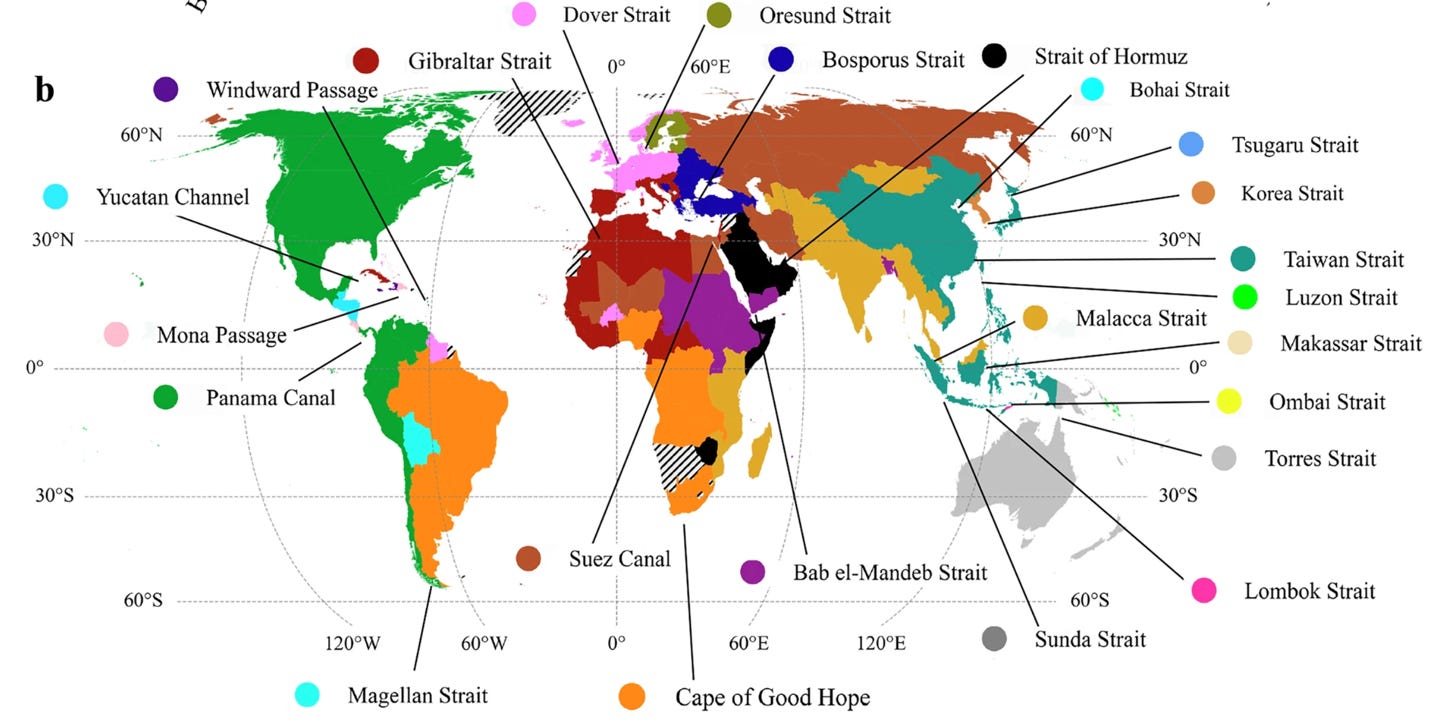

For decades, the Strait of Hormuz has been the world’s most sensitive energy choke point. Today, the hypothetical “nightmare scenario” is now a very real and very costly reality. With a dual blockade effectively closing the artery that carries 20% of the world’s liquid petroleum, the global economic trade map is being violently redrawn.

As we’ve often discussed at Prinsights, money flows don’t just stop or run away in the face of a crisis, instead it migrates.

While it is true that the blockade creates inflationary headwinds and economic pain for the average consumer, for strategic investors, it can reveal a new hierarchy of power.

What we are witnessing right now is a massive structural pivot away from the Middle East and Persian Gulf dependency for oil. While the headlines are focus on the chaos and unfortunate war, three specific sectors are quietly unlocking the immediate benefits of this era that’s gravitating toward a “Realignment of Energy.”

Below are the three sectors set to strategically benefit from the lockdown in the Strait of Hormuz.

1. The New Sovereigns of Supply: Shipping and Logistics

With the strait is effectively shuttered, the simple act of moving a barrel of oil or a ton of cargo has become exponentially more valuable.

Shipping routes are being rerouted around the Cape of Good Hope (Africa’s Southern point), while now adding thousands of miles and tacking on weeks of travel time to global trade. This “extra-mile” demand could be the start of a windfall for shipping and logistics companies, particularly those outside the immediate conflict zone.

We are seeing a surge in dominance from logistics hubs in Southeast Asia, North America, and the Caribbean. As Middle Eastern supply lines are frozen and conflict-driven, these regions are stepping in to bridge the gap.

Researchers from a 2025 Oxford University analysis report pointed out that globally, critical chokepoints impact around $192 billion worth of maritime trade each year. These disruptions result in estimated economic losses of about $14 billion annually. Yet, when primary routes fail, secondary hubs with decreased “spot exposure” become the new market makers.

As one of the report’s authors noted, “by identifying where and how the system is most vulnerable, we can help governments and businesses strengthen resilience to future shocks.” Business carriers focused on US-Europe or Australia-Asia routes are now finding themselves as the stable beneficiaries of this new, longer-distance trade reality.

