Is the US economy collapsing into the Epocalypse that I predicted would start to show up as large cracks in the economy last summer? The initial damage that I forecast for last summer was in auto sales, housing sales, and the ruin of retail stores and shopping malls along with their satellite restaurants. These initial breakups, I said, would likely also include a stock market crash a little later … likely by January 2018, or, in the very least, by this summer.

Those things that I set out for last summer did begin to materialize on schedule, but autos and homes got a big temporary lift from the hurricanes and wild fires that destroyed hundreds of thousands of each. I also predicted that reprieve as soon as those events took place. I didn’t wait until after the fact as a justification of the change but stated it before any statistics showed the reprieve was happening and before other economists came out saying such a reprieve would happen (though many economists now concur). You can find all of that in last year’s articles. I also indicated then how long that temporary reprieve would last — to the start of this year for autos and probably until late summer for housing. (I’ll come back to those in my next article.)

Fed up with the Fed

In this article, I want to lay out the tidal change in stocks and bonds that is happening exactly on the slower schedule for decline that I gave for those markets. That, by the way, was a prediction that should have been easy for any economist. It is to the utter shame of nearly all economists and stock and bond gurus that the shift that is now appearing everywhere was not in their forecasts. It is even more to their shame that so many still cannot see what is happening even as it now takes place right under them; but we’ve seen that specialized ineptitude in the past.

In fact, I started writing this blog because economists seem uniquely to be the solitary class of experts who understand the basics of their own field far less than anyone in any other field. To their monumental discredit, almost none of them saw the Great Recession coming. The worst of them all, however, was one who was highly regarded for his analysis of how the Great Recession’s predecessor, the Great Depression, came into being. This is the same man who, as the worst possible answer to the Great Recession, gave us the Great Repression of interest rates all over the globe, believing he could engineer our way out of a debt-caused problem by enticing everyone to a lot more debt.

It was just as easy during those recent years when all economists must have been on hallucinogens as it is now to recognize that a global crash of enormous magnitude was imminent. Nevertheless, two heads of our nation’s central bankers (one who was CEO of the central bank at that time and one who was about to be) stood knee-deep in the Great Recession and pronounced there was no recession anywhere in sight! That was one of the most bombastic claims ever made — given that it turned out to be one of the greatest recessions in US history — one that plagues us still. The same highly praised, overpaid economists who missed that one while standing in it are missing the present one, even as they create it.

Because of his astute understanding of the formation of great economic abysses, the younger one of the two (Ben Burn-the-banky) was handed the reins of our economic system by the other (Alan Greenspent). Why national government would readily approve handing the reins over to a blind man after the hindsight of his total blindness was a clear fact is something that would be utterly beyond me to comprehend, except that I readily affirm that is how government and crony systems routinely operate.

So, do not be surprised that none of our nation’s central banksters see what the fallout of their present actions, and do not take their misguided statements about the strength of the economy with any more seriousness than their august opinions deserved in 2008. You have to look to those with no economic training, such as myself (or just look to your own gut-level understanding) to find people who can see the obvious in the face of a multitude of professionals who deny the obvious and odious facts that already engulf us.

To that end, I am going to start this short series about the death throes of the Fed’s recovery by looking at the sea-change in stocks and bonds simply because this was the most self-evident pair of events I predicted, which many still argue with even as they are now standing ankle-deep in the problem’s formation. Most of all, I present it first because it is the area of economic destruction that is directly related to the Fed’s earlier interference in the economy and its new unwind from said interference.

Stocks in bondage

First, let’s look at the stock market. Here is where the stock market was going when I made my prediction last spring as well as where it went as soon as January, 2018, came and where it is headed still:

One-year Dow trends 2017-2018.

Pretty clear to see a complete change here in the market’s dynamics and its direction. which exactly matches what I predicted on this blog … even to what I gave as the mostly likely date for the change’s beginning. The stock market rally broke its long-term trend at the end of January. This timed out precisely with the Federal Reserve’s increase in quantitative tightening, which is what I said would break the market when January came in the first place. (The Fed did its January tightening in the final week of the month where the trend reverses almost symmetrically to the hyped enthusiasm of the year before.)

