Earlier this month we explored how tungsten has entered its most bullish phase in two decades. Three weeks later, we’re following up because Japan’s tungsten supply has just collapsed. So much so that Samsung, SK Hynix, and TSMC have been formally notified that they no longer have access to the chemical that wires their advanced memory and AI chips.

Behind that immediate crisis sits an even deeper problem. That’s why Washington is committing billions to build a supply chain outside China, yet it is doing so against a relentless ticking timeline.

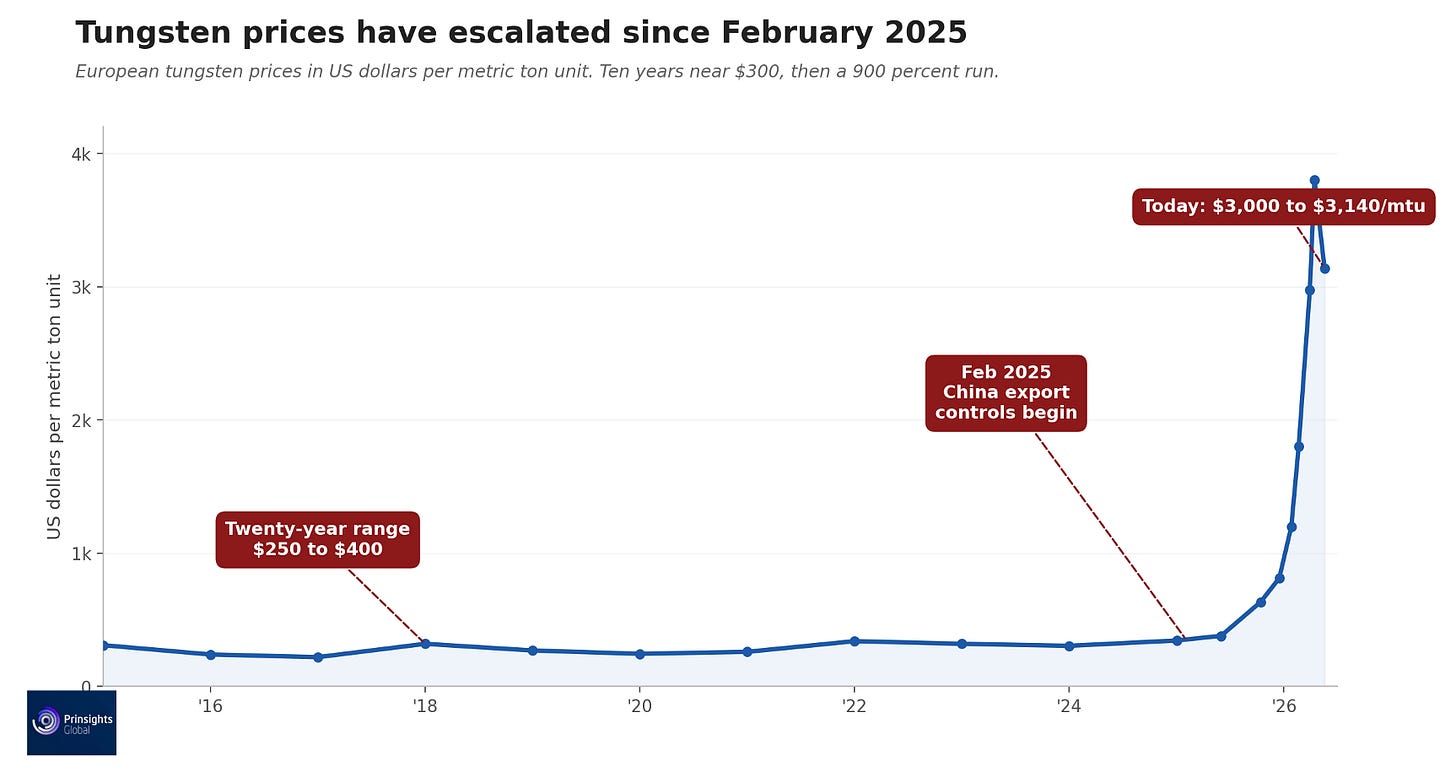

The issue is that the Rotterdam price for ammonium paratungstate (APT), the benchmark Western buyers use for tungsten outside China, now trades at nearly nine times what it was a year ago. Meanwhile, the United States has not commercially mined tungsten since 2015, when the last U.S. producer closed under competitive pressure from China’s cheaper supply chain.