2. The Non-OPEC Renaissance: Major Oil Outside the Middle East

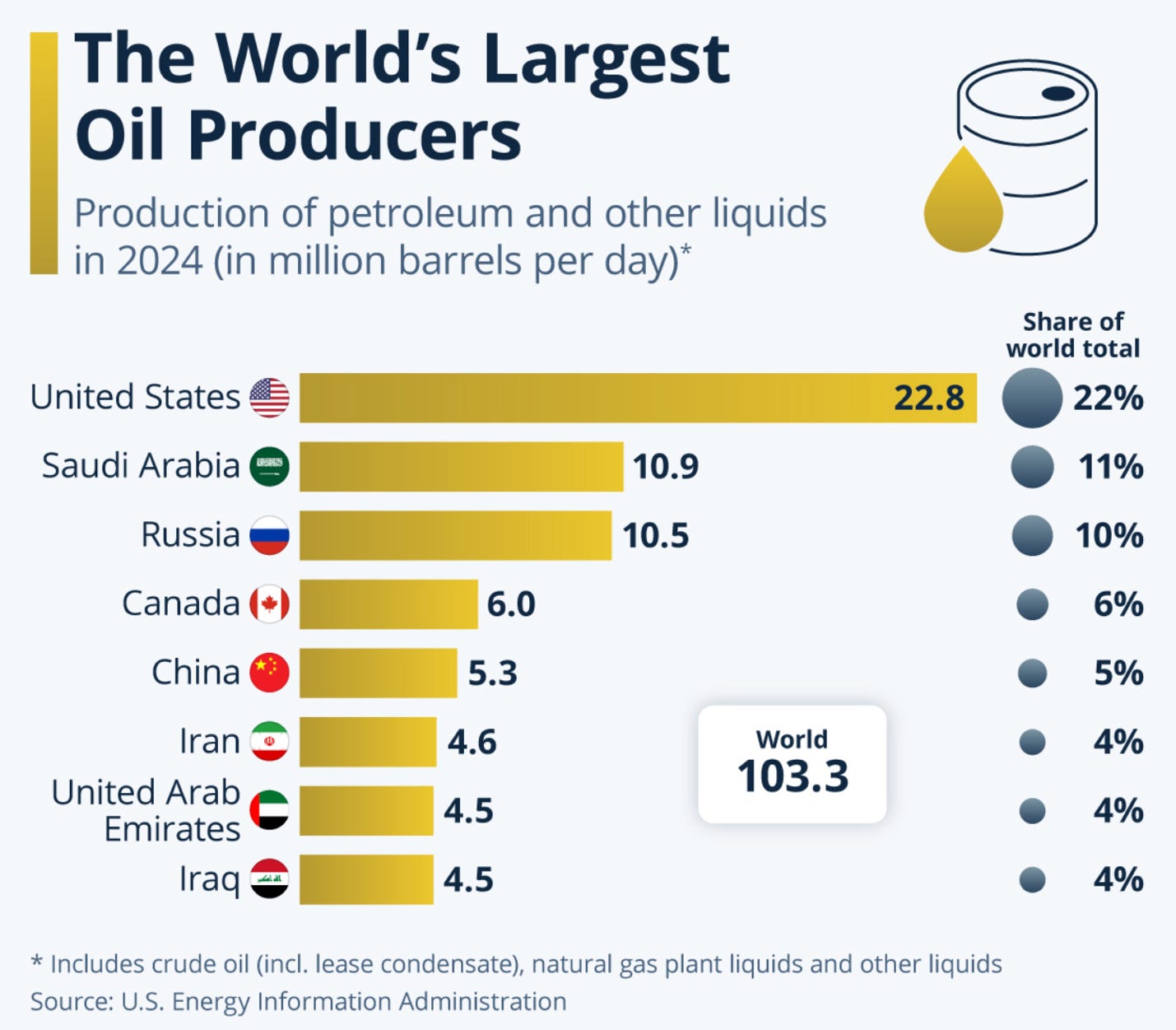

The disruption we are seeing is truly unprecedented. According to the International Energy Agency (IEA), Brent futures finished April more than 55% above pre-conflict levels, marking “the largest oil supply disruption in history.” This price floor is a massive tailwind for “big oil” producers operating in the Permian Basin, the North Sea, and Brazil’s pre-salt fields.

As highlighted by the BBC, the global scramble for non-Middle Eastern crude has turned once-expensive extraction projects into gold mines. Analysis from Wood Mackenzie also notes that energy trade flows are being permanently rerouted, a shift that favors long-term infrastructure investment in the Americas and Africa.

While companies like ExxonMobil, Chevron, and Equinor are in the business of selling oil, they’re increasingly selling security – and the market is now being forced to pay a premium for it.

3. The Architect of Volatility: Wall Street

Finally, we turn to the casino and look to the “House.” While the real economy grapples with higher costs, Wall Street is thriving on the volatility. What some of the top traders on the street know is that the moment offers the opportunity for a “reconfiguration” trade. What that means is that investors are moving billions to manage risk and hunt for new opportunities in energy transition and alternative logistics.

As I’ve noted several times before in my books, the big banks thrive when the “Permanent Distortion” of the markets creates wide spreads and high trading volumes. When we look at the numbers, they speak for themselves. Morgan Stanley recently reported profits of $5.57 billion (up 29% YoY), Goldman Sachs smashed $5.63 billion (up 19% YoY) and JPMorgan Chase surged with $16.49 billion in first-quarter earnings (up 13% YoY).

Wall Street has positioned itself as the primary intermediary for the massive capital shifts required by this conflict. From hedging energy prices to financing the “New Energy” infrastructure, the big banks are the ultimate winners of the Hormuz stalemate.

The reality is that in 2026, the world and the nature of the geopolitical landscape is changing. While headlines are focused on conflict in Iran and the impasse with the Strait of Hormuz, those developments are just the beginning of a broader trend over the longer term.

Comments

Log in or sign up to join the conversation.