I had said that the US stock market could crash in the fall of 2017 when the Fed’s tightening was scheduled to begin, but that I expected the break to come in January because the Fed’s initial tightening in the fall would be fairly insignificant. That amount would double in January and start to become a significant factor working against the stock market.

I expected, then, that that end of the market’s glory days would not be recognized (or, at least, admitted) by many until this coming summer by which time the Fed’s unwind will begin happening at a furious pace, so that market troubles will be worse than they are now and the trend long enough that no one will be left to deny the change. So, I’ve said all along to anticipate a major drop in January with worse to come by summer. (That doesn’t mean the new down-trend will be a clean line. I have said to expect some reprieve — even in the trend — as that is how major crashes have played out in the past. Remember, for example, that April is typically a good month for stocks, whereas late May through October … not so much.)

The stock-market plunge that ran from the end of January into February included two of the largest point falls in the Dow’s long history, no insignificant event. In fact, it was one of the most rapid corrections from a record high in Dow history. More to its significance — now that we have a little time frame for assessing the damage — is that the market clearly has not recovered — evidence that this was a major market shift point; and there is certainly more of that to come because the amount of tightening is set to increase by another 50% at the end of this month, which I expect will increase the market’s volatility once again, exerting even more downward pressure.

The precise correspondence so far between the Fed’s unwind and the market’s troubles is similar to the market crash that I predicted would happen in 2014 when the Fed said it would stop quantitative easing. I said then that the market would break in October when QE stopped, and here is what happened:

While the market plunge that fall was great, it didn’t quite add up to what many would call a “crash,”as I had said would happen. That’s because the Fed continued a small amount of QE even after it said it would stop by reinvesting its profits in more government bonds and continuing to roll over all the bonds it held. What was extremely significant, however, was that the market clearly broke in a way that it did not recover from for an entire two years. I declared the bull market dead because I don’t think trading sideways and getting NOWHERE for two years can justly be called a “bull market.”

Even though technical definitions say a bull trend hasn’t died unless it is replaced by a bear trend; but I call sideways for two years more bearish than bullish. If you got out of the stock market entirely in the fall of 2014, you could have re-entered the market exactly where you jumped out two years later and missed nothing but a roller-coaster ride in between. That’s a dead bull. (Of course, some investors are great at trading the volatile ups and down and would do well in that secular bear market, but clearly it was a completely different market from the years of almost constant, guaranteed, and serenely smooth rises that preceded that period.)

The death of the bull began exactly with the official termination of QE and continued all the way to the Trump Rally, which finally changed the game again … but only in a final burst of irrational exuberance over a fantasy about the salvation tax cuts will bring. That was a completely new rally because it no longer had anything to do with the Fed, which was driving he Obama bull. It was built on the hopes, which I said were false at the time, that Trump’s tax cuts would deliver great gains for the market. Clearly those hopes have failed so far to materialize now that the tax cuts are the new reality and have had nearly a third of a year to show themselves true. While some short-term reprieve may yet come, those cuts are ultimately as self-defeating as the Fed’s own efforts to restore the nation by expanding debt (for that is exactly what the tax cuts are attempting to do, too — only this time by expanding government debt).

The Trump bull shows no signs of getting a second wind because the trend has now been down, down, down (for as many months as I just gave “downs”); and many new concerns like trade wars and military wars are stacking up against it. (All darts to the bull’s spine that I’ve said were certain to start accumulating.) Most of all, the Trump Tax Plan’s own expansion of our debt balloon guarantees self-anhilation because it will raise interest rates on our unsustainable national debt through natural market responses at the same time that the Fed is raising interest rates by decree and raising them by its unwind wherein it is getting OUT of government debt. It’s the perfect debt storm, which will build to a furious state of affairs by the end of this year.

Why it’s all so predictable (and therefore was avoidable from the start)

The importance of pointing out these predictions again is to demonstrate that the impact any major Fed change of course will have on the market is highly predictable. (End of QE, end of zero interest policy, beginning of QE unwind — I’ve said what would happen with exact timing for those events, and it has happened in substantial ways.)

