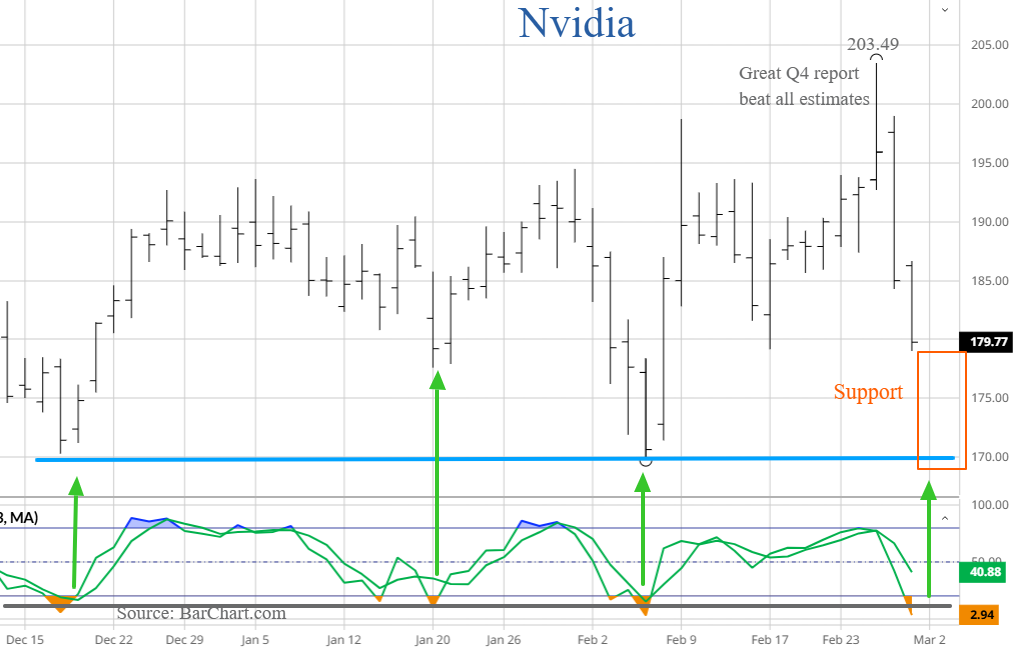

The market waited with bated breath for Nvidia (NVDA)’s fourth quarter earnings report – expectations inflated, speculation extravagant. The company delivered. Revenue, margins, data-center growth, and guidance all surpassed even the optimistic “whisper numbers.” For a fleeting moment, investors awarded Nvidia a valuation cresting near $5 trillion, north of $203 per share. And then—predictably—the stock fell roughly 12% from its post-report high. “Buy the rumor, sell the news,” goes the adage. But the selling was less about disappointment than digestion. In a market hypersensitive to capital intensity and duration risk, excellence has become an invitation to monetize gains.

NVDA may be another example of throwing the baby out with the bathwater. It did not matter how amazing the earnings, revenues, margins and guidance were for the Wall Street Fashion show. Many of the stocks being jettisoned recently are adopting AI to become more profitable, but that realization is for another day once valuation multiples have contracted to some mystic level reflecting a safer growth path.

Competition: Real, But Not Determinative

There are legitimate Nvidia challengers in the long run.

Advanced Micro Devices (AMD) continues to expand its AI GPU lineup.

Alphabet (GOOGL) (Google) designs TPUs for internal training workloads.

Amazon (AMZN) offers Trainium and Inferentia chips.

Microsoft (MSFT) is investing in custom silicon as well.

Competition in capitalism is evidence of opportunity. Yet investors occasionally mistake “more players” for “less demand.” Current hyperscaler capital expenditure plans for AI infrastructure are staggering— estimated in the $600–$700 billion cumulative range for 2026. Even assuming incremental silicon share shifts, aggregate compute demand continues to exceed supply.

