Photo by Yashowardhan Singh on Unsplash

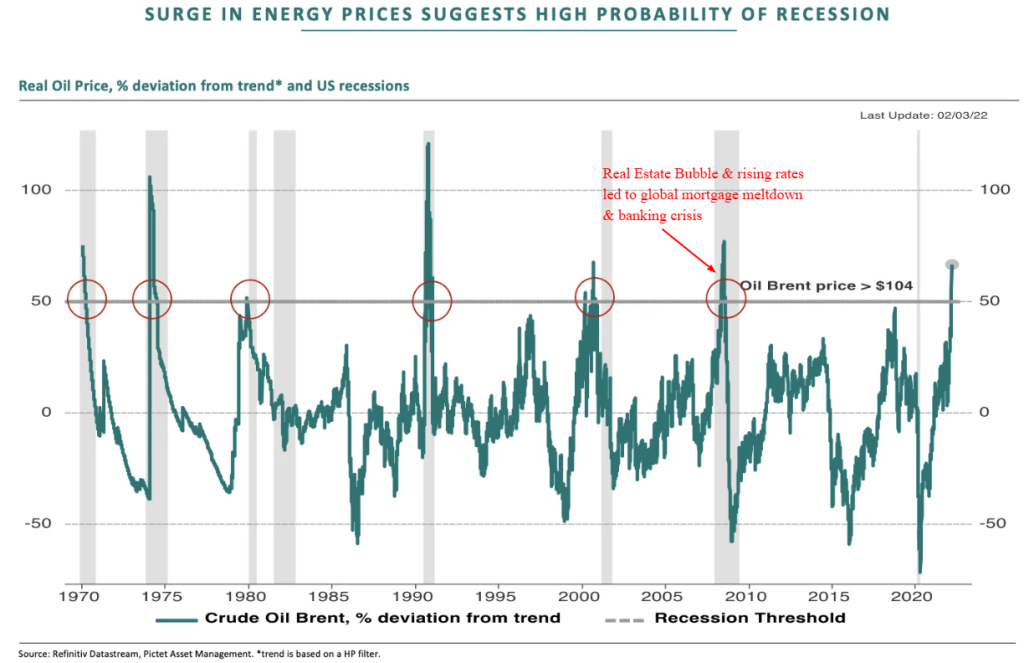

History occasionally compresses itself into geography. Religion, commerce and empires sometimes converge upon an inconveniently narrow place. Occasionally, a strip of water, such as the Strait of Hormuz in the Persian Gulf, becomes a fulcrum of the global economy. In ancient times it was spice traders and today this chokepoint of waters now carry supertankers of fuel supplying 20% of the lifeblood of global economic arteries. Geography here concentrates the interests of distant nations into a small and combustible space. The Persians guarded this strip. The British kept it open and the United States now secures it. When tensions rise here, oil prices react, stock markets tremble, and suddenly world leaders rediscover their interest in geography. The Strait is a pressure valve for global commerce. And at moments such as this one, when missiles fly and tankers seek safe harbor, history is compressed into twenty miles of water between panic and prosperity. The Strait of Hormuz carries roughly 20 million barrels of oil per day, about one-fifth of global petroleum supply, making it the most critical energy choke point on earth.

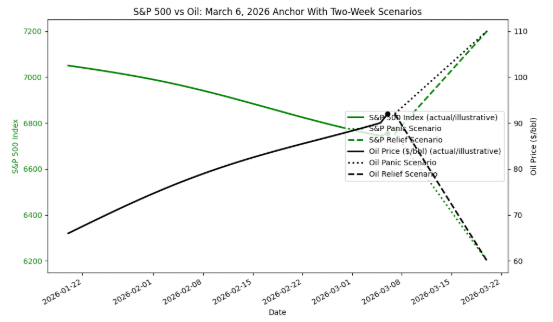

War has returned to that narrow waterway and markets have reacted accordingly, with Oil at 2 and a half year highs and stocks testing 6 month lows. Normally such a spike is one the precursors to an impending recession. If this inflationary surge is brief, then our favored outlook avoids recession. If Iran can keep the Strait mostly closed for months, with Oil remaining near current levels or higher, then the economy will slow, stocks will stall and Trump’s GOP will lose the November midterms.

The Rapid Decline of Iran’s Counterstrike Capacity

The military tempo of the conflict has been intense. Allied forces have reportedly struck over 4,00 Iranian military targets, destroying Iran’s air defenses, radar network, naval capability, and missile infrastructure. Iran responded with a furious opening barrage that has quickly dwindled to a whack a mole irritant.