Thus, when the Fed said it would start raising interest rates in 2015, and we went all the way to November without a raise, I said with complete confidence the Fed would raise rates at its December meeting because, if it didn’t, it would lose face and appear unable to do as its forward guidance had promised. That would make the Fed’s much vaunted “forward guidance” dubious to where people would start ignoring the guidance, making it useless to the Fed’s intention of steering markets. The Fed couldn’t risk that because its credibility is the only thing that stands behind its money and its influence.

Further, I said the market would respond by getting euphoric right after the first rate increase and leaping up the next couple of days. It would do that because the long-anticipated and highly feared date came and nothing bad would happen. Everyone would be ecstatic that the sky didn’t fall. That is exactly what happened.

I also said that following that brief updraft, reality would set in, and people would start to wonder what it means that the seemingly endless days of zero interest were gone — perhaps for good — as an underlying support to the market. The market would start to fall off in the remaining days of the year and then would go over a cliff as reality set in. And that’s exactly what the market did.

To be fair, I initially proclaimed the Epocalypse would begin then. Though the downturn did not turn out as bad as I thought it would, the timing was precise to the day for each gyration in the market, and the January jolt did turn out to be the largest January point-decline in Dow history, so it was no little thing.

Moreover (and of great interest) the recovery from that plunge coincided mysteriously with two emergency closed-door meetings of the Federal Reserve’s board of governors followed immediately by a rare closed-door session between the Fed head and the president and vice president of the United States. We still don’t know what any of that was about; but clearly something significant was in the process of breaking because the Fed almost never has closed emergency meetings of its own board called on short notice and then with the president and vice president. President Obama’s only public response about that emergency meeting with Janet Yellen was a vague, “We compared notes.”

Of course, they compared notes, but what the heck were the notes about? I think something much bigger broke economically (now tucked forever away in those black holes that are carved out by law as dark spaces in every Fed audit) exactly as I thought it would, requiring immediate Fed reaction and immediate presidential reaction. You don’t have two emergency board meetings and presidential summit over anything sub-catastrophic.

The timing between the Fed’s major course changes and major market responses has always been exact in correspondence. While one financial writer, Mike Shedlock, ripped me apart for stating these turns could be predicted, there is a simple reason each market transformation came with exactly the timing I predicted, regardless of Shedlock’s argument against me. (I’ve erred a little in estimating the depth of each impact, but never in the timing or the fact that there would be a significant major negative impact.)

Why is are these sea changes in the market predictable? For one simple reason that has nothing to do with market cycles or charts or even economic fundamentals: As the Fed itself acknowledged, the Fed has been “front-running the market” (their term) with their “forward guidance” that promised huge hits of new money “in order to create a wealth effect.” (That, too, is something I stated about the Fed’s intention long before they admitted it and while many denied the Fed had any such intent; but their intentions were obvious by the timing of their announcements and moves.)

The Fed’s foundational support is as infinite as the Fed wants it to be and is the only reason we have experienced the illusion of recovery from the Great Recession. Any paradigm shift in its actions is going to have a major impact. So, each time the Fed pulls one more major support out from under its fake recovery, the recovery takes another jog down. Now the Fed is slowly pulling out all remaining support (in fact, reversing all of it), so the market is going to go down, down, DOWN.

The restoration of the housing market is fake because it was built on the Fed’s abnormally low long-term interest rates. As mortgage rates are now rising in response to the Fed’s unwind, the housing market will unwind, too — meaning it will collapse again as it did in 2008. So will auto sales as auto loans become more expensive. In part, the collapse of the auto market is also happening because the industry pulled forward sales with all kinds of gimmicks that manufacturers cannot keep repeating. (The retail apocalypse, on the other hand, is its own set of problems, but will be exacerbated by now rising credit-card interest as the retail recovery wasbuilt only on cheap debt due to Fed policies, too.)

