.jpg")

By the time the public is finally invited to the IPO feast, much of the banquet has already been consumed.

The stock market occasionally experiences moments when investors stop asking what a company earns and instead ask what civilization itself may become if the company succeeds. America has entered such a season again. The railroad era had Vanderbilt. The automobile age had Ford. The internet age had Bezos and Page, Jobs and Tm Cook, Gates and Zuckerberg. The artificial intelligence era has produced a collection of private corporations so immense, so strategically intertwined with communications, defense, software, satellites, cloud computing, robotics, and national power that they increasingly resemble sovereign entities more than mere businesses. The new AI icons that are still private are Amodei, Altman and Musk. And now they are coming public. The summer and autumn of 2026 may become remembered as the greatest transfer of private technological wealth into public markets in modern financial history — a speculative migration measured not in millions or billions, but in trillions. At the center of the Wall Street launchpad stands SpaceX.

The remarkable feature of the anticipated SpaceX Nasdaq listing is not merely its size. It is the combination of immense valuation and microscopic public supply.

Private transactions already imply a valuation approaching:

$1.7 trillion to $2.0 trillion

Yet the proposed public float may initially consist of only:

3% to 4% of total shares outstanding

This creates an extraordinary imbalance between supply and demand.

Passive index funds, growth managers, sovereign wealth funds, pension systems, momentum traders, retail investors, and AI-focused ETFs may all compete for a sliver of tradable equity smaller than many ordinary industrial IPOs.

The result could resemble less an IPO than a liquidity stampede.

Some institutional estimates now quietly discuss the possibility that:

a $2 trillion IPO valuation

could briefly inflate toward:$2.3 trillion to $2.7 trillion

during the initial scarcity phase.

IPO Float Comparison (% of Shares Available to Public)

Typical Mega IPO ████████████████ 15%

Recent Tech Unicorn ███████████ 10%

SpaceX Estimated Float ███ 3–4%

Yet, the trio of companies inside Spacex is losing money. While Starlink brings home the bacon for now, the combined entity lost an estimated $5 billion in 2025 and is unlikely to be profitable until at least 2028. The mathematics become staggering, dare we say, irrationally exuberant. Bulls project a tripling of 2026 SpaceX’s total revenue projected for 2026 when it becomes public to roughly $100 billion in about 4 years and they are banking that this will be another Amazon (AMZN) in prior decades using its AWS to fund retail or when Google (GOOGL) used its search engine profits to fund money losing moonshots like Waymo – autonomous vehicles, creating new entities with monopolistic stature.

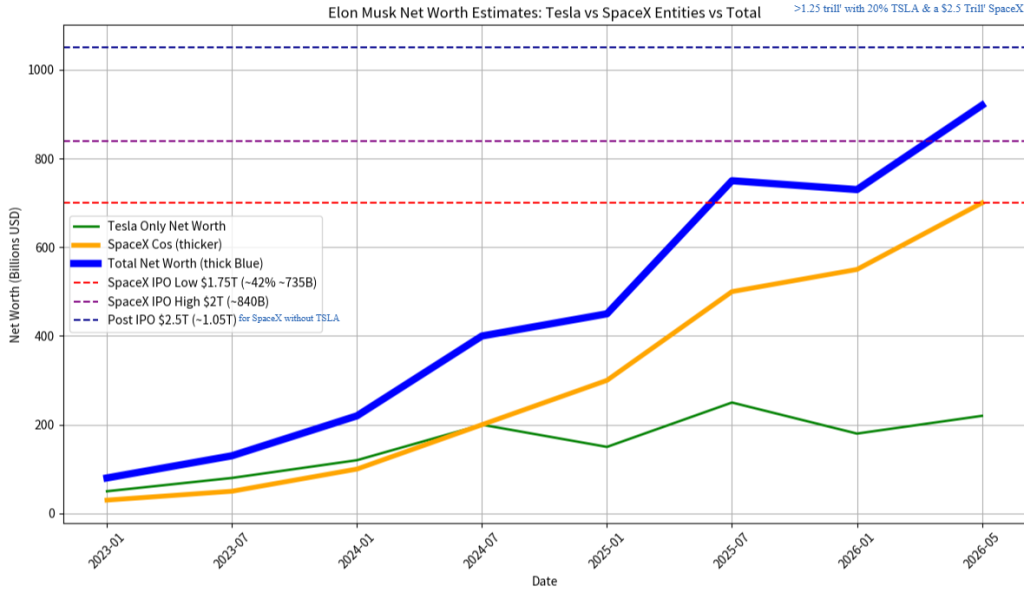

Elon Musk and the Arithmetic of Modern Power

Assume Elon Musk ultimately controls approximately:

40%–42% economic ownership of SpaceX common equity.

