We at Pretiorates are always delighted to share our thoughts on the markets with you—thoughts that we hope will serve as a useful compass for your investment decisions. But of course, we too rely on input from which we distill our assessments. Among the sources we find particularly valuable is cycle analyst Eric Hadik of InsiideTrackTrading. He has described the behavior of the U.S. dollar, gold, and Bitcoin (BTC.X) in a simple and intuitive way: They function like the game of rock, paper, and scissors. Each can beat the other—and one is always on top.

We have attempted to translate this theory into a trend model using our own strength indicators. It quickly became apparent: one of these assets always takes on the role of favorite—but can rarely defend this position over the long term. As soon as one of the three candidates reaches full strength of 100%, the leading role is usually passed on again. And the dynamic seems to work the same way on the other end of the spectrum: absolute weakness at 0% is only evident for a short time. What’s important for trend analysis, however, is that whoever is at the very bottom usually doesn’t stay there long.

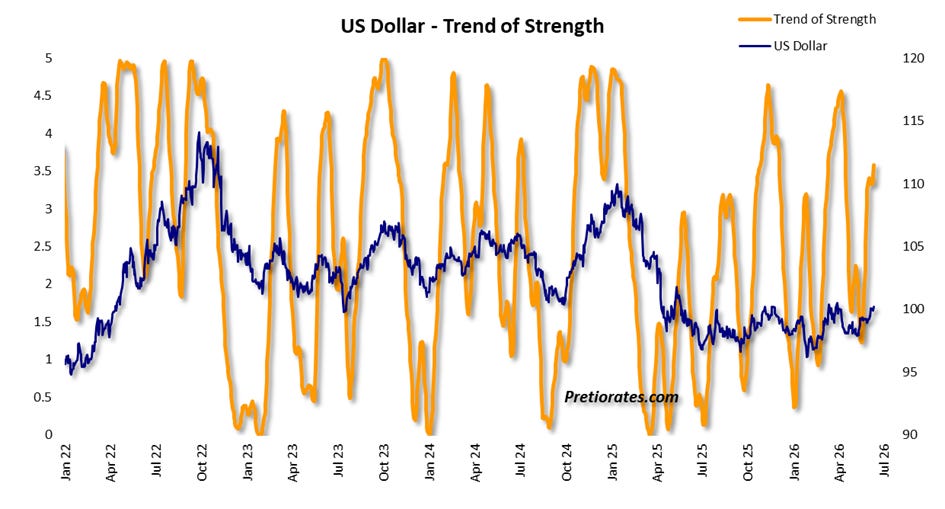

Given current events, it’s hardly surprising that the U.S. dollar is currently gaining strength and is likely to remain in the lead for the foreseeable future.