That has been the central theme of this blog from day one — that we are still in the Great Recession, that our recovery has been an illusion created by Fed magic that is ultimately unsustainable. Therefore, the crash back into that recession will happen when the Fed’s magic runs out and will be worse than the original crash of 2008.

Economic reality here is that we are still in the Great Recession and simply don’t know it because the belly of the Great Recession was propped up artificially by the Fed. As the last of the props are being removed, we’ll go back into the recession we created, and discover a depth far worse than our first plunge. That will require a huge new global response; but more on that when the time nears.

We have done nothing to correct the deep flaws in our debt-driven economy, and the time to pay the piper for all of our cheap and easy living is NOW as interest rates climb. Our debt collapse may be a slow-moving event, but the stock market will not handle it well (because rising interest pulls money out of stocks and because stock buybacks, which helped drive the market up, were funded on debt that can no longer be supported when interest rises). Its an event the auto market (already flailing) cannot handle either, and certainly an event the housing market (completely dependent on the replay we had of super-low interest and relaxed terms in the early 2000’s) cannot handle. Ultimately (and most importantly), it is an event the US government (now desperately addicted to massive debt financing) cannot handle.

A lot of really big stuff is going to come down as interest rises from the triple forces of Fed rate hikes, Fed quantitative tightening, and rapidly expanding demand by the government for new creditors.

Stock market annihilation

The stock market’s inability to handle the present moves by the Fed and the expansion of government debt spending can particularly be seen in the ineffectiveness now of stock buybacks. I predicted last year that the repatriated money under the Trump Tax Plan would flood into buybacks far more than into capital investments. In complete proof of that, buybacks have now soared to levels even greater than seen in all the rest of the recovery period. If they stay on track with the record level of announcements year-to-date, stock buybacks will hit an insane trillion dollars by the end of the year.

Since the GOP tax bill passed … corporations have announced more than $225 billion in stock buybacks, overwhelmingly benefiting corporate executives and wealthy shareholders, and leaving the middle class behind. Corporate boards—often at the urging of activist investors—now spend an inordinate amount of their profits buying back their own stock and issuing dividends, leaving minimal resources for long-term investments in workers, training and innovation….

Across the country, there is a growing trend of big corporations using massive, permanent tax breaks for stock buybacks – choosing to reward wealthy CEOs instead of the workers who create profit and grow the company. In 2017, Wisconsin workers helped create $3.3 billion in operating profit at Kimberly-Clark. The company spent $911 million on stock buybacks last year and in December, Congress passed and President Trump signed a permanent, corporate tax cut for companies like Kimberly-Clark. Now, Kimberly-Clark announced that it will spend even more on stock buybacks this year. At the same time, the company announced that it would close two Wisconsin manufacturing facilities in the Fox Valley that employ 610 workers….

Stock buybacks are a “boondoggle” for the American economy and a practice that for much of the nation’s history was, in fact, prohibited. (Common Dreams)

And it still should be prohibited (one of the numerous needed corrections for real recovery that never happened as CEOs use the practice to enrich themselves at the expense of the company’s long-term success and at the expense of workers who suffer because the company goes downhill, as did Kimberly-Clark, as did Walmart after announcing buybacks and them closing Sam’s Club and laying off workers).

How can anyone think the Trump Tax Plan will create a platform for longterm economic growth when very little of the money is being spent on capital improvements, worker training/development, or research and development?

I’ve stated repeatedly on this blog that, if the Republicans were genuinely interested in seeing tax savings from repatriated profits employed to better the condition of the middle class via research and development, investing new capital in American factories, improved wages, etc. … they would have put such provisions in the new tax code. (More on the proofs of that failure in a future article.) They wouldn’t have to tell companies what to do, but would have mandated that companies deriving these new tax benefits not spend any money this year or next on once-prohibited stock buybacks. Better yet, as part of passage, they would have outlawed buybacks altogether, as they once were.