Under various valuation scenarios:

SpaceX Valuation | Approx. Musk Stake Value |

|---|---|

$1.75 trillion | ~$700B–$735B |

$2.0 trillion | ~$800B–$840B |

$2.5 trillion | ~$1.0T–$1.05T |

In other words, the public market could temporarily create:

the world’s first trillionaire on paper, not including his $150 to $300 billion of assets and option packages from Tesla (TSLA).

At such valuations, one privately founded company would approach:

the GDP of Italy (and Musk’s personal net worth may surpass Switzerland’s GDP)

exceed the market capitalization of most global stock exchanges,

and rival the combined value of entire industrial sectors.

Previous generations built steel mills. This generation builds orbital internet constellations and reusable rockets while simultaneously competing in AI, robotics, autonomous transportation, communications infrastructure, and defense contracting.

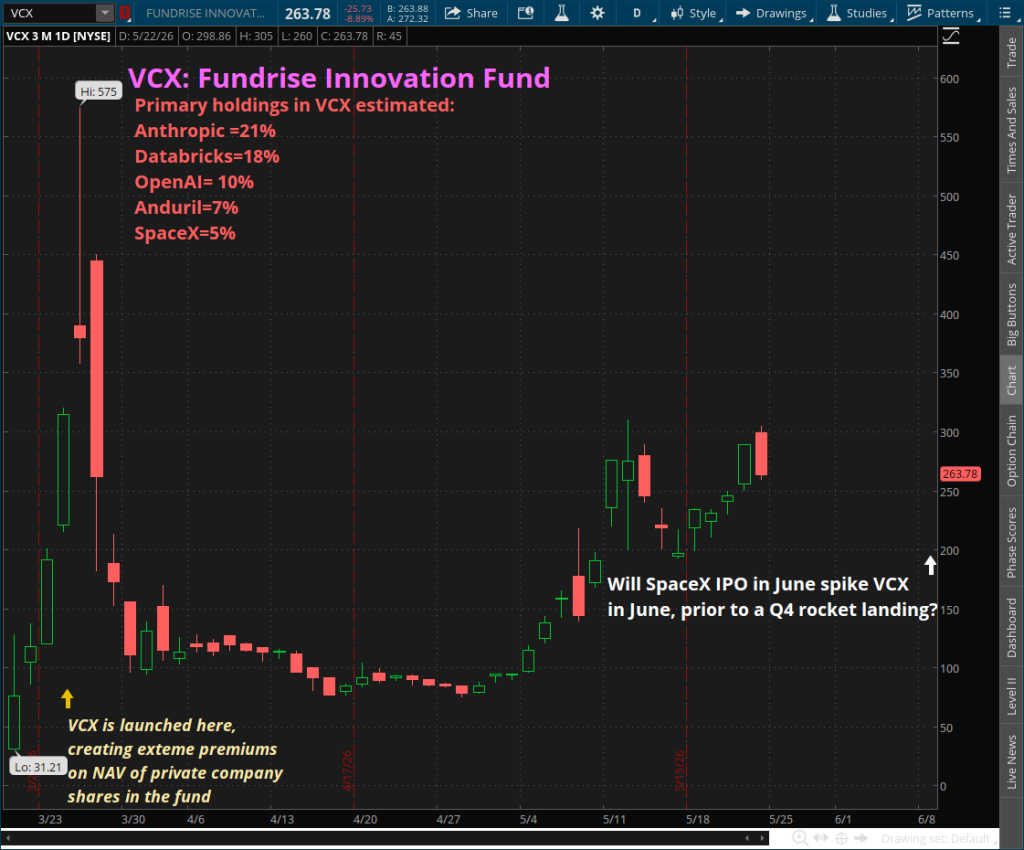

VCX and the Public’s Backdoor Into Private AI

One of the more fascinating speculative instruments in this cycle is the Fundrise Horizon Fund (VCX), which effectively functions as a retail-access bridge into late-stage private technology holdings before they IPO, such as Spacex.

At a hypothetical:

VCX share price of $300

or a return toward:prior highs above $500

investors are implicitly assigning extraordinary premiums to its underlying private holdings.