The analogy is electrification. When Edison faced competitors, the market for electricity expanded. When railroads competed; commerce multiplied. Telecommunications saw price wars; bandwidth exploded. Infrastructure cycles are less about monopoly permanence than about total addressable growth.

The AI capital expenditure supercycle was initially net cash flow heavy, sending the hyperscalers and their suppliers soaring on a wave of profits. Investors have become understandably nervous that near term cash (liquidity) and profits (financial gain) are being sacrificed so much so as to warrant a greater risk premium and thus lower valuation multiples. NVDA had a Price to Earnings multiple of 139 in April 2023. It was about 50 in 2024 and 2025, but only a 23 to 25 PE multiple on Forward expected earnings in 2026. Until there is a major earthquake in this AI buildout, it’s hard to imagine NVDA correcting too deeply given their 65% sales growth and consistent 75% profit margin.

The hyperscalers’ cap-ex ambitions remain extraordinary. The pessimists fixate on “cash burn.” The optimists note that data centers are to this decade what rail hubs were to 1880 or fiber-optic backbones to 1999. They were expensive before becoming indispensable. There will be major corrections along the way, but the AI genie is not going back into the bottle.

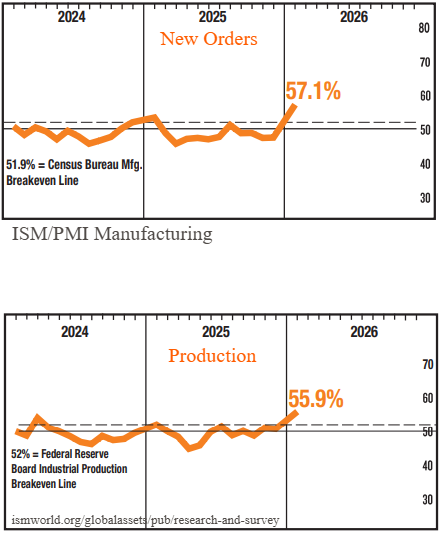

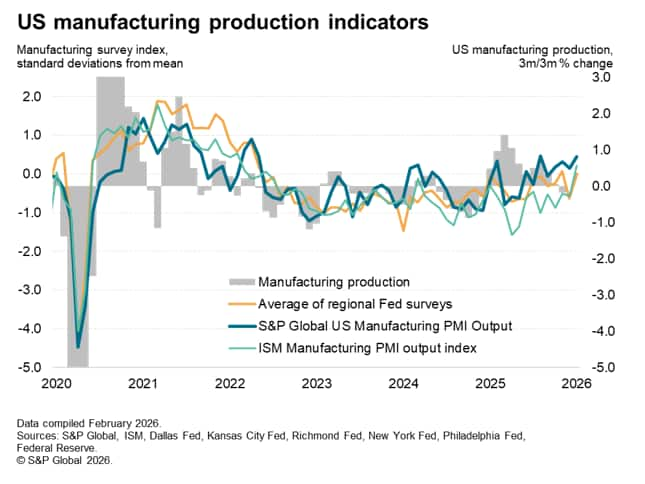

While the financial press obsesses over GPU and TPU, quieter data are improving:

ISM manufacturing PMI recently moved back into expansionary territory.

New factory orders have accelerated.

Industrial production has firmed.

Wage growth remains ahead of inflation in real terms.