The buybacks were completely predictable because we have years of Great Recession history to know where the money is flowing. What I wish to point out here with this note about buybacks is that even with more than a quarter-trillion dollars in buybacks already announced for 2018 — a much higher buyback rate than in previous years — the stock market is still falling. Even with all the other new corporate tax advantages front loaded into 2018, the stock market is still falling. So great is the downdraft from the Fed’s unwind, which is still in its infancy stage.

In fact, at the end of March…

market technicians [warned] that major indexes are on the verge of a full-fledged, technical breakdown. “The extent of the deterioration in equities is very much a concern given the combination of near-term technical damage, along with the decline in longer-term momentum after having reached record overbought conditions into late January,” wrote Mark Newton, technical analyst at Newton Advisors. (MarketWatch)

U.S. equity benchmarks finished lower for a second straight session on Wednesday as a withering decline among last year’s most-prominent stock performers helped to unsettle Wall Street sentiment. (MarketWatch)

It’s been referred to as the “Tech Wreck” in which the FAANG stocks that carried the market up in past years during periods when other stocks were mostly falling are now falling the worst.

Fund managers have begun to ditch so-called FANG stocks that powered the U.S. stock market to record highs in January and are slowly rotating into commodity-related shares and other value stocks which typically outperform in late-cycle recoveries…. On Tuesday, an index which tracks the FANG stocks along with six other mega-cap technology stocks tumbled 6.3 percent, the biggest decline since September 2014…. Each FANG company rose more than 33 percent last year, helping power the S&P 500 to a nearly 20-percent gain. Yet … “Rising volatility and changing market leadership are now pointing towards the possible conclusion that the stock market peaked in late January 2018,” said Douglas Kass, president of Seabreeze Capital Management. (Newsmax)

Even the FAANGs are falling out of the market … and Facebook has been unfriended. While there are many internal reasons they are faltering, buybacks and the Fed put kept them rocketing onward and ever upward during all prior times of internal troubles in the recovery period. Now buybacks aren’t working, and the Fed isn’t there to save them. Nothing was able to pull them all down in unison until … the Fed began unwinding its QE. Thus, even market analyst’s are changing to “late-cycle” thinking, meaning they see the end of the boom is near. In fact, it’s actually here.

Recently, almost every security in the U.S. stock market has seen big moves, and increasingly, they’re all moving in the same direction. Wall Street’s spikes in volatility have coincided with a return of high stock-to-stock correlation, which could mean a far more difficult environment for stock pickers, as security selection is seen as harder when all issues are moving in tandem, fluctuating on macroeconomic issues rather than being driven by company-specific factors. (MarketWatch)

We have just seen the most rapid shift back to high correlation between stock moves at any time other than in 1987 (the year of Black Monday), Stocks are now moving in greater correlation than they have since 1980, and their trend is downward. (Correlation had hit an all-time low in January and is already back to all-time highs … and all in a downward direction. That’s a landslide.)

Even Bank of America’s Chief Investment Strategist, Michael Hartnett, now says, “Cracks in the bull case are starting to emerge, with fund managers citing concerns over trade, stagflation and leverage.”

You’ve heard a lot about the long Trump Rally being nothing but a euphoric melt-up in the market here — the exact kind of irrationality that precedes a major crash. Michael Wilson, chief U.S. equity strategist at Morgan Stanley Institutional Securities, now agrees: “We think January was the top for sentiment, if not prices, for the year…. When we look at our internal data combined with industry flows and sentiment, we think there is a strong case that January was the melt-up, or at least the culmination of it.” According to these banks, it’s downhill from there.

All of that and more is why this time is going to be an economic apocalypse (the “Epocalypse”) and not just another recession. Even the massive new corporate tax revisions are not saving the stock market because the Fed has always been the biggest game in town, and its leaving town. We are now entering (in phases) a time of great revelation about the abject failures of Fed policy for bringing a sustainable recovery and about the folly of our debt-based economic foundations and the corruption of our financial system — all of which we left fully in place and in power. We did NOTHING to resolve the real problems that created the Great Recession. That’s why I say we are really still in it. It’s the same grave financial flaws that are creating the problems we are now starting to feel again as the last of artificial life support is pulled.

