For the first time since the dollar’s link to gold was cut in 1971, gold now sits atop the world’s official reserves. The European Central Bank (ECB) confirmed it on June 2 in its annual report on the international role of the euro. At the end of 2025, gold made up 27% of global official reserves by market value, ahead of U.S. Treasuries at 22% and the euro at 15%.

Dollar-denominated assets combined still hold the largest overall share at around 42%, so the dollar has not been displaced. What has changed is the standing of gold on its own, as the single reserve asset that central banks now hold more than any other.

The ECB Made It Official

The ECB attributed much of gold’s larger reserve share to valuation math. Gold rose roughly 60% in 2025 after gaining about 30% in 2024. On that basis alone, its share of any reserve pool would climb even without a single new purchase. And while that explanation is accurate, it is not quite the full story. The more useful question to consider next is why central banks continued buying through that advance instead of taking profits into it.

The answer becomes clearer just by looking at the global marketplace. That’s because strategic demand remains strong. Central banks bought 863 tons of gold in 2025, well above the 473 ton average of the prior decade, in a year when the metal set a whopping 53 record highs. That buying continued into 2026 even as the price rose further before it corrected.

The latest World Gold Council projections show another 750 to 850 tons of official purchases this year, with economic powerhouse China and India driving momentum along with continued accumulations by Turkey, Poland and Singapore. Yet, the narrative does not stop there. Once again, among the steady buyers are Saudi Arabia and the United Arab Emirates, which are all exploring new allocations.

The ECB report measured reserves at the end of 2025, so it captured a position still in progress. That matters because central bank buying has continued into 2026, including through the spring correction earlier this year. The motivation remains the same: reducing dollar concentration, managing actual and potential sanction risk and anchoring monetary policy in real assets.

Prinsights made this call in our January commodity forecasts, when gold was setting records above $5,000. At the time, we offered that central bank gold holdings were on course to overtake U.S. Treasuries as the more important reserve anchor. The ECB has now put the official collective weight of Europe behind that shift.

Rich Checkan at Asset Strategies International has described the same divide this week. While investors wait for the next FOMC meeting and trade the geopolitical headlines, he noted that central banks have continued to accumulate gold and reduce dollar reserves.

“Investors have been shy to buy gold in this ongoing pullback, but central banks know there’s peace of mind to be had with a strong allocation to gold in these trying times.”