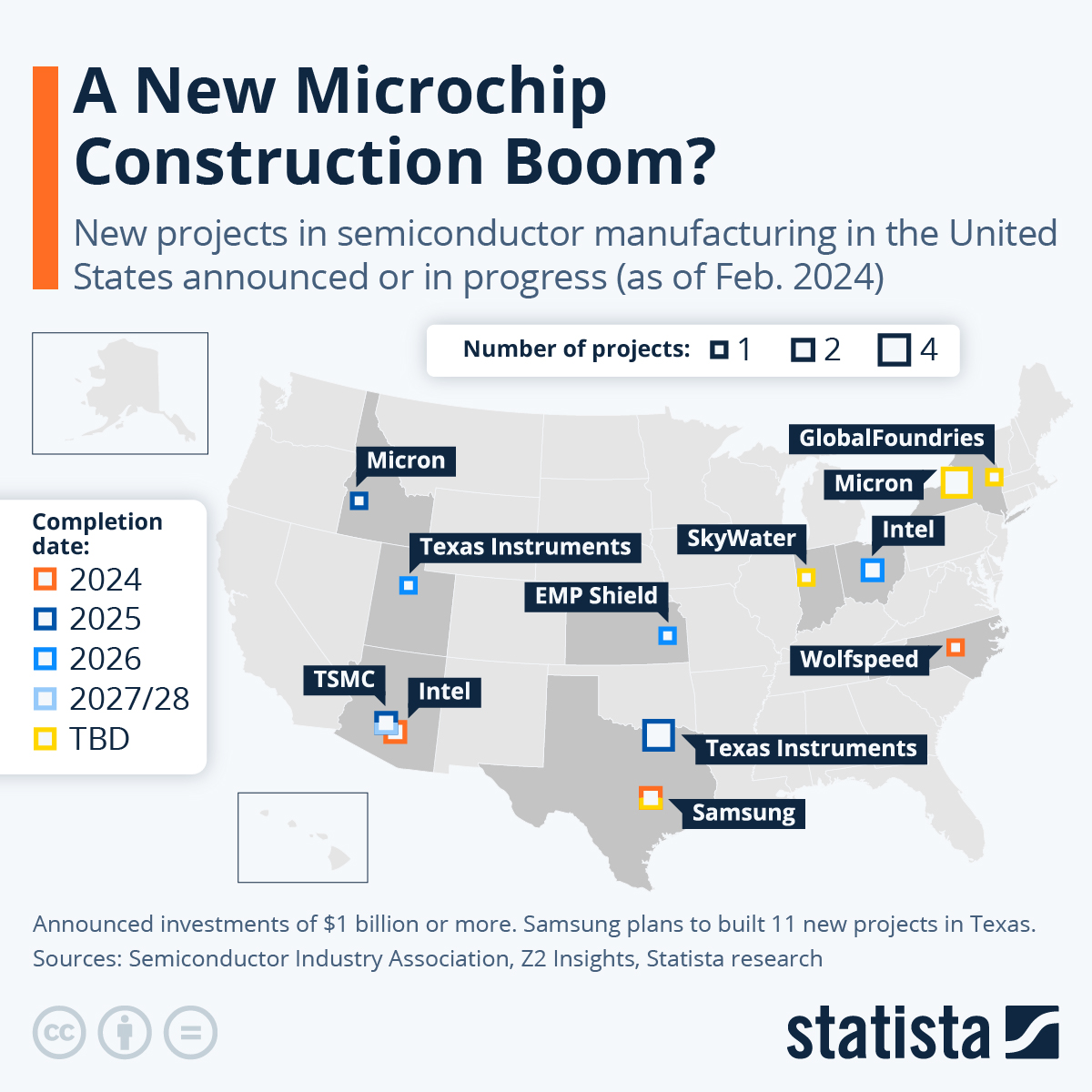

The U.S. economy continues to grow above trend. Household net worth remains elevated. Employment is sturdy. Manufacturing reshoring—semiconductors, energy infrastructure, heavy equipment—adds ballast to what critics describe as a “purely digital bubble.”

Consider complementary beneficiaries:

Corning (GLW) supplies optical connectivity essential for AI data centers – glass for cell phones.

Eaton Corporation (ETN) provides electrical systems for power-dense facilities.

Vertiv Holdings (VRT) builds thermal and power management systems.

GE Vernova (GEV) provides power generation for data centers – sold out capacity through 2028.

Caterpillar (CAT) benefits from infrastructure expansion.

Freeport-McMoRan (FCX) gains from copper demand.

