There are two competing tungsten narratives in the market right now that are at odds, and that matters to investors looking to navigate the current landscape.

One says the price action over the past year was a Chinese export panic that has now cooled down, the other says the move was a repricing of a single-source critical mineral for what it actually is, and any pullback is a diversion along that route. Based on our analysis, Prinsights is in the second camp.

Tungsten is on the U.S. Geological Survey and European Union critical minerals lists. The EU shortlisted it in May 2026 for its first joint critical minerals stockpile. And for good reason.

Tungsten has the highest melting point of any metal, roughly as dense as gold, and is the standard material used for drill bits, machining inserts, armor-piercing tank ammunition, missile and drone components, and chip interconnects. It’s also used to cut silicon wafers in solar manufacturing.

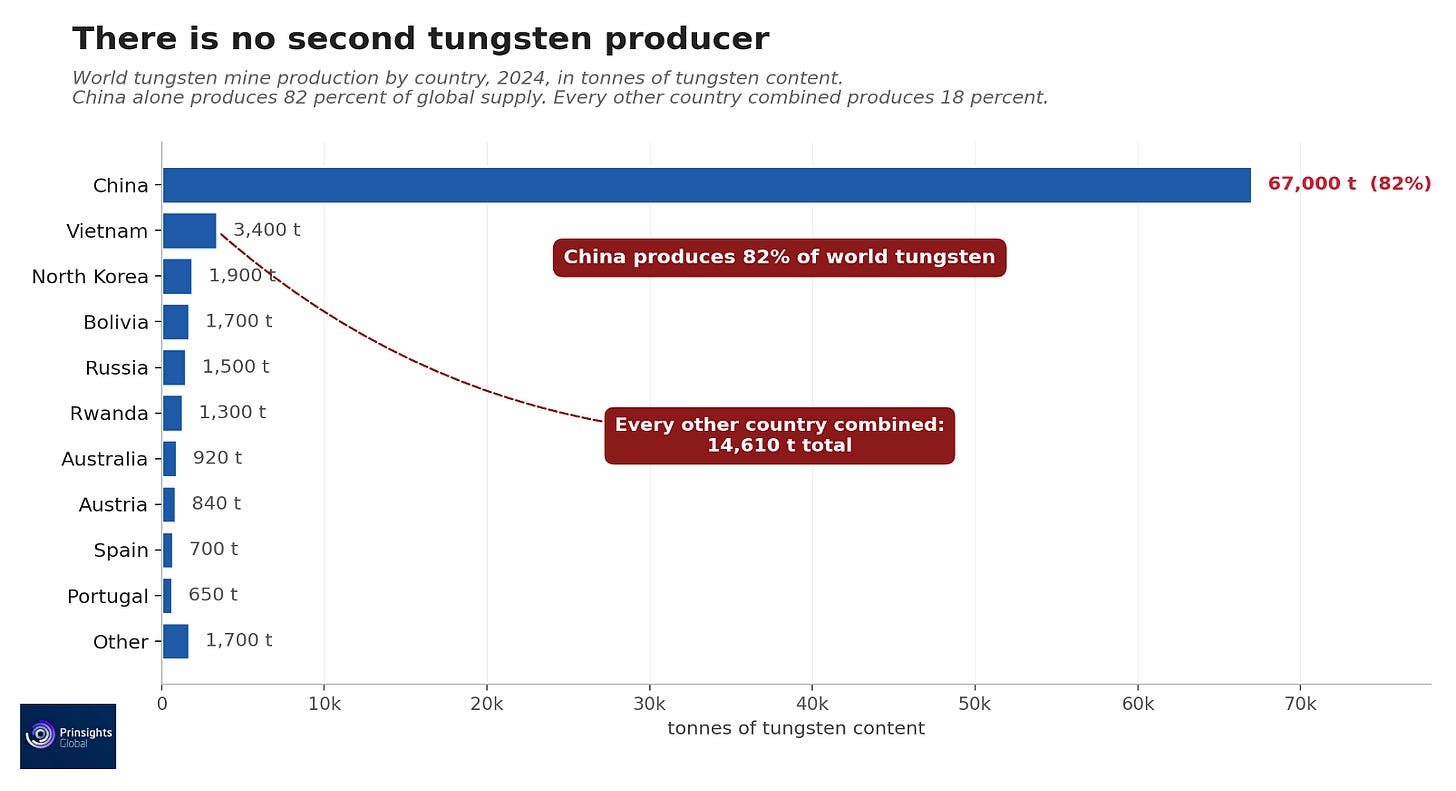

And like with many other metals, China dominates the tungsten supply chain, producing nearly 82% of it and using about half of what it produces.

