The chatter from Wall Street and the financial news media has created a lot of noise around short-term price fluctuations, daily technical indicators, and geopolitical headlines. Right now, most eyes are glued to the recent U.S.-Iran agreement, whether it sticks, and any developments around the reopening of the Strait of Hormuz.

When looking at gold, analysts have been asking whether short-term geopolitical anxiety will cool or whether the wind has been permanently taken out of gold’s sails.

But as we continue to detail, the structural shifts beneath the global financial system and the fundamental decoupling of real, physical assets from the printing-press realities of Western central banks are unfolding in real time.

This week, the World Gold Council (WGC) released comprehensive information that proves the world’s most powerful monetary institutions are executing the exact long-term strategy we have been sharing.

“More Positive on Gold Than Ever”

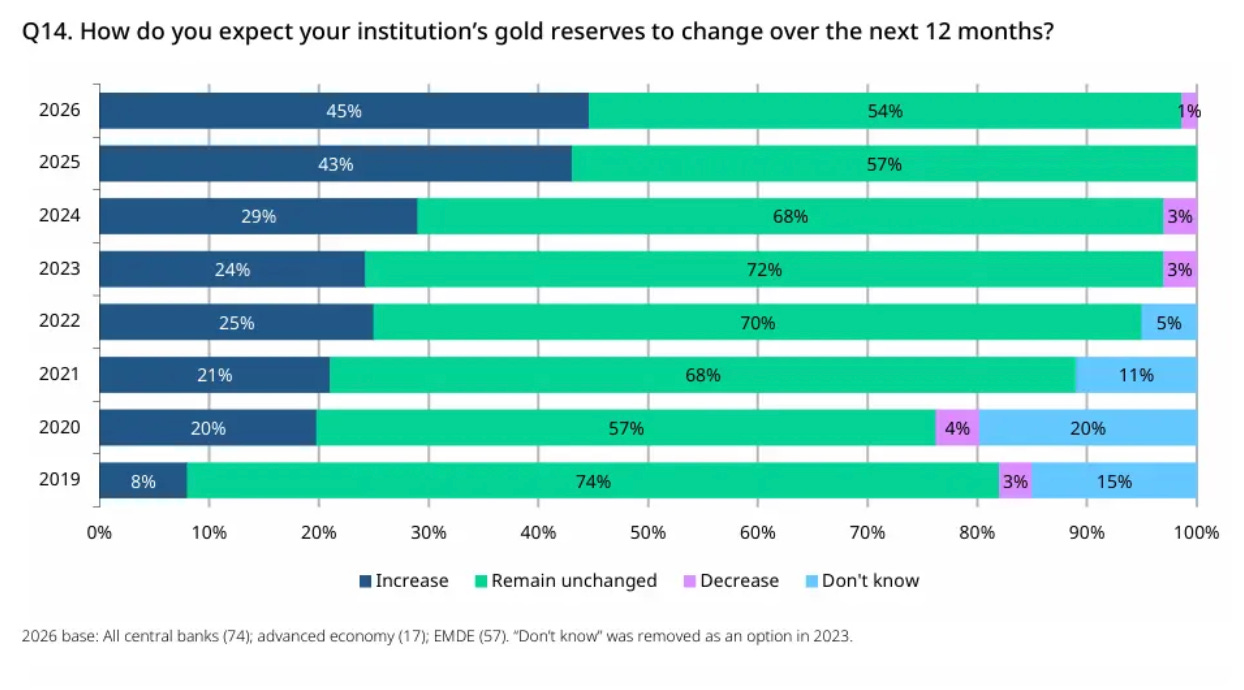

The World Gold Council just published its 2026 Central Bank Gold Reserves Survey. The headline figure is a historic wake-up call, revealing a record 45% of central bank respondents openly state they expect their own institutional gold reserves to increase over the next 12 months.

When we put that into perspective, this is the highest proportion recorded since the survey’s inception. Meanwhile, a whopping 89% of reserve managers expect total global central bank gold holdings to rise over the coming year. Conversely, a mere 1% intend to reduce their positions.