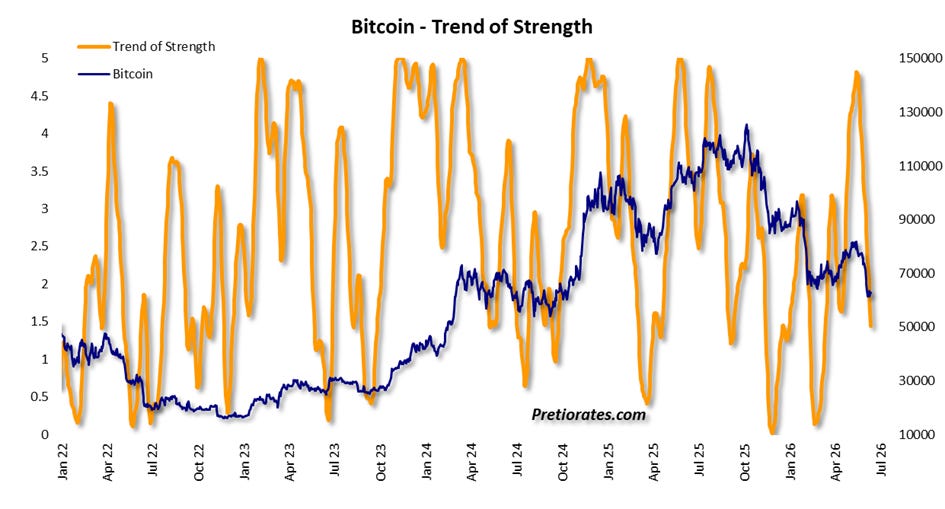

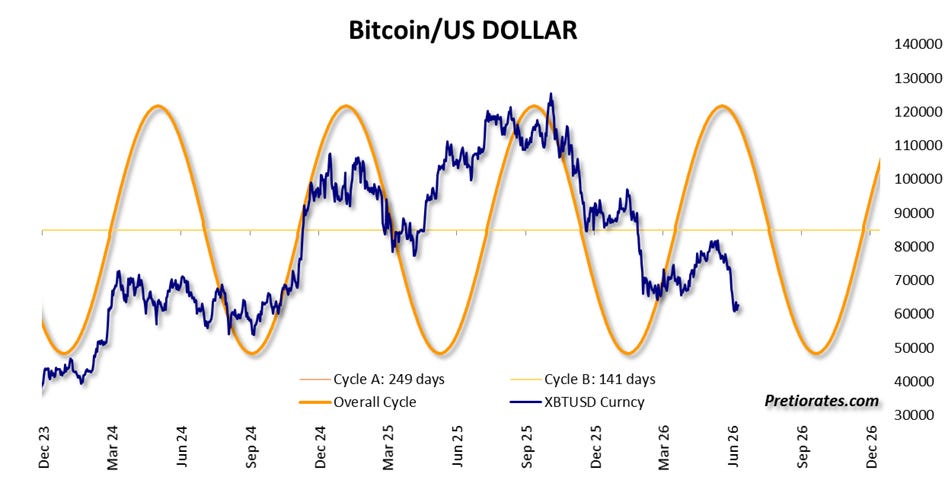

Bitcoin, on the other hand, had temporarily taken the lead back in April, but May turned out to be anything but a merry month. The strength index suggests that little will change in this regard for the time being.

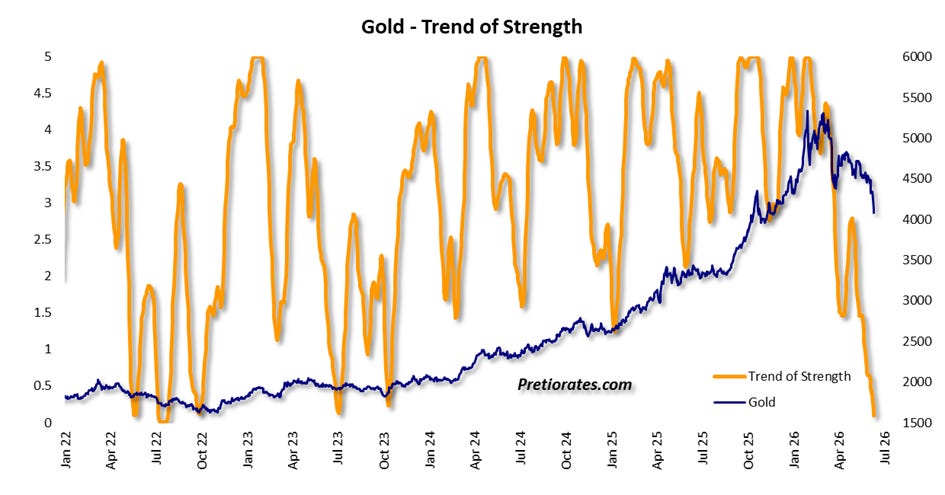

It is equally unsurprising that the third member of the trio, gold, had to endure a dismal spring. But—and here comes the big “but”—the strength index has nearly reached its absolute low. If this dynamic continues, there is a high probability that the precious metal will next take the lead. Gold could thus rise again from substitute to captain.