What has changed since we laid out this growing tungsten problem at the start of June, is that Washington is putting serious money behind supply chain solutions that counter China. This, as the processing bottleneck is harder to solve than the mining gap.

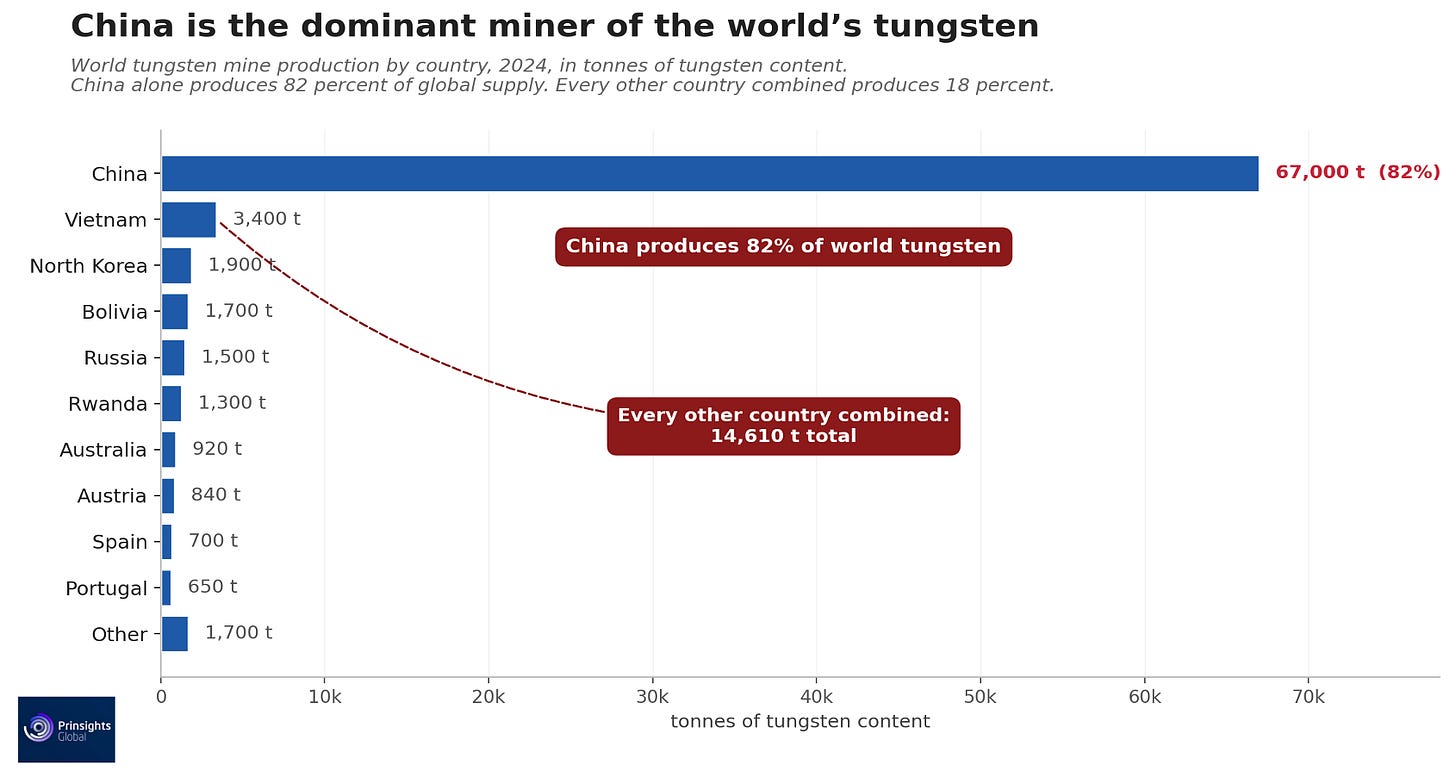

Compounding the issue is the dynamics of the Iran war, which has elevated the demand for more of the metal. The fact is that tungsten is required to build every missile, machine tool, and advanced chip, because it has the highest melting point of any metal featured on the periodic table. Basically, nothing else can match its role in armor-piercing rounds, drill bits or microchip interconnects. For a metal this essential to the tech world, the national security apparatus and the defense sector, the supply picture is alarmingly narrow. China mines about 80% of the world’s tungsten and holds 53% of global reserves, and it has spent the past year turning that dominance into geopolitical leverage.