These firms are not speculative app developers vulnerable to AI. They pour concrete, forge copper, cool servers, provide energy and connect fiber.

Markets do not advance in straight lines; they lurch between euphoria and prudent uncertainty. Recently, investors have been quick to punish any company perceived as vulnerable to AI disruption—or overly aggressive in financing distant growth. Multiples contract first; fundamentals adjust later.

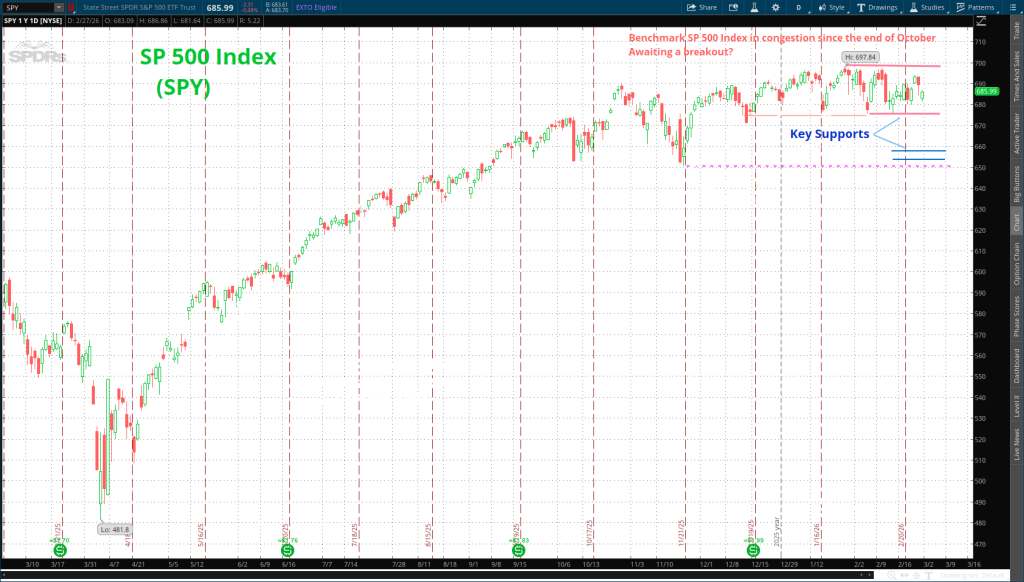

We expect the current valuation reset to precede a renewed advance. The MAG 7 hyperscaler stocks have been in a sideways correction for about 4 months with declining multiples. If early-year volatility produces a more disciplined earnings multiple environment – lower stock prices, the runway for the second half expands.

Even trade tensions and regulatory noise—credit card rate caps, institutional housing scrutiny, tariff disputes—introduce uncertainty but not paralysis. We anticipate that many of the policy clouds will disperse well before the midterms in November.

The Great Rotation: small- and mid-cap value sectors have aggressively led in recent months as the mega cap tech stocks have stalled. Leadership broadening is not a sign of weakness. It is the democratisation of capital redistributing momentum. While mega-cap consolidates, industrials, financials, healthcare, and materials have gained relative strength.

In prior cycles, when leadership narrowed excessively, subsequent expansions required rotation before renewal. The 1990s saw tech rise, falter, regroup. The 2003–2007 expansion broadened beyond early cyclicals. The post-GFC era saw FAANG dominance before industrial and value resurgence.

The Nvidia episode is not the unraveling of the AI thesis; it is the normal cleansing of excess enthusiasm. If volatility persists or panic manifests near term it may serve as the precondition for a broader advance. As AI capital expenditure moderates toward sustainable cash flow later in 2026, leverage concerns should ease. As policy uncertainty clears, multiples may expand again.

The second half of the year may witness synchronized participation—mega-caps stabilizing, small-caps ascending, cyclicals strengthening. Earnings are growing, production is expanding, and capital is being deployed, which provides a lenghty tailwind to this enduring Bull market.

Comments

Log in or sign up to join the conversation.