Last week’s April 29 FOMC meeting saw the Federal Reserve hold rates at 3.5 to 3.75% for the third meeting in a row. The easing bias remained, leaving the door open to a rate cut whenever oil and inflation allow.

Ultimately, none of this changes the structural setup of costly debt. U.S. national debt crossed an epic $39 trillion in March. Net interest expense is now above $1 trillion annually. To put that into perspective, it has surpassed defense spending for the first time in modern history – typically the largest portion of the U.S. government’s spending.

Currently, the Fed balance sheet sits at $6.7 trillion. Its quantitative tightening (QT) program of selling bonds ended December 1, and the New York Fed has been buying roughly $40 billion a month in Treasury bills since December 12.

Foreign holders are holding 31% of U.S. public debt as of December 2025, down from a 2008 peak of 49%. The Fed is now absorbing the gap and has been steadily losing money on the payments it remits to the Treasury.

The Fed Held Because It Had to

As with all things Fed, the internal mechanics aren’t simplistic. Fed governor Stephen Miran wanted a quarter-point cut. Three regional Fed presidents, Hammack of Cleveland, Kashkari of Minneapolis, and Logan of Dallas, voted with the majority on keeping rates where they are but dissented on retaining the easing bias in the statement.

The committee leaned toward neutrality for interest rates, but the easing bias held. What that means is that the doves won the language by two votes.

Meanwhile, core PCE, the measure of U.S. inflation that tracks price changes in consumer goods and services, is running above the Fed’s 2% target. At the same time, Brent, a major metric of crude oil, is up roughly 50% since U.S. and Israeli strikes on Iran began February 28.

Yet, the Fed cannot afford a restrictive policy with $39 trillion in debt and over $1 trillion in interest expense, so the easing bias survives even when the data does not justify it. Every basis point matters now – and in the future. The stakes are not just high, but getting higher.

Fed funds futures removed essentially all 2026 cut expectations last Wednesday and the 10-year pushed to 4.41%. That indicates term premium for longer term debt rising, and not a market betting the Fed wins the inflation fight. For now.

