Photo by D O M I N I K J P W on Unsplash

Market Analysis

Last week’s 2022 US planting intentions provided some surprises when the survey revealed higher corn plantings, unchanged in soybeans seedings & even higher winter wheat plantings than the trade expected. The USDA won’t utilize these planting levels until their May 12 first 2023/24 US supply/demand update. Their importance however justifies 2023/24 balance sheet creations utilizing Ag Forum trends. The latest quarterly stocks, S America’s crop prospects, the Black Sea conflict’s impact on world trade & US spring planting weather will all be factors influencing the upcoming April 10 US old-crop balance sheets.

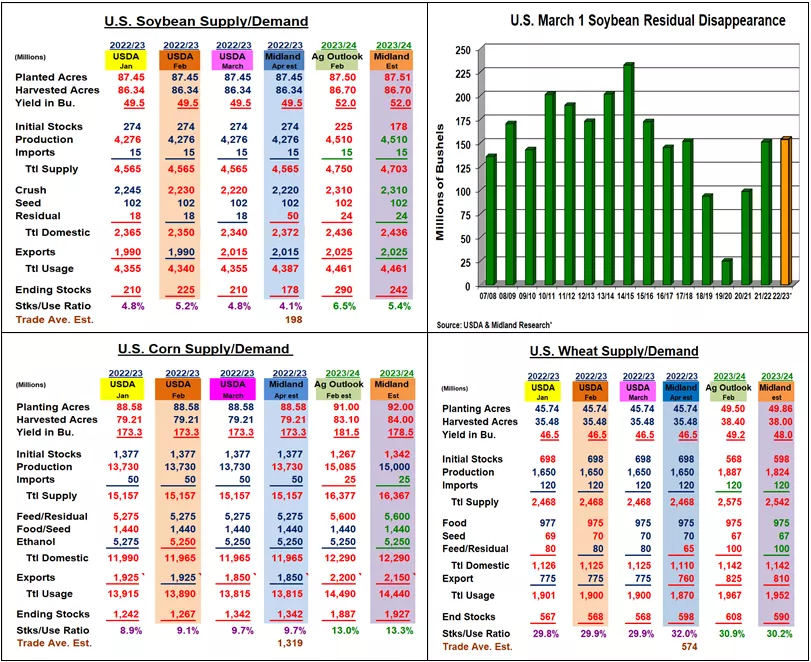

Soybean’s March 1 stocks were 57 million bu below the trade’s estimate. February’s 25 million stronger US crush & Census export data helped explain part of this difference. Given Argentina’s poor crop & recent US hog & poultry reports, the current US export & crush trends seem on target. However, the current 154 million residual disappearances suggest the US crop could be overestimated by 30-35 million bu or possibly more. This suggests beans' residual demand should be 50 million bu to reflect a 2023/34 ending stocks below 180 million. Will the USDA do this change now or wait until later? A smaller carryover tightens up the soybeans 2023/24 balance sheet without any change in plantings.

Corn’s quarterly stocks were also 70 million below expectations. A higher Feb US export pace (+29 million) than inspection data & China’s hefty 4 mmt of purchases should keep exports unchanged. Feedlot cattle numbers are down, but hog & poultry figures are near last year. With limited alternate feedstocks (wheat & small grains), corn remains the # 1 feed source. With higher spring & summer driving, ethanol should have a strong 2nd half-corn demand. Corn’s 92 million seedlings are sizable, but 1.3 million of these added acres are in the N Plains under snow keeping us nervous.

Wheat’s higher quarterly stocks suggest 10-15 miln lower feed usage. Slow exports also suggest a 15 million rise in stocks to 598 million. US wheat seedings are large, but 2023’s Plains drought could cut harvested area sharply.

What’s Ahead:

Higher corn and wheat planting intentions seemed to counter soybeans and corn’s lower-than-expected March quarterly stocks. However, current ground conditions aren’t favorable in either N or SW Plains for spring crops to be planted (snow) or winter crops to be harvested (drought). How S America’s crops finish is also important. Hold corn & soybeans sales at 80% & new-crop marketings at 10-15%.

More By This Author:

US Planting Intentions/Q-STKS

Reaction To USDA's March 2023 Prospective Plantings And Grain Stocks

Strong Ag Prices Could Return Total US Plantings To Recent Levels

Comments

Log in or sign up to join the conversation.