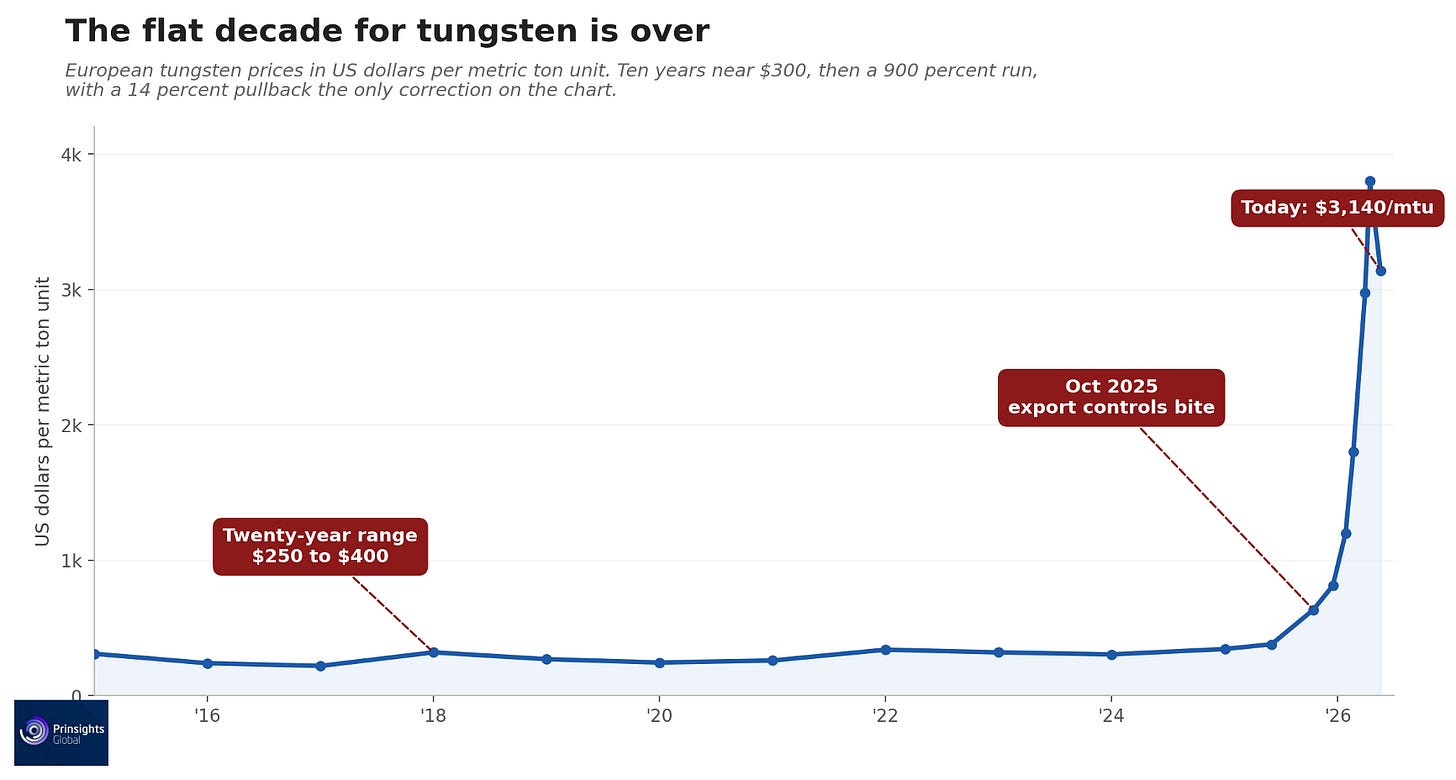

European tungsten prices are trading between $3,000 and $3,280 per metric ton unit. They traded at $850 in December 2025 and at nearly $350 a year ago.

This massive recent price surge is important to consider because the previous twenty-year range was relatively stable at $250 to $400. That means tungsten has been significantly repriced in the past twelve months.

Shanghai Metal Market noted that the upstream tungsten segment had stopped falling after a more than 61% peak-to-trough decline in some Chinese products and started rebounding. The European benchmark dropped 14% below its April peak near $3,800, but as we mentioned above, we consider this dip temporary in the trajectory of tungsten.

Below, we detail the four reasons tungsten has surged and what you need to know.

Four Reasons Tungsten Surged

1. China is The Tungsten Market

China mines 67,000 of the 82,000 tons of global tungsten produced in 2024, or 82% of world output, per the U.S. Geological Survey. Vietnam is second at 3,400 tons. Russia is third at 1,500 tons. The combined output of Australia, Austria, Spain, and Portugal, along with every Western-aligned producing country put together, is 3,110 tons, or under 5% of Chinese production. China also holds 53% of global reserves.

