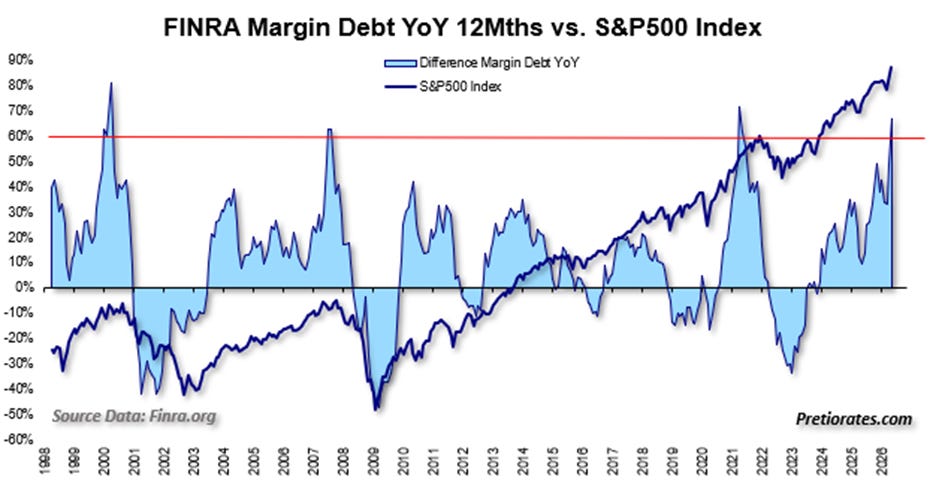

In last week’s thoughts, we pointed out that a long-term but very reliable indicator had generated a sell signal. Margin debt—that is, stock investments made on credit—has grown by more than 60% over the past twelve months. A classic sign of greed—that magic word that, at the end of a major uptrend, almost always eventually takes control away from caution. And remember: Investors who use borrowed money to invest don’t have much staying power.

Even though last week’s commentary explicitly mentioned a long-term sell signal, sentiment in the financial markets has since taken a new turn—with immediate and, in some cases, dramatic effects on precious metals, stock markets, and market interest rates. The trigger: the new Fed Chair.

When war broke out in Iran, the general narrative was: “Higher oil prices = higher inflation = higher interest rates = bad for precious metals.”

This market formula has thus shifted to “lower oil prices fuel demand in an economy that’s already running hot—and that drives inflation even higher.” And, as is well known, inflation is combated with higher interest rates, which led to a painful sell-off in precious metals.

This week, we want to focus on the strength of the U.S. economy. But first, let’s address the most pressing of all questions: Have precious metals hit bottom?

With a little help from traditional technical analysis and Fibonacci numbers, there’s a very good chance that the pain for gold bugs should now slowly begin to subside. Today, the gold market touched—and confirmed—a very important support level at USD 3,960: the yellow line, which has already proven itself multiple times as both resistance and support, as well as the purple 0.618 extension line. 0.618 is a well-known mathematical number from the Fibonacci sequence, aptly named the “Golden Ratio.” Fibonacci numbers are particularly effective when emotions are running high in the markets.

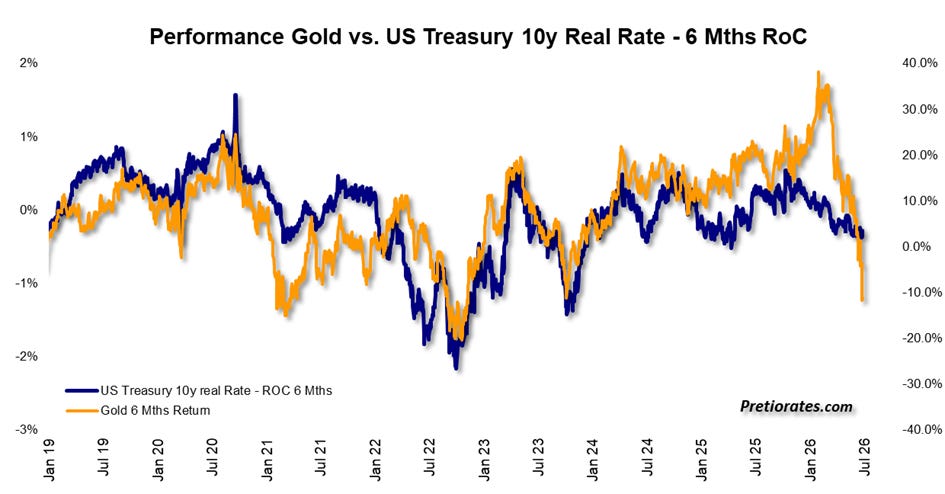

The fact that the gold price has now overshot on the downside is also evident from its correlation with percentage performance over the past six months—just as it overshot on the upside in early year.