If SpaceX comprises roughly:

20%–25% of NAV exposure potential during a speculative mania

then the market may effectively be valuing SpaceX within VCX at levels approximating:

VCX Price | Approx SpaceX Exposure Portion | Possible Implied SpaceX Enthusiasm Valuation |

|---|---|---|

$100 | $20–$25 | ~$1.2T–$1.6T |

$200 | $40–$50 | ~$1.8T–$2.2T |

$300 | $60–$75 | ~$2.1T–$2.5T |

$500 | $100–$125 | potentially ~$3T+ speculative enthusiasm |

$600 | $120–$150 | potentially ~$3.5T–$4T+ speculative enthusiasm |

These are speculative NAV market-implied enthusiasm premiums layered atop already aggressive private marks (actual SpaceX portfolio weight in VCX is still 5% pre IPO). VCX holders are purchasing: scarcity and the belief that future buyers will pay even more.

The Nasdaq Fast Track Listing for SpaceX

Ordinarily, companies of this size endure 4 to 8 week delays from IPO to being listed on the Nasdaq exchange and a lengthy 6 months post IPO before private shareholding lockup agreements expire, before significant shareholdings can float to the public market. The Spacex IPO will essentially cut these times in half, but speed carries consequences. With so few shares trading in June, demand may overwhelm float, creating upward pressure in June, but eventually supply arrives along with share dilution from mid September into early November – or beyond if the GOP loses control with the midterm elections. The potential $4 trillion dollar valuation of the Spacex (June), Anthropic and OpenAI IPO’s (September?) combo and their eventual share lockup avalanche of expirations will add overhead supply risk for the broader market as well in Q4.

Since these large companies remained private for long periods, that means: employees, dozens of venture round funders, secondary investors, private funds, and institutional crossover holders will all await liquidity simultaneously.

The anticipated lockup framework could include staged expirations such as:

Potential Lockup Timeline Structure

Time After IPO | Approx. Shares Unlocked |

|---|---|

30–45 Days | Limited employee liquidity |

60–90 Days | Early VC distributions |

90–120 Days | Secondary institutional unlocks |

180 Days | Major broad unlock |

9–12 Months | Final large insider supply wave |

The cumulative effect could create hundreds of billions in incremental tradable equity entering markets over a relatively compressed period.

Over the past several years, history suggests that large high-profile IPOs have frequently experienced: euphoric early rallies, followed by substantial retrenchments. The average peak-to-trough decline for major speculative IPOs in the last several years has commonly ranged:

20% to 40%

with many declining considerably more before stabilizing.

During the ascent, investors believe they are buying the future. During the decline, they discover they merely borrowed returns from it.

All of these new trillion dollar global tech companies require massive new AI inspired data centers. The genie may be out of the bottle, but the opposition to progress is growing. Today the objections focus on exaggerated fears of electricity demand, water consumption, environmental stress, and fears that hyperscale data centers will inflate utility costs for ordinary citizens. The political resistance to AI infrastructure increasingly resembles earlier American anxieties surrounding railroads, interstate highways, nuclear power, oil pipelines, airports, and the internet itself. Every transformative infrastructure boom eventually collides with a public fear that the machinery powering prosperity may itself become too large, too fast, or too consuming.

Energy prices globally will rise regardless due to global expansion, but many of the major datacenter concerns are already being mitigated by evolving technology and policy. The newest generation of hyperscale AI campuses increasingly incorporate:

dedicated natural gas generation,

closed-loop cooling systems,

wastewater recycling,

SMR-ready nuclear integration,

battery buffering,

and direct compensation agreements protecting local utility ratepayers.

Yet, it may surprise many to know that a recent Gallup poll in March illustrates that not only are most people opposed to building data centers, but would rather live near a nuclear power plant (53% opposed) than a data center (71% opposed).

Missouri: A Case Study in the New Industrial Policy

In Missouri — roughly an hour from St. Louis — proposed combined investments from Amazon and Google associated with AI and hyperscale data infrastructure reportedly approach $50 billion.

The projects increasingly incorporate:

independent or dedicated energy sourcing,

water recycling systems,

closed-loop cooling,

wastewater reuse,

and local compensation structures designed to insulate residents from rising utility costs (Google will create a $20 million fund to compensate rate increaes and improve local residential power use.)

The politics surrounding AI infrastructure increasingly resemble earlier American resistance to:

railroads,

pipelines,

airports,

interstate highways,

and industrial manufacturing expansion.