S&P Global concluded in a Q1 2026 tungsten report that even if construction on new Western tungsten mines began today, no meaningful new supply would arrive before 2030.

Yet, inside China, average mined ore grades have fallen from above 0.5% in the 2000s to closer to 0.3% today, which raises the unit cost of every ton mined. That means the supply side is being actively tightened from within the country that controls almost all of it.

2. China Tightened Its Grip on Tungsten Exports

China began tightening its recent campaign to increase control over tungsten exports on February 4, 2025, when the Ministry of Commerce added tungsten to its export control list and required licenses for overseas shipments.

Then, on October 26, 2025, China added tungsten to its Key Export Supervision Catalog. Exporters were then required to undergo quota reviews and obtain additional government approvals before shipments could leave the country.

What started as a licensing requirement morphed into a broader effort to limit and monitor the flow of tungsten out of China. On December 30, China’s Ministry of Commerce listed just 15 companies authorized to export tungsten in 2026 and 2027.

By January 6, 2026, China prohibited exports of tungsten products to Japan for military and military-related end uses. That was a huge slap in the face to Japan, which accounted for 57% of Chinese APT exports in the first eleven months of 2025.

Taking together, these measures did not stop tungsten exports outright. But they did give China more control over who could buy tungsten, who could sell it and where it could go on a global scale.

What’s unfolding is that the flow data is showing the squeeze amplifying. Chinese APT exports fell from 782 tons in 2024 to 243 tons in the first eleven months of 2025, a 69% drop. Canaccord Genuity reported that Chinese exports of key tungsten products effectively fell to zero in March 2025. The first two months of 2026 still showed export volumes down 27.6% year-over-year against a 2025 base that was already heavily compressed.

The supply chain is in a race to find enough tungsten that is not physically available outside China at any price.

3. The Pentagon Just Tightened the Rules on Chinese Tungsten

The U.S. government has spent several years trying to reduce its reliance on Chinese tungsten in defense applications. Under existing Pentagon procurement rules, the Department of Defense cannot purchase tungsten produced in China, Russia, Iran, or North Korea. The restrictions are about to become much tougher.

Starting on January 1, 2027, those rules will apply to where tungsten is mined, refined, or separated, not just where it is produced. The Pentagon is effectively extending its ban to the entire upstream supply chain.

The change also closes a long-standing loophole. In the past, many commercial off-the-shelf products containing Chinese tungsten could still find their way into defense supply chains. Under the new rules, that exemption will no longer apply to products that are 50% or more tungsten by weight.

For defense contractors, the message is becoming very clear. Within six months, any tungsten-heavy component entering the U.S. defense supply chain will need a non-Chinese, non-Russian, non-Iranian, and non-North-Korean source across the entire upstream chain.

Demand beyond defense is moving in the same direction. The global semiconductor industry uses tungsten in chip interconnects and advanced packaging, and equipment sales are forecast to climb from $145 billion in 2026 to $156 billion in 2027, driven by AI accelerator and memory build-out.

Japanese chipmakers were told in April that tungsten delivery cycles had stretched from three months to nine. Germany’s next-generation Leopard 2 ammunition, the KE2020Neo, uses a new high-strength tungsten alloy penetrator, the same tungsten-based approach Germany has taken since the DM33 round and the one the UK is adopting for the new Challenger 3 tank.

Every one of those demand sources is either mandated by law, locked in by capacity decisions, or has no substitute that works.

4. The July 13 Section 232 Report Can Only Make This More Bullish

President Trump signed a proclamation on January 14, 2026 that ordered Commerce Secretary Howard Lutnick and U.S. Trade Representative Jamieson Greer to negotiate critical minerals trade agreements with foreign governments and report back within 180 days. That report is due July 13. Tungsten is one of the 50 minerals in scope and this year’s squeeze makes it a glaring target for action.

The proclamation explicitly leaves Lutnick four tools to use if the negotiations are not enough. Tariffs on imported tungsten products. Minimum import prices, which would set a price floor below which foreign tungsten cannot enter the U.S. market. Quotas. Or further Section 232 actions.

At the Critical Mineral Ministerial in Washington on February 4, senior administration officials laid out plans for an allied trade bloc built around reference prices and price floors, and named tungsten as one of the markets they have in mind. None of the four tools is bearish for U.S.-aligned tungsten producers.

The price retracement we are looking at right now is happening before the report lands, not after. And that’s where the opportunity is.

What This Means for Investors

Tungsten is a metal that cannot be substituted, mined fast enough or imported from anywhere in a meaningful way, outside of one country. U.S. defense procurement law now bans the Chinese product.

Ultimately, the July 13 report has no bearish outcome. The 14% pullback that has the consensus calling a top is happening inside the most bullish setup the metal has seen in two decades.

Comments

Log in or sign up to join the conversation.