An ugly reality will reappear behind our matrix of self-deception exactly as the Fed magic finally dissolves. It is, in fact, reappearing now in the seismic shifts we are seeing the stock and bond markets.

Bonds in the stockade

I’ve also predicted all along that — simultaneous with this change in the stock market — a significant rise in long-term bond interest would come as soon as the Fed started unwinding its bond holdings. In fact, it would be a race to see which crashed first — the bond market or the stock market. I believed the rise in long-term bond interest would be fairly small in the fall and would build quickly as the Fed increased its rate of quantitative tightening. This should have been obvious to everyone, but there are still many who cannot see it even as it is happening (because they don’t want to, which is how denial works).

It is just basic logic and math: the Fed started down the path of quantitative easing by buying long-term government bonds specifically in hopes of lowering long-term interest. Clearly that plan worked, given that long-term interest never went as low as it did during the long period of QE that was intended to lower long-term interest. It should be obvious as the shine on Bernanke’s head then (and its hard to understand why it isn’t to some) that, if you reverse from quantitative easing to quantitative tightening, you are going to experience the reverse effect. (It amazes me how many investment gurus cannot see this even as it is happening.)

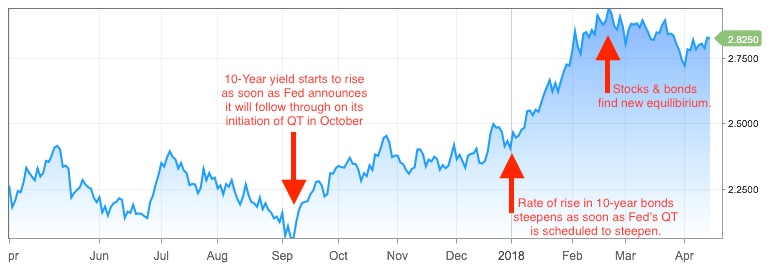

10-year bond interest rises in tandem with Fed moves.

You can see in the chart above that long-term bond interest began to rise subtly as soon as the Fed made a clear decision in September to follow through with its promise of quantitative tightening in October. The initial change in long-term bond interest was minimal during the fall months, but those interest rates rose drastically as soon as we moved into the month where the Fed’s unwind of QE was scheduled to double. Eventually, bonds achieved a new equilibrium with the stock market and interest settled on a new plateau, as could be expected. Here is how that math works:

The rise in interest rates was certain to happen because the number of bonds supplied to existing investors increased as soon the Fed began backing away from sopping up most of the government bond market. When the Fed doubled the speed at which it was backing out of the government bond market in January, the rate of rise in interest actually more than doubled.

However, when bond interest rises, it attracts investors away from stocks and into bonds. This is the normal inverse relationship between bonds and stocks that has been long-dormant under the Fed’s QE program; but now we are moving back toward reality. As a result, the demand for bonds rises to meet supply, so interest no longer has to rise to attract more buyers. Thus, by late February, bond interest had become high enough to attract enough buyers (out of the stock market) for the increased supply of availablegovernment bonds. So, interest settled at a new higher level — market equilibrium.

Obviously, now that the long-dormant dynamics of supply-and-demand are moving back into play, the Fed’s next roll-back in the amount of government bonds that it buys will increase available supply again. That will require, yet again, the enticement of more investors, which will force the government to offer higher interest to attract a larger pool of investors.

Many of those new bond investors will move money out of stocks in the normal historic pattern. Interest will hit a new level that sufficiently attracts a number of investors that matches the number of available government bonds. Then stocks and bonds as competing investments will find a new equilibrium again until the next interest increase.

It is simply the reverse of what the Fed was doing with quantitative easing in the first place. So, this is not hard to predict, and I don’t know why writers like Mish Shedlock miss it, except that they seem to see only how bond interest goes up when inflation goes up, and they don’t believe inflation will rise.

