, consumers pulling back, businesses cutting prices because nobody's buying.

That kind of negative CPI print usually shows up alongside a slowing economy, and it's a real concern.

But that's not really what happened here.

This pullback was tied to a supply-side factor: falling energy prices, as oil retreated from its highs during the Iran conflict.

That's a very different story than weak demand.

In fact, much of the recent data I'm seeing about the consumer right now, (like retail sales and personal spending) continues to look resilient.

According to Bespoke's historical data, the market has tended to perform well in the six and twelve months following this specific kind of print, precisely because it isn't a symptom of a weakening economy.

There's also a Fed angle here. Lower inflation makes near-term rate hikes less likely, which removes one of the bigger overhangs the market's been dealing with.

Now, I'll add the same caveat I mentioned earlier this week. A lot of this relief came from energy prices that I don't think are as sustainably low as they look right now.

That's a conversation for another day, but it's worth keeping in the back of your mind rather than assuming this week's number means the inflation story is fully behind us.

Where This Leaves Us

We've got two big stories this week, and they connect more than they might seem to at first.

The AI boom is showing up in places beyond the obvious chip and hyperscaler names, and this week's investment banks proved it.

And this week's CPI report, once you look past the headline, gives the market some real breathing room to keep going.

Tomorrow, I want to circle back to SpaceX and that $135 level I've been watching closely all week. I'll also share three names from my watch list that I may be trading soon!

Here's to growing and protecting your wealth!

Comments

Log in or sign up to join the conversation.