China has narrowed its list of companies allowed to export tungsten to just 15 firms for 2026 and 2027. Meanwhile, Chinese exports of ammonium paratungstate, the intermediate chemical that nearly all tungsten products start from, fell 69% in 2025 to about zero in January and February of this year. China also barred tungsten exports to Japan for military and defense applications in January, after Japan had accounted for 57% of Chinese APT exports in the first eleven months of 2025.

The price has since skyrocketed because China tightened who could get supply. Chinese buyers have now gone as far as to start bidding up tungsten scrap in American yards, hunting for feedstock their own mines no longer supply.

The widening in the demand versus supply gap has been showing up in trade data. U.S. tungsten imports in December 2025 came primarily from Bolivia, Canada, and Vietnam, with China dropping out of its top three sources entirely. But even if the U.S. can source raw supply, accessing processing capacity offers a dynamic element to the situation that keeps the problem both complex and far from resolved.

The Main Choke Point Is China’s Processing

China refines more than 80% of the world’s tungsten, the step that turns mined concentrate into the ammonium paratungstate, powders, and carbides that industries actually buy.

So even when tungsten is mined outside China, most of the world’s processing capacity to get it across the finish line as a usable product sits inside China. That means a non-Chinese mine is only useful to a Western buyer if there is a non-China processor available to take the concentrate. That barely exists.

China has cut its first-batch mining quota for three consecutive years. Its 2025 quota was set at 58,000 tons of concentrate, which was down 4,000 tons from 2024. The result is a structural deficit that forecasters expect to last for much of the decade. Even if a new mine in the West broke ground today, no meaningful new supply would reach the market before 2030, and that assumes no project delays or disruptions.

Washington Is Now Committing Billions to Replace It

The clearest measure of how serious this quagmire has become is what the U.S. government has been willing to spend on it. In December 2024, the Pentagon put $15.8 million directly into the Mactung tungsten project in Canada’s Yukon. In late August 2025, the Defense Logistics Agency began testing the market for roughly 1,700 tonnes of tungsten ores and concentrates for the National Defense Stockpile.

By November, the Export-Import Bank of the United States (EXIM) together with the Development Finance Corporation followed up this move with $1.6 billion in Letters of Interest for a tungsten project in Kazakhstan.

At the start of this year, in February, the EXIM signaled another $240 million for a second Kazakh project on the condition that all of its output ships to the U.S. Washington is actively working to fund a tungsten supply chain from scratch, but any productive outcomes will take years to make a material dent in what’s needed.

Here’s where Iran complicates the matter. In the first weeks alone of the U.S. war operations against Iran, the U.S. military fired more than 850 Tomahawk cruise missiles, nine years’ worth of typical Navy procurement. It also used at least 40 Precision Strike Missiles, roughly 45% of the entire stockpile. Each Precision Strike Missile detonates above its target and disperses thousands of tungsten pellets. Tomahawk missiles use tungsten heavy alloy in the warhead technology. Patriot missiles and THAAD interceptors also use tungsten in the kinetic-kill vehicle. In an April 21 analysis, the Center for Strategic and International Studies concluded the Pentagon will need three or more years to rebuild Tomahawk, Patriot, and THAAD stockpiles to prewar levels.

Acknowledging the difficulty of the moment, on June 11, President Trump invoked the Defense Production Act and authorized the Secretary of War to address what he called “systemic constraints in the munitions industrial base,” the federal mechanism for fixing the gap CSIS identified. Every one of those rebuilt missiles will require tungsten.

Yet, that clock is legally ticking. Starting on January 1, 2027, the Pentagon won’t be legally able to source that tungsten from China across the upstream chain.

Chips are another factor making the squeeze worse. Japanese makers of tungsten-hexafluoride gas, the chemical that wires advanced memory and AI chips and about a quarter of global supply, warned of production risk after China cut off their tungsten powder, which leaves major chipmakers exposed.

Meanwhile, semiconductor-equipment sales are forecast to climb from $145 billion in 2026 to $156 billion in 2027, and ultrafine tungsten wire for slicing solar wafers has added thousands of tonnes of new annual demand. None of these applications has an easy substitute.

Tungsten cannot be mined quickly or processed at scale outside China. That rewards the few producers positioned outside China, especially those that can both mine and process. And while the price has slipped from its March high, our analysis shows that the lull is temporary and largely offers an opportunity.

Plus, there’s an additional looming factor on the horizon, driven by a July 13 Section 232 deadline, that could result in a bigger supply gap that the market has not priced in yet.

Comments

Log in or sign up to join the conversation.