Technology stocks remained under pressure on Friday, extending a sell-off that has spread from Wall Street into Europe and Asia. The retreat reflects a combination of factors. After a remarkable rally in recent months, investors have become increasingly sensitive to stretched valuations, rising infrastructure costs associated with AI, and a more hawkish outlook for US monetary policy. While some degree of profit-taking was perhaps inevitable, the latest moves also raise broader questions about whether expectations for the sector have simply run too far ahead of commercial reality.

For now, Nasdaq 100 futures pointed lower, while major regional equity markets also declined, as investors continued to reassess the lofty expectations underpinning the artificial intelligence trade.

Rising costs cast a shadow over Big Tech

The pressure intensified following Thursday’s session on Wall Street, where Apple led declines after announcing price increases for its MacBook and iPad ranges, citing higher component costs, including semiconductors. The stock fell 6%, overshadowing stronger-than-expected earnings from Micron.

The market reaction suggests investors are becoming increasingly concerned that higher semiconductor costs could begin to erode margins across the technology sector. Companies have been willing to absorb rising expenditure in pursuit of AI leadership, but there are growing signs that those costs are becoming more difficult to ignore.

That theme continued into Friday’s trading. Several US chipmakers were among the key premarket movers, while European semiconductor stocks also opened lower. In Asia, SoftBank Group tumbled by double digits, leading a broader decline across the region’s technology sector as investors questioned whether current levels of AI investment remain sustainable.

Momentum reverses

The latest weakness has significantly altered the picture for US technology stocks. The Nasdaq has fallen more than 4% this week, wiping out the previous week’s gains and pushing the index into negative territory for June, following two exceptionally strong months in April and May.

While the scale of the decline is notable, it also reflects how concentrated market gains had become around a relatively small group of AI-linked companies. As valuations expanded, the margin for disappointment inevitably narrowed.

The AI investment question

At the heart of the debate is the sheer scale of capital being committed to artificial intelligence. The sector has attracted trillions of dollars of investment, yet profits have yet to emerge on anything like the same scale.

Critics argue that the industry now faces mounting pressure to justify those spending levels within a relatively short timeframe. Unlike earlier technological revolutions, today’s investment cycle is exceptionally capital-intensive, requiring vast expenditure on chips, data centres and electricity before meaningful returns can be generated.

The concern is not whether AI will ultimately transform the economy, but whether businesses and consumers will generate sufficient demand quickly enough to support current valuations. If monetisation takes decades rather than years, today’s level of spending may prove difficult to sustain.

Higher rates add another headwind

The reassessment of AI comes as investors also contend with a shifting interest rate outlook. Expectations for further policy tightening have increased after Federal Reserve Chair Kevin Warsh reiterated the central bank’s commitment to bringing inflation under control.

Higher interest rates would increase borrowing costs across the economy, posing an additional challenge for companies undertaking large-scale AI investment programmes. For a sector whose future depends on sustained capital expenditure, tighter financial conditions could make investors less willing to overlook the absence of near-term earnings.

Taken together, rising costs, elevated valuations and a less accommodating monetary backdrop have prompted investors to reassess one of this year’s strongest market narratives. Whether the current pullback proves to be a healthy correction or the beginning of a more prolonged repricing will depend less on AI’s long-term promise than on its ability to deliver tangible profits in the near future.