Eventually economic gravity tends to prevail as communities ultimately compete for investment once employment, tax revenue, infrastructure improvement, and secondary development become visible.

Two Peaks, Then a Reckoning?

The most probable path for markets may not be an immediate collapse, but a two-stage speculative climax.

Phase One — June:

SpaceX mania, Nasdaq melt-up and a scarcity-driven euphoria

Phase Two — September

OpenAI IPO and Anthropic IP trigger a second speculative acceleration and retail participation climax

Then:

expanding supply,

lockup expirations,

insider selling,

valuation fatigue,

and growing election uncertainty into the November midterms.

This sequence could create a higher-risk market environment from September into Q4,

with the potential for a broader market correction, particularly within momentum-heavy AI and technology sectors.

That does not invalidate the long-term AI revolution. It merely reminds investors that even transformative technologies obey liquidity cycles. We concur with the consensus that this secular wave is still in its formative stage with a tsunami climax somewhere over the horizon.

The larger reality, however, is geopolitical. The AI buildout is not merely an economic race between American corporations competing for market share. It is increasingly a strategic competition among nations for technological dominance in the 21st century.

Whoever leads in:

cutting edge AI,

reasoning systems,

robotics,

semiconductor,

quantum computing,

autonomous defense systems,

and cyber infrastructure

may ultimately write the operating rules for much of the global economy as well as the ability of bad actors to dictate massive geopolitical leverage over our existence. Anthropic’s most advanced Mythos model revealed that users can exploit vulnerabilities faster than they can be defended, and consequently is being limited for use by our mission critical security infrastructure first before sharing with the world. America cannot afford to slow the AI race while adversaries accelerate. The same tools that may expose vulnerabilities are also the tools needed to defend banking rails, power grids, defense networks, and financial markets.

This is why the pace of capital spending continues accelerating despite political criticism. American hyperscalers are not merely competing against one another. They are competing against national-scale industrial policies in countries such as China, where artificial intelligence, quantum computing, semiconductor independence, and cyber warfare capability are increasingly viewed as matters of state security.The stakes extend well beyond advertising algorithms and chatbots.

The next generation of AI and quantum-enabled systems may determine:

financial system resilience,

cyber defense superiority,

military targeting capability,

encryption dominance,

energy-grid security,

and protection against increasingly sophisticated digital sabotage.

A nation that falls materially behind risks technological dependency upon strategic rivals. The danger is not simply economic stagnation. It is vulnerability. An adversarial state possessing overwhelming AI and quantum superiority could theoretically cripple banking systems, disable military systems, or hold entire economies hostage through cyber coercion. This reality increasingly explains why AI capital expenditures continue expanding at extraordinary rates.

Across the hyperscaler ecosystem, AI-related infrastructure spending is now growing approximately:

40%–50% annually

despite already historic spending levels.

AI Capex Is Surpassing Cash Flow

Projected 2026 AI-related capex:

Company | Estimated 2026 AI Capex |

|---|---|

Amazon | ~$200B |

Microsoft (MSFT) | ~$170B–$190B |

Alphabet | ~$180B–$190B |

Meta (META) | ~$125B–$145B |

Combined: roughly $650B–$750B this year and possibly $1 trillion+ in 2027.

The United States has effectively entered a modern industrial mobilization race — not unlike prior strategic races involving the military: Only now the factories are data centers, the ammunition is compute power, and the battlefield is increasingly digital.

The stock market now approaches what may become the defining speculative crescendo of this cycle — a June-to-September climax spanning the Age of Rockets and the Age of Reasoning. June may belong to SpaceX and escaping the gravity of rational valuations. September may belong to Anthropic and OpenAI, where Claude and ChatGPT increasingly symbolize synthetic cognition becoming commercial infrastructure. The speculative fever surrounding these offerings may ultimately propel the S&P 500 toward and perhaps beyond the 8,000 threshold before this portion of the cycle fully exhausts itself in the weeks ahead . Yet history suggests that periods of technological ecstasy are eventually followed by periods of digestion. The likely path remains one of mounting volatility, with heightened risk surrounding July and especially October into the midterm elections — or later still should political power shift and fiscal or regulatory uncertainty intensify. Valuations may become temporarily unreasonable before supply, lockup expirations, and political anxieties restore sobriety. But even after a deeper correction and consolidation phase, the larger trajectory of the AI era likely remains intact. The next technological wave will eventually emerge from the rubble of excess enthusiasm, just as prior industrial revolutions did before it.

Comments

Log in or sign up to join the conversation.