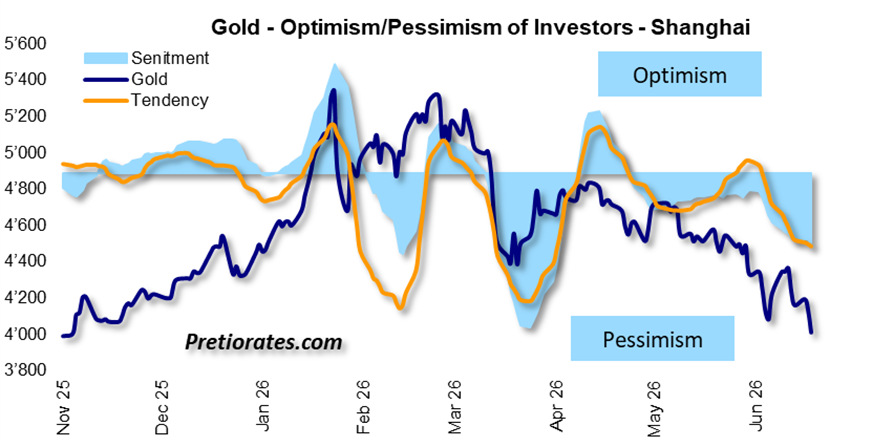

Pessimism in the gold market has recently intensified even in Shanghai, despite the fact that the Chinese central bank, the PBoC, imported 163 metric tons last month—the highest volume in two years.

During the first five months, the central bank’s imports rose by no less than 76% compared to the previous year. This puts us back in a situation similar to two years ago: physical gold is flowing from the West to the East—even as prices fall.

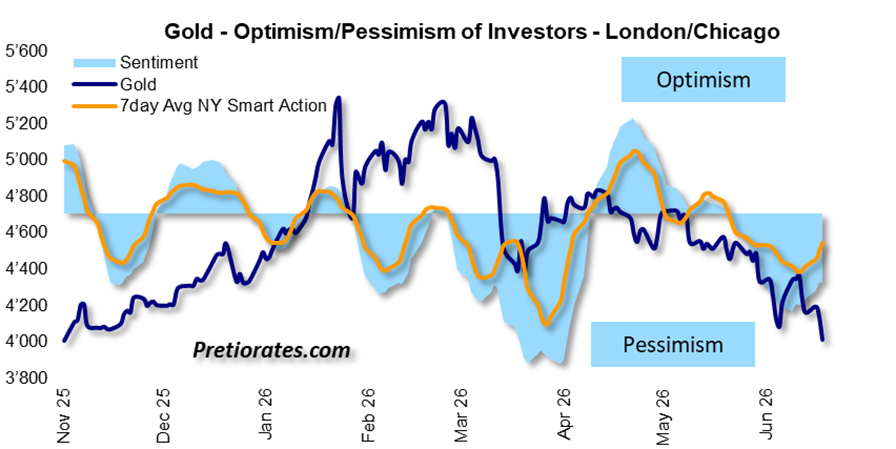

What is surprising, however, is the shift in sentiment in the West: after being deeply pessimistic until recently, sentiment now appears to be brightening. An important prerequisite for market prices to rise again…

Another factor that should act like aspirin: EquityClock.com tracks price movements over several years—in this case, over 20 years. According to this seasonal analysis, gold tends to rise on average from July through August.

In the short term, however, the gold price is likely to remain constrained by the interest rate environment. Since Fed Chair Harsh’s first appearance last week, the market has been anticipating at least one interest rate hike this year, possibly even two.