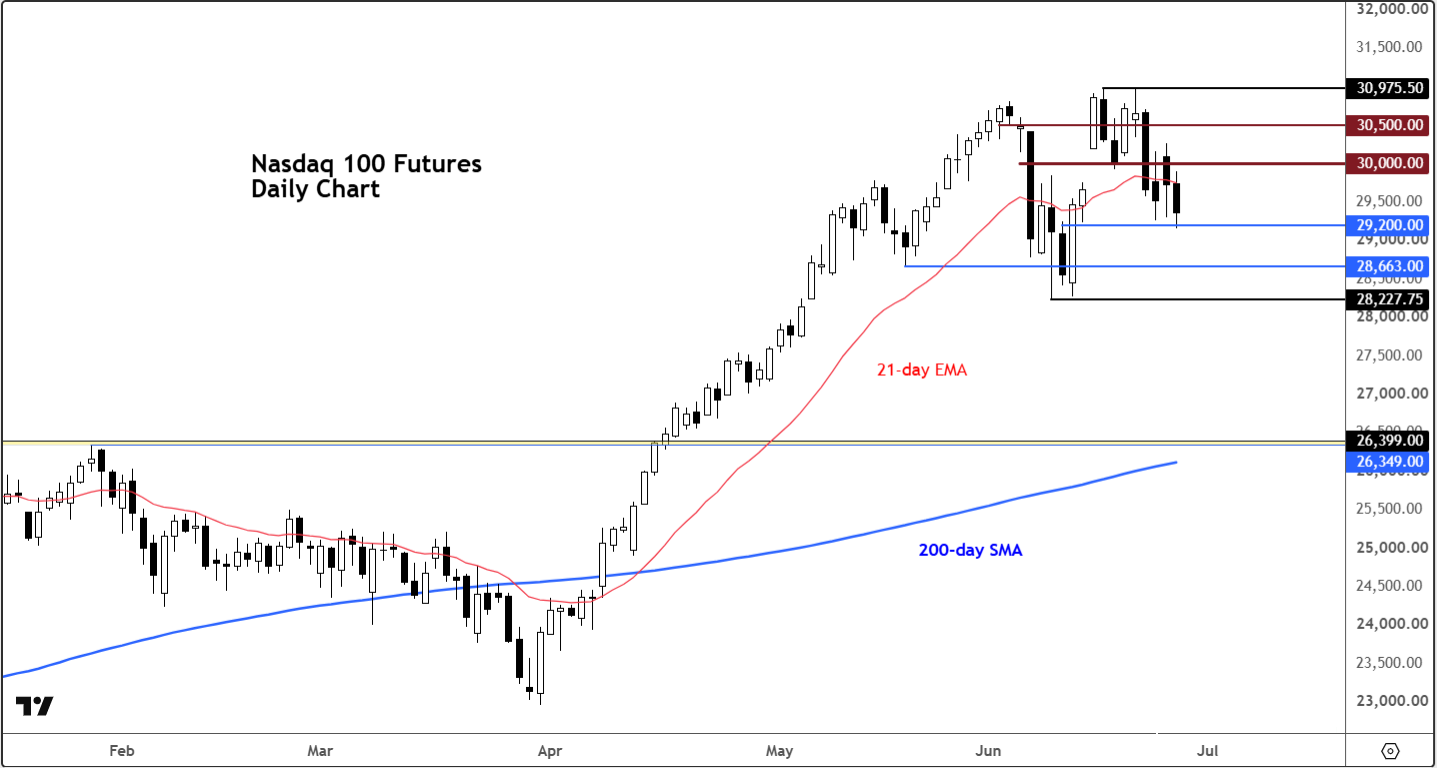

Nasdaq 100 technical analysis

From a technical point of view, the chart for the Nasdaq 100 futures is starting to look a little more bearish. The index has now fallen back below the 21-day exponential moving average and has formed a couple of lower highs and a couple of interim lower lows.

That said, I wouldn’t say we’re in corrective territory just yet, as none of the major support levels have broken down. However, that could change if we don’t see the return of the dip-buying mentality over the coming days.

For now, consolidation remains the name of the game, although the directional bias has turned slightly bearish.

In terms of key levels to watch, resistance on the upside comes in around 30,000, which previously acted as support last week before giving way during this week’s sell-off. Above that, 30,028 is the next level of potential resistance. This was a support level on Monday before it was broken during Tuesday’s sell-off. As is often the case, former support can turn into resistance when approached from below.

Beyond that, 30,500 marks the next area of potential resistance, followed by the all-time high at 30,756.

On the downside, 29,000 is the first support level to watch, and it was being tested at the time of this writing. Below that, 28,570 is another important support area. The most recent swing low from earlier this month sits around 28,190, and that is now the line in the sand. A break below that level would be viewed as a bearish technical development and could pave the way for further selling pressure.

So, let’s see whether that level holds. If it doesn’t, we’ll reassess the outlook from there. Things could become a little more bearish should that happen.

Comments

Log in or sign up to join the conversation.