The January Federal Open Market Committee (FOMC) minutes dropped this week. Suddenly, the headlines turned to the Federal Reserve potentially hiking rates and what that could mean. But if you actually read them and examine the data, that framing doesn’t make sense.

Let’s quickly walk through the six reasons why the Fed’s rate hike headlines are not matching the reality the data is showing:

1. The Vote To Hold Rates Was 10 to 2. Dissenters Wanted to Cut.

The January FOMC vote was 10 to 2 to hold rates at 3.5% to 3.75%. The two dissenters, Governors Miran and Waller, didn’t want to hike. They wanted to cut rates by 25 basis points. That indicates that not a single voting member wanted to raise rates. The most hawkish position on the entire committee was to stay put. None of that screams for a rate hike headline.

2. “Several Officials” Were Talking About a Hypothetical, Not a Plan

What actually happened is that some officials wanted the post-meeting statement to include “a two-sided description” of future rate decisions. So, what does that mean? Basically, they wanted to acknowledge that rate hikes could be appropriate if inflation stays persistently above target. What you should know is that’s a big “if.” There’s a huge difference between “let’s acknowledge hikes are theoretically on the table” and “we think we should hike”.

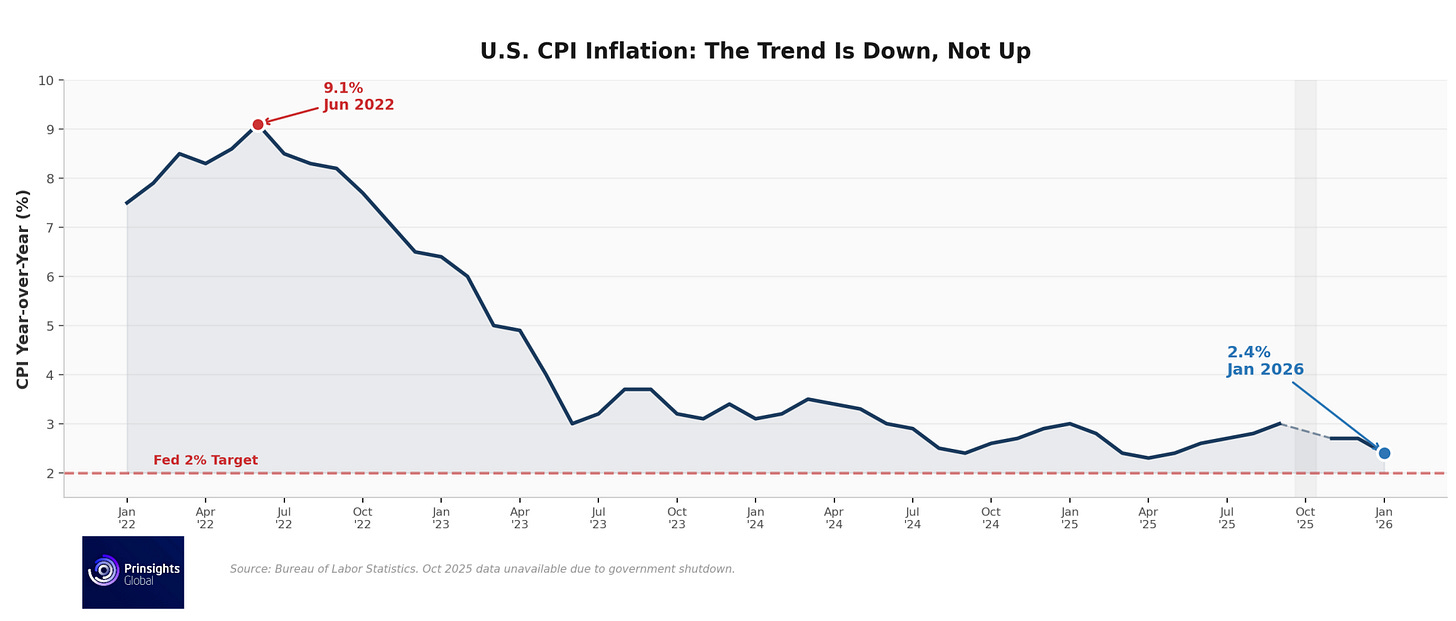

3. Inflation Is Moving in the Right Direction, Albeit Not Quickly

The U.S. Bureau of Labor Statistics (BLS) reported that the Consumer Price Index (CPI) came in at 2.4% in January, down from 2.7% in December. Meanwhile, the Dallas Fed’s trimmed mean personal consumption expenditures or PCE rate, which strips out the noisy one-off price swings to give you a cleaner read, is at 2.5%, down from 2.9% a year ago. The trend is pointing toward 2%, not away from it. You don’t hike into that.

To note: Some economists argue the January CPI may carry a slight downward bias because last fall’s government shutdown disrupted BLS data collection in October, and Moody’s estimates the rate would be closer to 2.7% if that missing data were included. But, even so, the broader disinflationary trend holds.

4. The Labor Market Is Softening, Not Running Hot

2025 job growth got revised down hard, from 584,000 to just 181,000 for the whole year. January 2026 came in at 130,000 jobs, with unemployment sitting at 4.3%. Nobody is looking at those numbers and thinking the economy is overheating. If anything, the risk is that rates are already too tight and doing more damage to the labor market than necessary.

5. Even the Hawks See Inflation Coming Down

Dallas Fed President Lorie Logan is one of the more hawkish voices on the committee. She supported holding rates, not a hike. And she’s said that her expectations are for inflation to keep improving this year. That’s why, when the hawks at the Fed are calling for patience and expecting disinflation, the hike narrative doesn’t compute.

6. The Doves Are Way More Aggressive Than the Headlines Let On

Governor Miran, a voting member of the FOMC, said he doesn’t see a significant inflation threat. He believes low shelter inflation will offset pressures elsewhere and that the biggest risk right now is the Fed not realizing how tight policy already is. He’s penciled in 150 basis points of cuts this year. Philadelphia Fed President Paulson sees a path for lower rates toward the end of 2026. That’s the other side of the committee that the headlines largely ignored.

What This Means for Gold

The FOMC vote was unanimous: either hold or cut. Meanwhile, inflation is trending down, the labor market is cooling and the hawks expect disinflation. A few officials floating hikes as a theoretical risk scenario is not the same as the Fed pivoting toward tightening rates.

The headlines took the most dramatic read possible from a set of minutes that, on closer examination, still tilt toward easing.

This is exactly the kind of environment that is favorable for gold.

The Fed is divided and uncertain about its next move. Yet it is not signaling rate hikes in a clear way, so real rates are likely to come down as cuts resume. The labor market is also losing momentum and headline volatility is shaking confidence in traditional risk assets.

Gold thrives when monetary policy is in flux and on any unclear signals, such as the most recent ones or those we covered in our recent analysis about Kevin Warsh’s dovish tendencies.

Whether the Fed cuts once this year or four times, its direction points toward easier policy, a weaker dollar and lower real yields. That’s a solid setup for gold’s next leg up, and nothing in these minutes changes that. If anything, the confusion around the headlines only reinforces why having that hard asset allocation at these levels makes sense right now.

Comments

Log in or sign up to join the conversation.