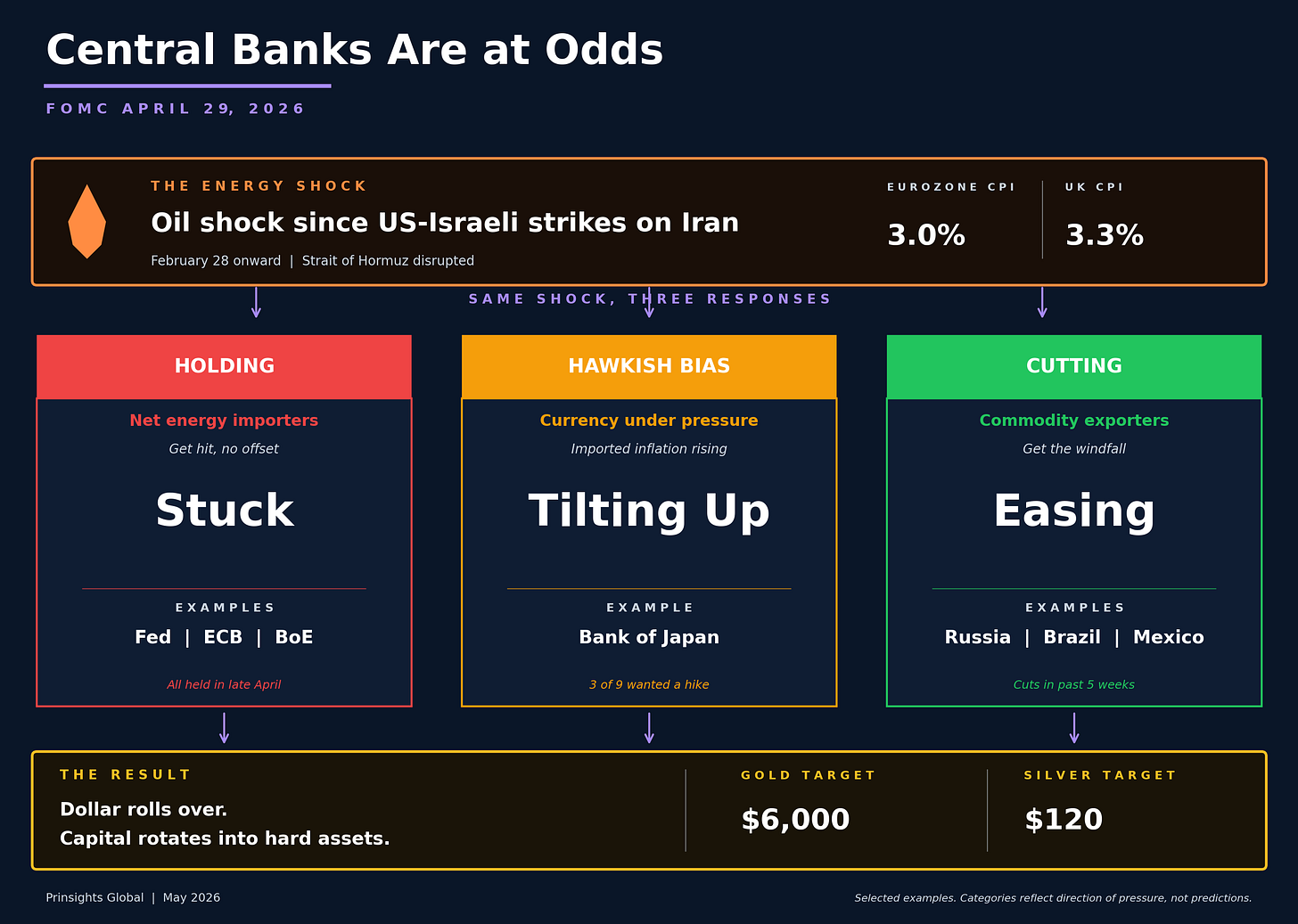

The Rest of the World Is Splitting Three Ways

The same debt-and-energy conundrum that’s constricting the Fed is playing out differently across the world. Six months ago every major central bank was cutting. Today, that synchronized cycle is over.

The dividing line now is whether a country imports or exports the commodities driving the inflation it faces.

The first group is stuck holding rates steady as oil feeds inflation. The Fed, the European Central Bank (ECB), and the Bank of England (BoE) now find themselves trapped.

The ECB and the BoE are massive net energy importers, so the oil shock hits as pure inflation with no offsetting export boost.

The U.S. is a marginal net oil exporter, but the debt math prevents real tightening. On April 30, the ECB held deposit rates at 2.0% with eurozone CPI, an economic datapoint that measures the average difference over time in prices paid by consumers for a range of goods and services, came in at 3.0%. The head of the ECB, Christine Lagarde said the council had debated hiking rates. Global markets are pricing three ECB rate hikes in 2026, and the first could arrive at the June 11 meeting.

The BoE also held rates steady at 3.75% in an 8-1 vote. The BoE’s Chief Economist, Huw Pill, was the lone dissenter, pushing for a hike to 4.0%, with UK CPI at 3.3% in March.

On the other side, the second group is leaning hawkish. The BoJ held at 0.75% on April 28 in a 6-3 vote, with three board members pushing for 1.0%. Japan is a net importer of most of its energy and food, with a weak yen making each import more expensive. The central bank raised its FY2026 core inflation forecast to 2.8% from 1.9%. With the yen past 159 to the dollar, the BoJ is the only major central bank with a clear hiking bias.

When we turn to the third group, we see they’re choosing to cut anyway. Commodity exporter nations are easing, while the importers are trapped by the same price spike. Russia, one of the largest global oil and gas exporters, cut rates by 50 basis points to 14.5% on April 24, the eighth consecutive cut. The central bank noted at its March 20 decision that the oil and gas price surge was supporting government revenues and tightening financial conditions less than expected.

Brazil, a net oil exporter and the world’s largest soybean exporter, took the Selic 25 basis points to 14.5% on April 29, second consecutive cut, unanimous vote, into 4.9% inflation expectations for 2026 versus a 3% target. Mexico, also a net oil exporter, cut to 6.75% on March 26 in a contested split vote.

What This Means for Gold and Silver

Once the Iran-related situation subsides, the dollar will gradually weaken as those rate differentials compress. Gold and silver have dipped recently on Iran-driven headlines.

The question is what happens when central bank policy divergence forces capital back out of the dollar and into something that central banks are buying. This is where strategic investors should be focused.

Three developments are shaping the next round of central bank decisions in June. The developments are:

The World Gold Council confirmed continued central bank buying of gold in Q1.

The Fed is buying $40 billion a month in bills.

The BoJ has indicated a clear hiking bias, which means yen-funded carry trades would unwind into hard assets, not more dollars.

All of this favors gold and silver. Our 2026 targets remain $6,000 gold and $120 silver.

Comments

Log in or sign up to join the conversation.