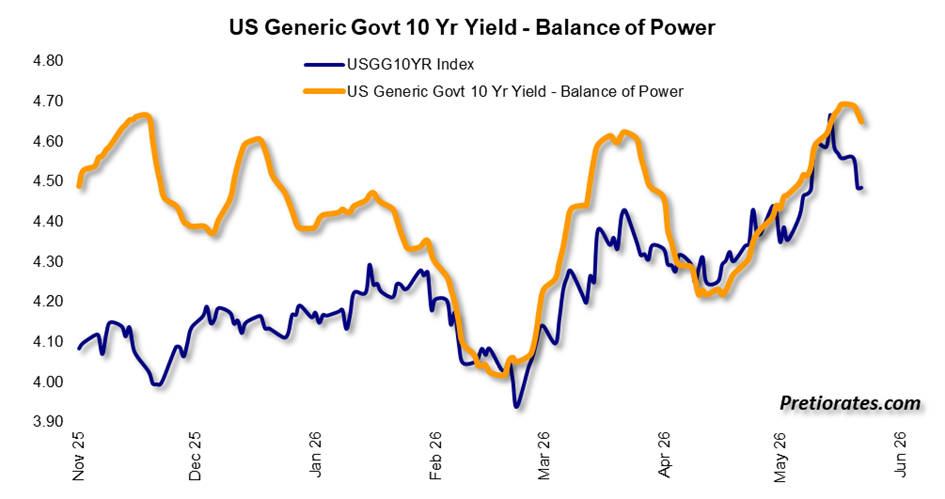

This assessment may be based on the principle of “hope for the gold bugs.” But let’s try to confirm it based on current events: If the U.S. dollar were to actually cede its leading role to gold and enter a consolidation phase in the coming weeks, gold would very likely benefit from this. The trigger could be of a geopolitical nature. Perhaps the parties involved in the Iran conflict will come to their senses after all. This would also ease inflationary pressure, and US Treasury yields could fall. Of course, this, too, is to some extent based on the principle of “hope.” Yet the reliable “Balance of Power” indicator from the US bond market has just generated a sell signal for US Treasury yields…

The Bitcoin cycle has also been working very well recently and suggests that the cryptocurrency—barring technical rebounds—can likely not expect a sustained upward trend until the fall.

Gold bugs can therefore hope that the cycles will continue to function in the coming months as they have in recent years.

Another question is currently pressing: Following the minor tremors of the past few days, should equity investors also expect a correction?

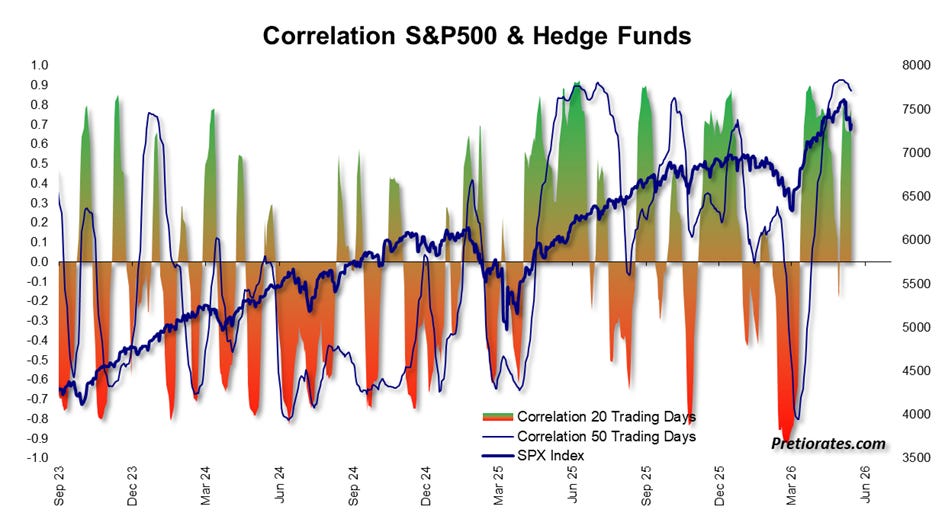

If we analyze the current asset strategy of hedge funds, they continue to show their bullish side. Long investments clearly outweigh short positions. Hedge funds are thus betting on further rising stock prices.

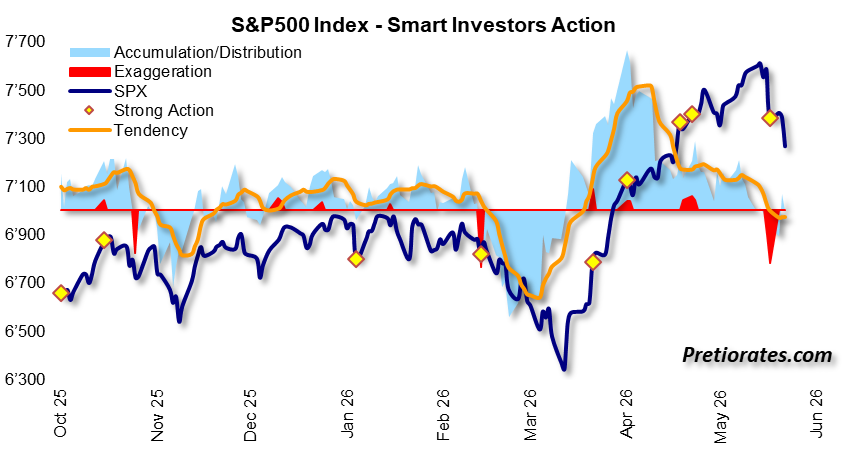

The smart investors—that is, those who tend to position themselves discreetly in the background with large investments—are not accumulating further. However, the indicator’s red area suggests that the market has recently overreacted on the selling side. This would make a rising index quite likely.