This development offers an active, coordinated flight to safety by the very leaders who are calling the shots for the global financial system.

“What stands out is the shift in how central banks think about gold. Fewer see it as a legacy holding; more see it as an active, strategic allocation in an environment defined by geopolitical uncertainty and reserve diversification,” said Shaokai Fan, Global Head of Central Banks at the World Gold Council.

The important takeaway here is that ongoing volatility in the macroeconomic landscape hasn’t changed their outlook. Instead, it has amplified gold’s role as the ultimate crisis buffer, a long-term store of value and a geopolitical risk hedge.

De-Dollarization Is No Longer Just a Theory

For years, mainstream media dismissed the concept of structural de-dollarization as a fringe theory. The WGC survey just brought that reality to light.

According to the 2026 data, 74% of responding central banks anticipate that the U.S. dollar’s share of global reserves will decline moderately or significantly over the next five years. At the same time, 84% expect gold’s share of global reserves to grow.

Over the last four years, global central banks have built up an average of 1,000 tonnes of gold annually. That’s a massive doubling of the 500-tonne annual pace compared to the preceding decade. As Prinsights detailed at the start of June, the accumulation recently hit a symbolic milestone when gold officially surpassed U.S. Treasuries to become the world’s largest collective reserve asset.

Ultimately, governments are no longer willing to back their economic futures entirely on the debt obligations of a single, highly leveraged global superpower. Increasingly, they are using the moment to reset and choosing the ultimate hard asset instead.

Unwinding the Headwinds

To truly understand how this structural dynamic interacts with current events, we must look closely at what is happening to the paper markets today. With diplomatic agreements passing between Washington and the Middle East, specific market pressures are shifting.

In a recent assessment, one of Wall Street’s top analysts, Alex Wolf, global head of macro and fixed income strategy at JPMorgan Private Bank, underscored this critical moment for gold, noting, “I see the U.S.-Iran agreement as a positive catalyst for gold because many of the headwinds created by the conflict are now starting to unwind.”

Now, a casual market watcher might look at those unwinding headwinds like a firmer dollar or cooling oil prices, and assume that as the crisis premium fades, gold could lose its appeal. But that conclusion is a fundamental misunderstanding of the distortion that’s been embedded in the markets.

When short-term macro headwinds unwind, they don’t break the gold market; instead, they clear a path for structural, long-term accumulation. The temporary price pullbacks created by these shifts do not deter policymakers at central banks. In fact, they create buying windows for governments to fortify their physical positions – and at a discount price.

The Gold Base is Broadening

What makes this current moment different from historical trends is that this movement is no longer confined solely to developing nations or emerging markets trying to escape Western dominance.

While emerging-market institutions continue to lead the charge, the desire to hold physical gold is broadening. The WGC survey showed that 18% of advanced-economy central banks now plan to increase their gold holdings over the coming year as well. Countries from Indonesia to Malaysia and Guatemala to El Salvador are now actively planning to step into the gold arena.

When digging into the details, an increasingly new wrinkle is how they plan to secure and store this wealth. Central banks are choosing to bring their gold closer to home. The survey showed an ongoing push toward diversifying vault locations, where 9% of respondents expanded their domestic storage footprints over the past 12 months, and 10% actively diversified their overseas vault allocations.

This means that central banks are moving their physical assets from centralized, vulnerable financial hubs to places where they greater control.

What This Means For You

The big takeaway here is not to let short-term market corrections or the noise of geopolitical headlines dictate your long-term investment perspective.

When nearly half of the world’s central banks tell us they are actively buying the exact asset they cannot print, that’s a material development. Central banks are signaling that they intend to preserve wealth as the current volatility in U.S. dollar currency faces its ultimate long-term blowback.

We continue to view any short-term market pullbacks as a golden opportunity to strategically unlock value in gold and select gold miners.

Comments

Log in or sign up to join the conversation.