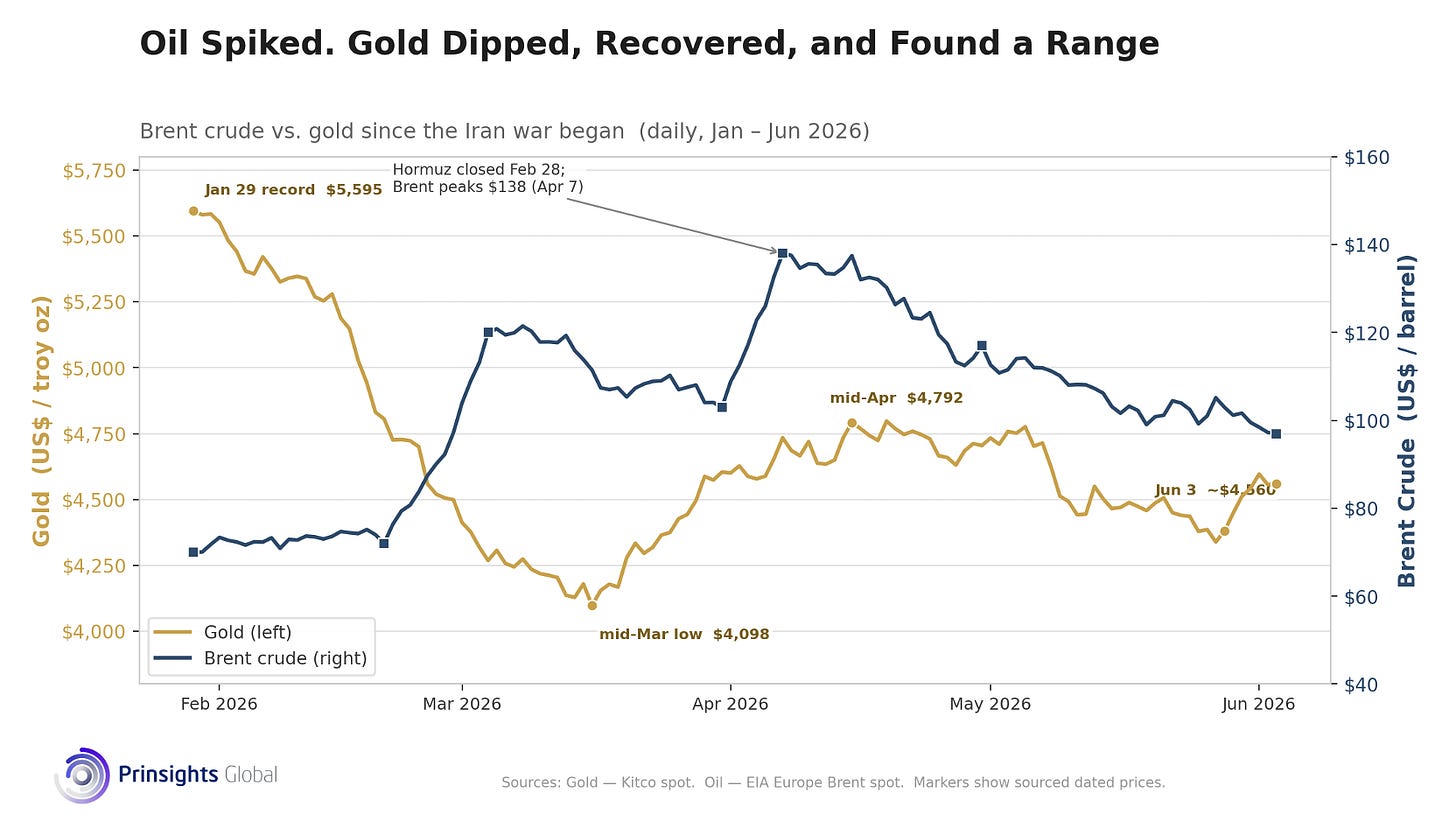

Oil Spiked. Gold Dipped, Then Found a Range

When the Iran war began at the end of February, oil moved the way it always does during a Gulf region crisis. With the Strait of Hormuz still effectively closed and roughly a fifth of global supply disrupted, Brent jumped from around $72 before the conflict to a March average near $103, then spiked to a $138 peak in April. It has since come back to about $97 as ceasefire talks remain in the balance, but are not yet resolved.

Yet gold followed a different path.

After setting a record of $5,595 on January 29, it sold off hard as a hawkish Fed nominee lifted the dollar, and an oil-driven jump in inflation stripped the market’s rate-cut expectations. The low came in mid-March near $4,098, a drop of more than a quarter from the peak that held above the long-term trend line. From there, gold recovered to $4,792 by mid-April and has traded in a $4,400-4,800 range since, sitting near $4,560 now.

That is the kind of correction gold has worked through repeatedly in this bull market, and Kitco, one of the primary outlets that covers gold and metals, itself has analysts who describe the current zone as a strategic accumulation window.