Metric | Early War Peak | Current Estimate | Decline |

|---|---|---|---|

Ballistic missile launches/day | ~300+ | 20–50 | ↓ 85–95% |

Drone launches/day | ~400 | ~25 | ↓ ~95% |

Cyber attacks | Peak Day 1 | ~10% of peak | ↓ ~90% |

The sharp decline in Iranian strike capacity suggests their missile stockpiles and launch infrastructure may already be reduced by more than half and without many launchers, their ability to strike back is becoming more like guerilla warfare with limited supply chains rather than a national military contest.

The Interceptor Economy

Modern war increasingly resembles an industrial contest. Iran fires ballistic missiles and drones. The United States and its allies fire interceptors. Factories— humming in Arizona, Alabama, Arkansas, and Texas—become as decisive as fighter/bomber squadrons as the US is consuming weapons much faster than they can be produced and at far greater cost than the missiles and drones they are intercepting.

Production of key missile defense systems is already accelerating and the President is presenting public calm, while gritting his teeth and strenuously whispering to manufacturers to step on the gas pedal.

Interceptor | Pre-War Annual Production | Current Rate | 7-Year Target |

|---|---|---|---|

Patriot PAC-3 MSE | ~270 | ~620 | 2,000 |

THAAD | ~96 | ~96 | 400 |

SM-3 Block IB | 36–48 | ~60 | 72–240 |

AMRAAM | ~1,200 | ~1,900 | 2,400 |

Yet the coming ramp-up presents a quieter challenge. America’s defense giants—principally Lockheed Martin and Raytheon—must now find hundreds of skilled engineers, machinists, and electronics specialists while simultaneously expanding their supply chains. Advanced guidance systems, rocket motors, radar components, and rare-earth magnets do not materialize overnight – and China still controls rare earth. Wars may be fought by soldiers, but they are sustained by supply chains.

Oil: The Market’s Panic Barometer

Commodity markets are notoriously unemotional—until suddenly they are not. The escalation of conflict has pushed crude oil sharply higher. Oil surged above $92 per barrel today, with weekly gains approaching 40%, as shipping disruptions and production cuts ripple through global markets.

Shipping traffic through Hormuz has collapsed.

Tanker transits dropped from roughly 24 ships per day to essentially zero.

Hundreds of tankers remain stranded or waiting offshore.

Kuwait are shutting down production due to storage constraints and halted exports and within days others will follow.

The resulting supply shock has already removed millions of barrels per day from global markets.

Markets reacted predictably:

Oil prices surged $27/barrel

Stocks fell 4%

Shipping insurance costs exploded

Then for a moment, politics intervened. The White House announced a plan to replace private shipping insurance—traditionally provided by Lloyd’s of London—with U.S. government war-risk coverage, accompanied by naval escorts for tanker traffic. Markets partially recovered within hours and fell back under $80 for a blink of an eye, but hopes were dashed when the explosive reality was that Iran’s firepower may have declined 90%, but their ability to slip past US defenses to strike tankers and storage facilities on a daily basis this week continues. Like passenger planes, these Oil tankers need error free transit and proof that military escorts will work. Iran knows they will lose the battles, but hope to persist in a war of attrition, with the paralysis of the Strait of Hormuz as the measure of their might.

The First Tanker Test

Eventually the market will look for something more convincing than policy announcements. Sooner or later a tanker convoy will attempt passage through the Strait of Hormuz under naval protection. That voyage will become the war’s first major economic litmus test.

Scenario | Oil | Stocks | Commodities |

|---|---|---|---|

Strait reopens safely | Oil returns toward $60–70 | Bull market resumes | Metals stabilize |

Limited disruption | Oil $90–110 | Volatile correction | Gold rises |

Prolonged shutdown | Oil > $120 | Global recession fears | Commodity shock |

Markets today appear to be wagering—tentatively—that the first scenario will prevail. However, as Oil prices rise, that courage will fade to fear.

The Broader Strategic Chessboard

Several geopolitical consequences may already be emerging from this war outside the battlefield.

Russia’s Drone Supply Chain

Iran has been a major supplier of drones used by Russia in Ukraine. Damage to Iranian production facilities could sharply reduce that supply and stall Putin.