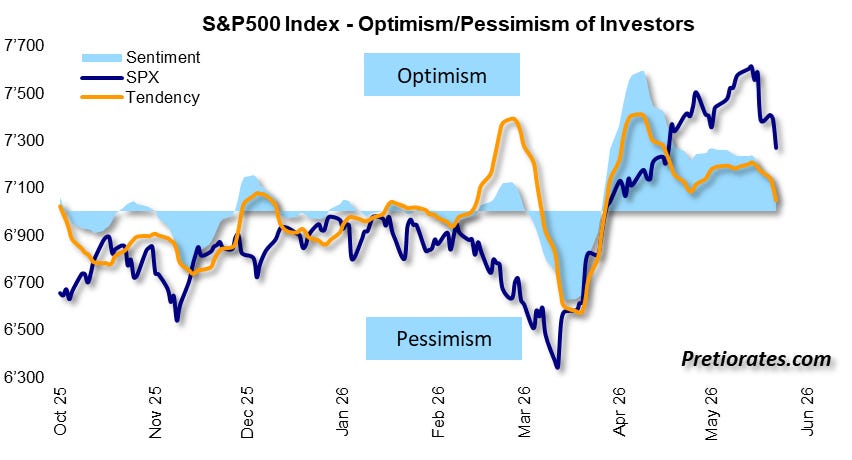

Of course, optimism has waned along with the recent decline in stock indices. Yet it remains on the positive side. Accordingly, Wall Street is expected to remain resilient.

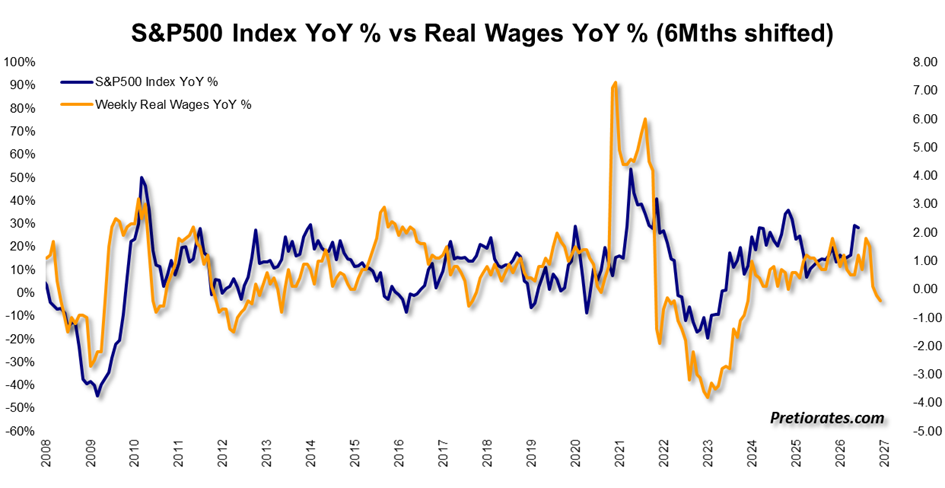

But let’s not kid ourselves: The war with Iran has led to an energy shock. While this is currently still relatively mild, the disruption to oil exports through the Strait of Hormuz could only be mitigated because many nations—particularly China and the U.S.—are drawing on their oil reserves, with China importing significantly less and the U.S. simultaneously exporting significantly more. But these reserves are not bottomless. In the second half of the year, we will be heading from a supply deficit toward a shortage unless the Strait of Hormuz reopens soon. Then consumers’ already strained wallets are likely to come under even greater pressure. And we know from previous observations: Consumers’ real income correlates strongly with the stock market. If people cannot save, they can also invest significantly less. Investors would therefore be well advised to take profits as markets rise again.

Comments

Log in or sign up to join the conversation.