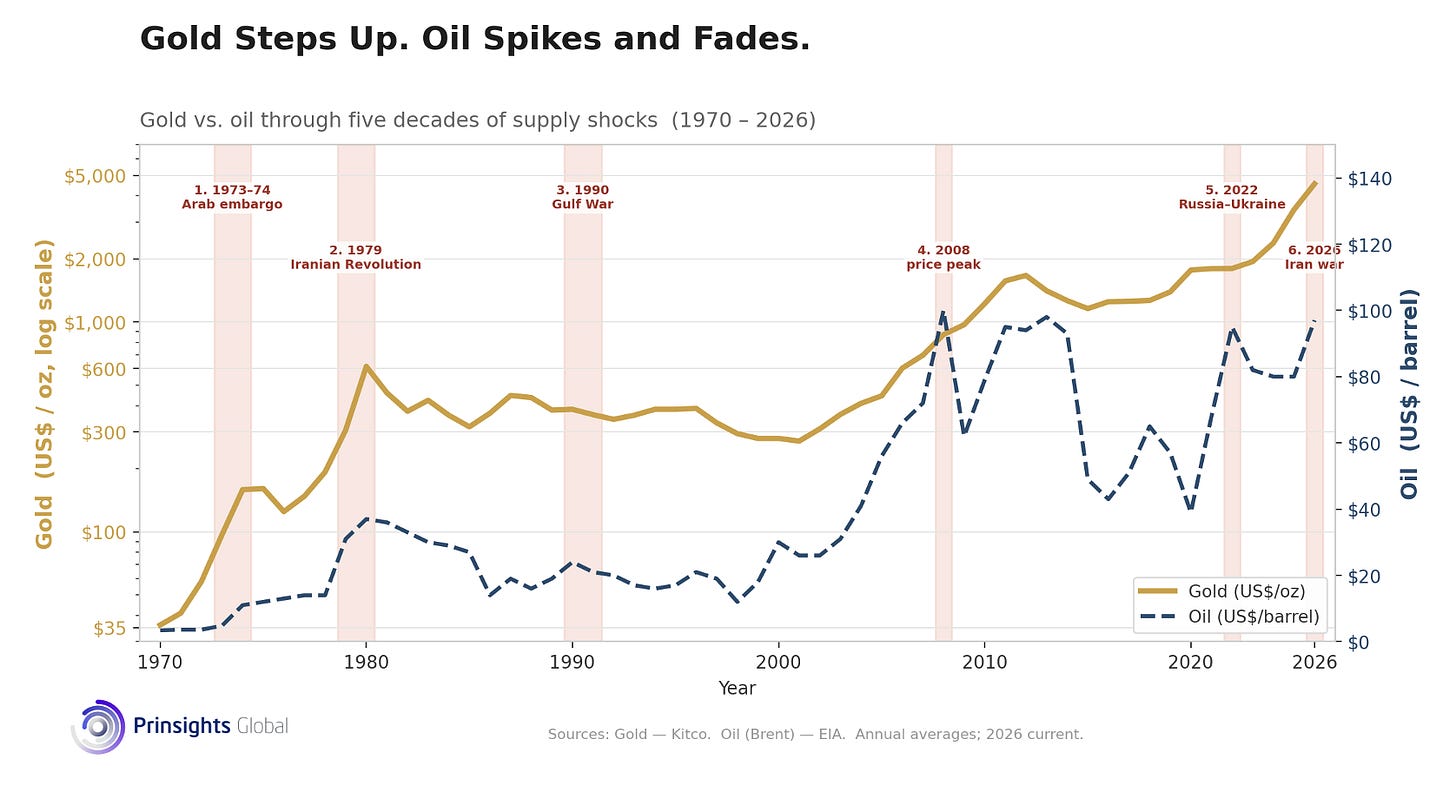

This behavior happened in multiple past periods, including the 1973 embargo, the 1979 Iranian revolution, the 1990 Gulf War, the 2008 financial crisis and the 2022 escalation of the Russia invasion of Ukraine.

Every major geopolitical oil disruption produced a crude oil price spike that later faded. Gold, however, moved higher in steps and kept the gains, because the forces behind it, monetary credibility and reserve demand, build on themselves rather than reversing.

The 2026 Iran war is the newest entry in that pattern, and the ECB milestone is the clearest confirmation of it yet.

None of the near-term volatility changes that. Gold is consolidating for now, the war will capture headline attention, and the Fed will remain caught between keeping related inflation contained and worrying about the high debt-servicing cost the U.S. faces, while fewer central banks are buying U.S. Treasury debt.

That’s why going beyond the headlines matters. Underneath it, the buying that the ECB just measured is still going on, and the institutions anchoring it are the largest, most motivated and best informed in the market.

With that demand intact and momentum building, Prinsights is reiterating our target of $6,000 an ounce for this year. We also continue to treat the current range near $4,560 as a level to accumulate gold and select gold miners rather than wait on the sidelines.

Comments

Log in or sign up to join the conversation.