China’s Energy Dependence

China imports large volumes of oil from both Iran and the Persian Gulf. The disruption of Iranian exports—combined with the curtailment of Venezuelan flows—places two important energy sources under Western – or rather US – influence.

Taiwan Deterrence

There is a subtler strategic signal here as well. If the United States and its allies can effectively cripple Iranian military infrastructure and control maritime energy routes in the Persian Gulf, Beijing may take note. The demonstration that Washington can disrupt key energy flows could serve as a deterrent to Chinese ambitions toward Taiwan.

Interestingly, today’s reports that China may soon announce a large order for as many as 500 Boeing aircraft may hint at a temporary thaw in geopolitical tensions. Energy security and military deterrence are rarely separate discussions. Boeing continues to be one of our favorite stocks over the next year.

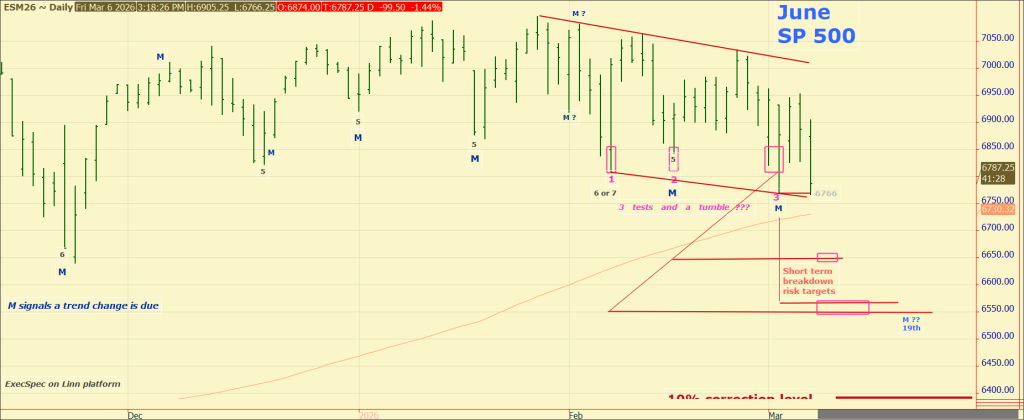

Financial markets attempt to quantify uncertainty

The S&P 500 currently sits at a critical crossroads. This benchmark index has been moving narrowly sideways for four months. Over the short term, since late January, there has been a clear downtrend of lower highs and lower lows which keeps a downward bias for resolving this trading range.

Level | Interpretation |

|---|---|

6900+ | Confirmation of renewed bull market |

6700–6750 | Major four-month support |

6500s | Normal correction zone below the 200-day moving average |

6100s | Panic level resembling “Liberation Day tariff” fears (≈11–12% decline) |

Global Oil Flows Through the Strait of Hormuz

Metric | Value |

|---|---|

Oil transported daily | ~20 million barrels |

Share of global supply | ~20% |

Share of seaborne oil trade | ~25% |

Primary destination | Asia (~80%) |

Most of this oil ultimately flows to China, India, Japan, and South Korea, which together consume the majority of Hormuz exports.

Commodity Outlook

Should the conflict stabilize within several weeks—as the sharp decline in Iranian strikes suggests—the commodity trajectory may resemble this:

Oil

Short-term spike > $100 if Strait remains closed through March 13th.

Return toward $60–70 if tankers begin moving without attacks by late March – early April

Possible move into the $50s later this year if Middle East peace reigns and energy supply chains open

Ags

Sharp price pullback when Gulf shipping commerce resumes

Gold

Safe-haven rally during uncertainty along with strong Dollar

Consolidation in precious metals and Dollar once shipping lanes reopen

The Fulcrum

Investment markets and global economies now balance on a narrow hinge. Should the Strait of Hormuz remain closed for long, oil could surge above $100, inflation fears would return, and investors might stampede toward safety. But markets are forward-looking creatures. If the strait reopens quickly—whether through military success or unexpected diplomacy—the current anxiety could dissolve just as rapidly. Oil could retreat below $60 and equities could resume their advance toward new highs. Which path prevails will likely be determined by the quiet passage of a few oil tankers through twenty miles of contested water. Eventually this Bull market will resume.

From the ancient spice routes to the supertankers of modern industry, the Persian Gulf has long been a place where the ambitions of nations converge. Today the world is once again reminded that history sometimes compresses itself into geography—and that the distance between panic and prosperity can be measured in nautical miles, between a dire strait and calmer open waters.

Comments

Log in or sign up to join the conversation.