Unlike the start of the year, it has been frustrating for investors to see the markets pummeling precious metals even as structural supply deficits are growing. While speculation and a risk-on mentality on Wall Street is nothing new, the tech-driven demand and role that precious metals will increasingly play in the future is clear. Yet, recent market behavior tells a different story.

The reasons for the recent rapid selloff are simple. The War in Iran, the fastest pace of inflation in three years and fears over what the new Federal Reserve Chair, Kevin Warsh will do or say at his first FOMC meeting as the leader this week have the market scrambling for cash. Investors are raising it by selling whatever trades easily, including through paper trading in metals from ETFs to miner shares.

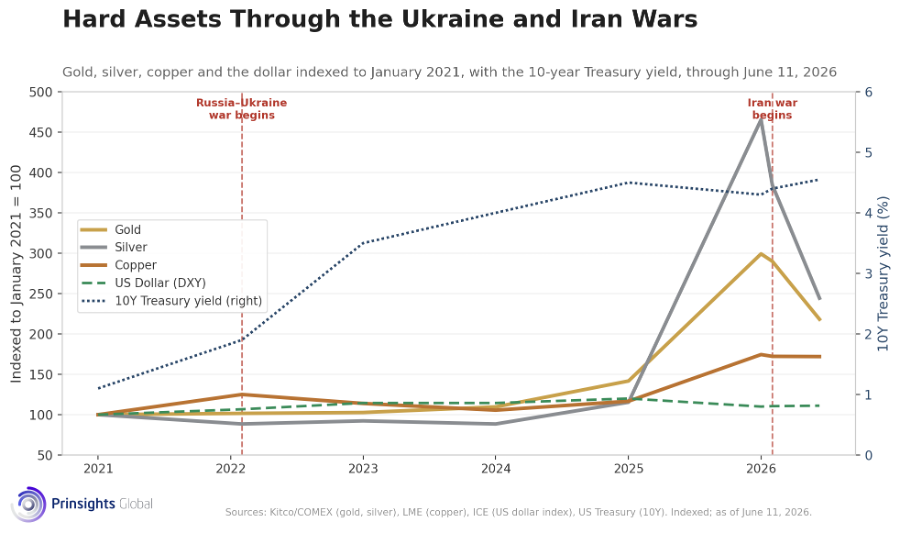

After the start of the year’s record-breaking momentum, silver in particular has been hit hard, dropping as much as 47% from its January record of $121. Gold is down 24% from its $5,595 high. Importantly, copper has held near its own record of $13,842 a ton on the LME, or around $6 per pound.

Yet nothing in the ground beneath any of these metals has materially changed.

That distortion shows us that nerves are high, liquidity is tight and in the current market landscape, asset management funds facing redemptions ended up having to sell their most liquid metal positions in order to raise cash.

The other wrinkle in the wildness of Wall Street is that trading algorithms have been piling on as prices break through chart levels and negative headlines induce even more headlines. The result is a market that’s pricing near-term angst while long-term physical deficits remain under structural limitations.

The sobering fact is that new copper or silver mines will still take anywhere from 7 to 12 years to permit and build. On the pragmatic side, solar technology still consumes about 17% of the annual silver supply, and silver is still in its 6th straight annual deficit, 95 million ounces short in 2025 and 820 million ounces short since 2021.

This hard asset selloff has unwound leverage in the paper market, not shifted metal in the ground.

The Commodity Liquidity Trap

Silver is the sharpest example, and historically has been, of how paper trades can invoke acute price impacts. That’s because it represents dual values that can be battered by dual narratives as a result.

Let’s break the silver situation down. On one hand, it is a form of monetary wealth, which can be bought, sold and stored like gold. On the other, it is an industrial metal with more than half of its demand coming from solar tech, electronics and electrical contacts. Silver has been in a deficit every year since 2021, yet prices dropped nearly in half this Spring. That change reflects speculative selling that is also a scramble for cash, not a change in how the metal is used or mined.

To be sure, silver isn’t alone. Platinum prices have also dropped to as low as $1,660, the lowest level since December, and palladium has hit near an eight-month low as well. Yet platinum just posted a record 1.082 million ounce deficit and is heading into a 4th straight shortfall.

