A core tenet of my outlook is that a new secular bull market in precious metals began two years ago and, based on historical patterns, will persist for at least a decade. In this scenario, I see gold reaching at least $15,000–$20,000 per ounce and silver $300–$500, with platinum, palladium, and mining stocks rising by a commensurate magnitude. For more detail, see my recent reports on gold and silver.

As you are likely aware, precious metals and mining stocks have recently experienced turbulence related to the Iran war. I have maintained that this is a routine pause of the kind seen in every major bull market and successful investment throughout history (learn more). As is often the case, however, some commentators are using this turbulence to argue that the precious metals bull market is now over and that significant declines lie ahead for years, but I strongly disagree with that view.

One of the reasons why I am so bullish on precious metals and miners is the relentless expansion of the money supply, both in the U.S. and globally, and how that erodes the purchasing power of fiat (or “paper”) currencies, resulting in inflation. Precious metals are the best hedges against that over the long run, especially in the tough times I see ahead in which this fiat money regime that has existed since 1971 unravels.

With that in mind, in today’s report I want to check in on the global money supply, which has been growing at an alarming rate recently and is a major source of fuel for the secular precious metals bull market that began two years ago. With all the issues they cover, the mainstream financial media has consistently ignored this critical issue, which is the cause of so much hardship today, including the soaring cost of living, plunging birth rates, and growing despair, especially among younger generations.

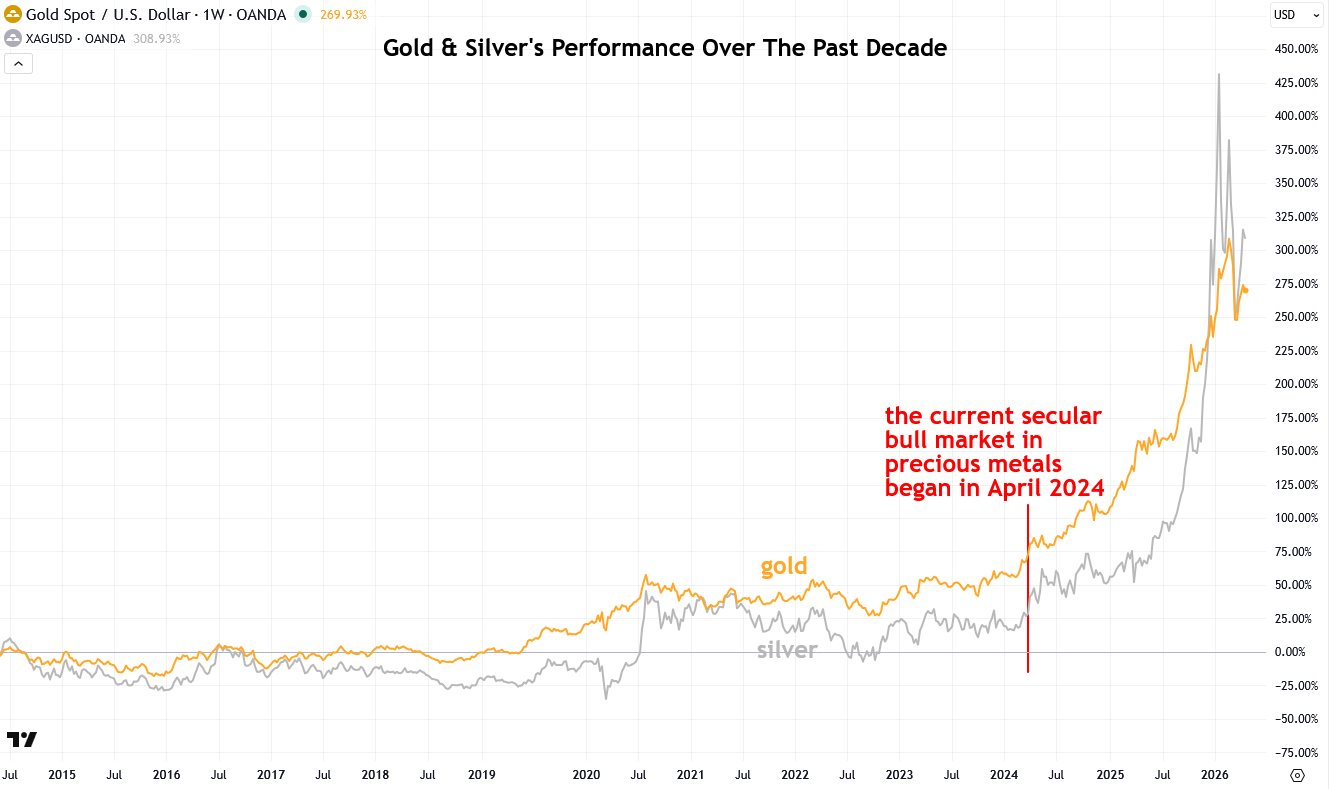

Before we get started, I want to show you a chart of gold and silver over the past decade, including where I marked the start of the secular bull market in precious metals in April 2024. Remember that point in time, because it will come up again when I show you the charts of the U.S. and global money supply next.