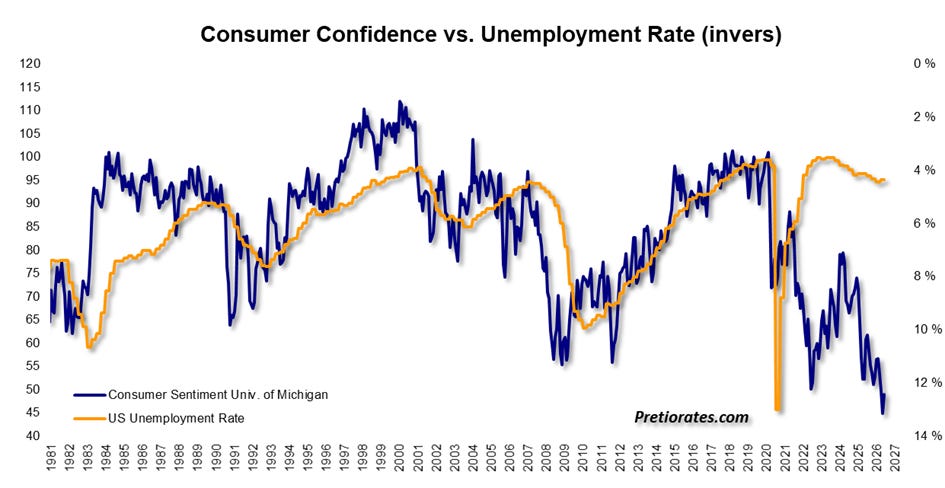

A strong U.S. economy and, consequently, rising interest rates? That doesn’t align at all with the University of Michigan’s consumer sentiment index, which recently hit a new low.

Yet the vast majority of recent U.S. economic data has come in stronger than expected. Of course, much of the credit for this goes above all to AI companies, which invest several hundred billion annually. This leaves fewer jobs for private consumers, which explains the subdued sentiment.

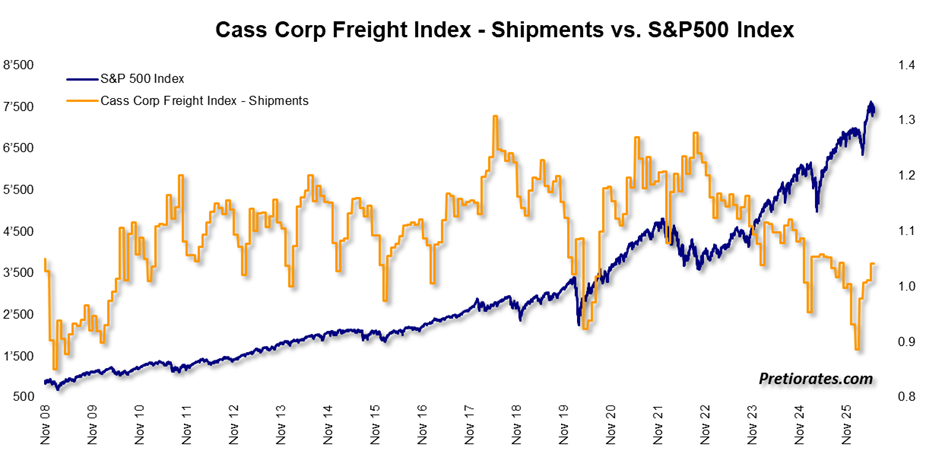

But it’s not just the AI companies: The Cass Corp Freight Index has also risen sharply in recent months. This index indicates whether more or fewer goods are being transported in North America. When it rises, it suggests that corporate business is doing well.

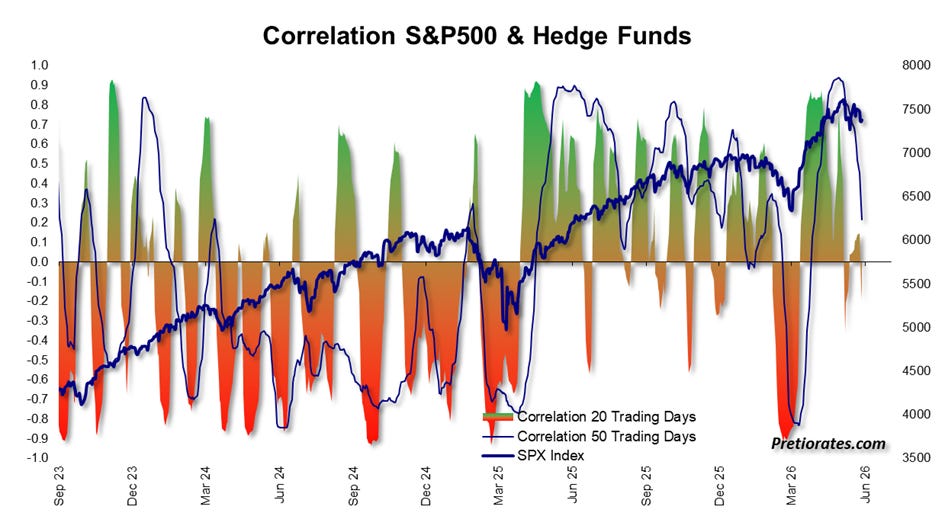

It’s therefore no surprise that investors have recently become more cautious. Hedge funds have now neutralized their above-average equity investments.