Still, silver prices fell dramatically because it is the most leveraged and volatile metal of the group. As the dollar hit 100 and 10-year yields rose, investors sold what was easiest to liquidate quickly, not what was physically abundant.

When we zoom out even further, gold, silver, and copper began climbing around the time that the Russia-Ukraine war escalated in February 2022. Yet silver is still trading at more than double its 2021 level, even after halving over recent months.

As for mining stocks, they have fallen by more than the specific metals themselves because the market amplifies their operating and financing risk. On top of that, forced or programmed sales in mining ETFs triggered selling across the board, regardless of whether individual companies’ assets or long-term supply conditions have changed.

Meanwhile, the strongest producers are still making money at these levels. In the first quarter, Pan American Silver (PAAS) reported a silver-segment all-in cost of $6.63 an ounce, helped by gold by-product credits, and First Majestic (AG) reported $29.76 per silver-equivalent ounce. Even at $70 silver, both still hold wide margins, and demand is only set to climb, with clean technologies alone forecast to consume over 1.5 billion ounces of silver through 2030.

Copper’s Fixed Demand Floor

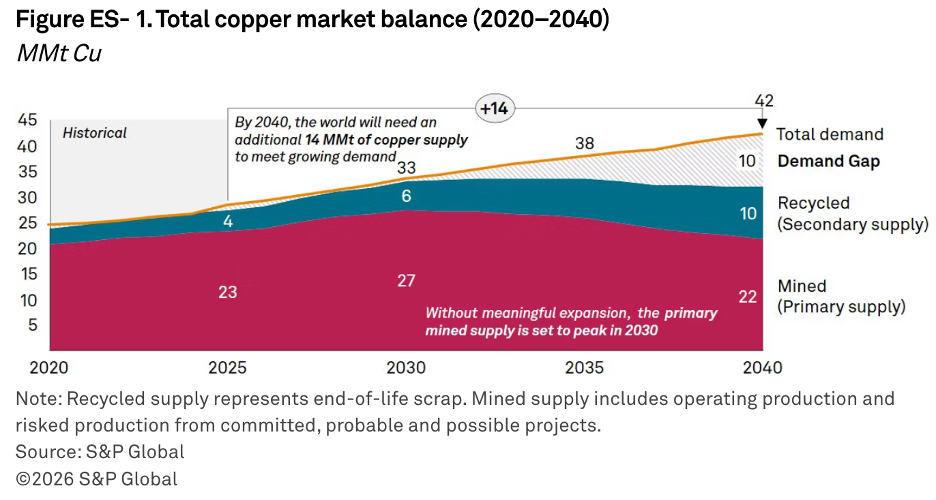

Copper prices have held steady these past few months because large businesses that are copper buyers cannot walk away from electricity infrastructure needs. The world’s power grids will require roughly 2.5 times more copper by 2040.

Power utilities, grid operators and big tech data center developers must all lock in copper supply years in advance of construction. They also work on fixed budgets, so this buying did not disappear when the price of silver whipsawed, nor is there as substantive a paper market in copper.

The copper market is on track to run short by more than 500,000 tons this year, as Chilean ore grades, some of the most important in the world, are down 25-30% since the early 2000s, and new deposits can take an average of 17 years from discovery to first metal. Copper still trades near a record while paper silver prices have halved since the start of this year.

As we head into Kevin Warsh’s first FOMC meeting as chair this week, how he frames his message will be key. He will have to balance inflation concerns, the high cost of capital for growth and debt servicing, and the question of whether the Fed sees enough stress building beneath the surface to pause until there’s more clarity on an Iran-U.S. resolution.

Digging In

As difficult as it is, this moment calls for commodity investors to dig in and be patient. Every one of these metals is being mispriced by the same tunnel vision from the short-sightedness over on Wall Street. The shortages behind them have not eased, and that’s exactly what makes this a window for disciplined accumulation rather than capitulation. Silver and the miners that drive it forward carry the steepest discounts and the sharpest swings, while copper carries the least – and is a strategic place to start.

Comments

Log in or sign up to join the conversation.