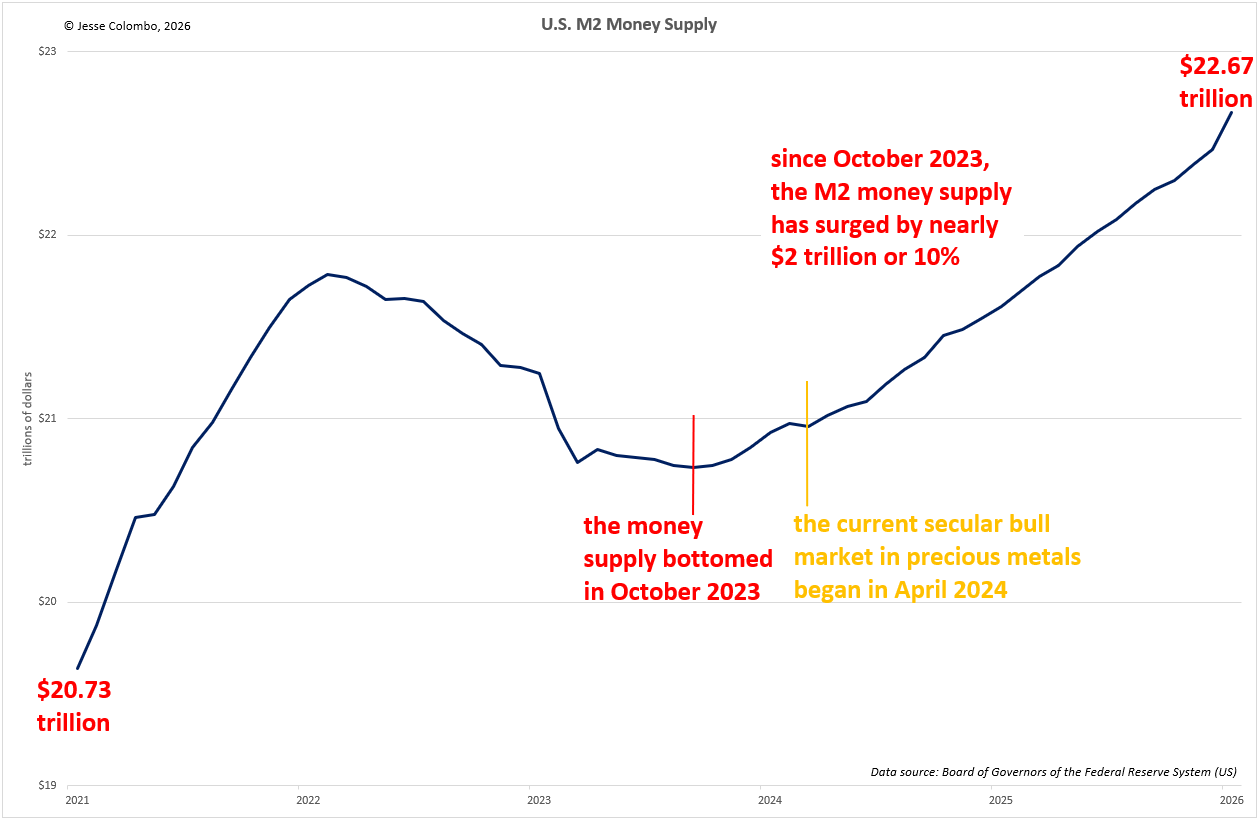

Next, let’s take a look at the chart of the U.S. M2 money supply, which is one of the most widely followed measures of total currency in circulation. After a rare contraction in 2022 and 2023 due to the Fed reining in its balance sheet following the aggressive COVID pandemic-related stimulus programs, the money supply bottomed out in October 2023 and has since surged by nearly $2 trillion, or 10%, which is a large expansion for a non-crisis period.

I want to point out that the U.S. M2 money supply bottomed out just six months before the current secular bull market in precious metals began, and I believe that is no coincidence but one of the primary reasons why precious metals took off when they did. To learn more about the relationship between the money supply and precious metals, read this report I wrote in the fall.

One of the main conundrums of the post-pandemic economy is how inflation has remained stubbornly high, with central bankers, policymakers, economists, the media, investors, and ordinary people pointing to a wide range of causes, while virtually none have pointed to what is the true cause, the ongoing expansion of the money supply.

As Nobel Prize–winning economist Milton Friedman famously stated, “Inflation is always and everywhere a monetary phenomenon.” That means that even soaring oil prices, which we have seen recently due to the Iran war, are not the root cause of inflation over the long run; only monetary debasement is.

The stubborn post-pandemic inflation can clearly be seen in the U.S. core Personal Consumption Expenditures (PCE) chart, the Fed’s preferred inflation gauge, which is running at nearly a 3% annual rate, almost 50% above the Fed’s 2% target. Amid all the hand-wringing over inflation, it is remarkable that practically nothing is being done to address the soaring money supply.

Comments

Log in or sign up to join the conversation.