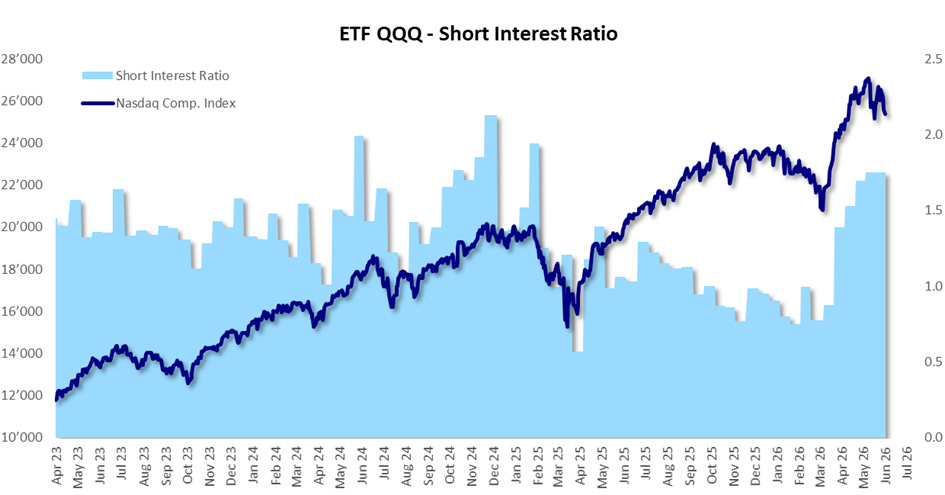

Short positions in the very large Nasdaq-100 ETF QQQ have been massively increased since the start of the last uptrend at the end of March…

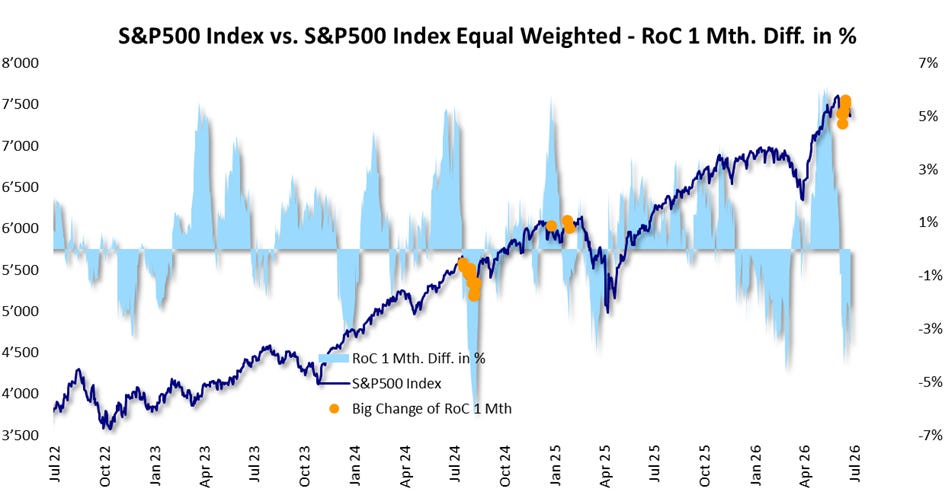

And market breadth within the S&P 500 has eroded significantly in recent days and weeks.

Bottom Line: The start of a Wall Street correction might be coming sooner than expected after all. Whether interest rates will actually rise remains to be seen. Rising interest rates would also bring the issue of government debt back into the spotlight—which, in principle, should also be a positive for gold.

If you enjoyed this issue, please click on the Like icon at the top or at the bottom of this email. This is very important in helping our Thoughts gain more followers. And don’t forget to recommend us - with the button below. Thank you!

Comments

Log in or sign up to join the conversation.