Many like Shedlock focus on inflation as the factor that determines bond interest. While bonds do have to track with inflation, because it erodes the long-term gains that long-term bond holders expect, bond prices (and as a result bond yields) are governed as much by supply and demand as by inflation. Greek government bonds, for example, have in the past gone up much more due to a growing supply in the face of demand that was rapidly retreating due to fear. To maintain demand, the Greek government had to hugely increase the yield on its bonds (reduce the acquisition price to investors).

Step by step, the restored market dynamic you see now between stocks and bonds is mathematically guaranteed to jack the government up into a situation of peril because the government astronomically increased its debt at a time when interest rates were pinned to the floor by the Fed. As a result, the US government has taken on way more debt than it can actually afford when interest rates normalize.

It is for all these reasons a given that the Fed’s unwind unwinds the whole “recovery.” I have maintained for years that will happen as soon as the Fed’s artificial life-support ends for a patient that actually died during the Great Recession. (It is astounding to me that the Fed is blind enough not to see that the same financial math they applied one way accomplishes a complete reversal of effect when applied the other way.)

Bond interest will rise in stages as the Fed forces the government to find additional buyers for its bonds in stages. Even interest on the government’s short-term debt rose by February to the highest level seen in nine years, which takes us back to the official period of the Great Recession.

This debt problem can easily be played and exacerbated by entities like China, which is the largest foreign buyer of US debt ($1.17 trillion in January), if it, too, decides to back away from buying government bonds — a possibility that China’s ambassador would not rule out when faced with Trump’s first tariffs. When asked about that exact possible retaliation, he replied only, “we are looking at all options.” With extreme deficits rising rapidly in the US as tax cuts fail to pay for themselves and as Republicans ramp up spending, the US can ill afford to have China, which holds about a fifth of the total US debt, back away from buying US debt.

China has two reasons to do stop buying US bonds. One is quite basic: reduced trade under the new tariffs will mean it needs to keep a lower balance of trade dollars and has fewer sales in US dollars to try to bank in US bonds. The other depends on how badly China wants to retaliate and pressure the US. They can back away just to bring economic harm to the US government, but there they will also economic harm to themselves if they go beyond what their lower trade balances mandate.

Regardless of what China does, the Fed’s unwind is sufficient to destroy its fake recovery. We are entering the day of reckoning that I have said throughout the writing of this blog would appear as soon as the Fed removes its artificial life support. Because the removal of the Fed’s resuscitation is happening in phases, the patient will grow increasingly pale in matching phases, but it is as inevitable as death by lack of oxygen.

The Epocalypse is arriving right on schedule

What remains a mystery is how far the Fed will go down this path before it realizes it is unable to unwind its QE without completely destroying its own recovery. Currently, the Fed’s targeted inflation has already risen above its goal of 2% annually. (CPI, the Fed’s yardstick, which understates real inflation, is now clocking in at 2.4% while other measures of inflation are over 3%.) With fuel prices poised to rise this summer, inflation on everything will go up even more because fuel factors into the price of everything.

That will make it extremely difficult for the Fed to retreat from its presently aggressive policy back to lower interest targets or to increase money supply (via low interest and more QE) because increased money supply will tend to push inflation up even more and because the Fed has always maintained that its financial policy is data dependendent (with inflation data and employment data being the primary data streams that concern it by congressional mandate).

It’s longtime claim is proven a lie if the Fed starts ignoring the data. How can the Fed justify easing financial policy again so long its own inflation data and job data show both are strong? It is pressed by its own duel government mandate (keeping inflation down and employment up) to, at least, wait until the job market is clearly deteriorating or until deflationary pressures have returned due to a clearly collapsing economy. By then, the downtrend will have a lot of momentum.

Failure of the recovery will make it clear the Fed’s recovery was always dependent on endless life-support. That means, when and if the Fed does return to zero-interest policy and QE, everyone will know it is now QE4-ever, creating serious credibility problems for anything the Fed attempts. And credibility is everything if the Fed is to retain belief in its money. That’s a whole new world of financial fear and uncertainty, and the markets don’t like either.

The alternative is that Trump gives the Fed governors a great war to blame their failure on or that their political allies get impeachment proceedings into motion as something to blame or that Trump’s trade war gives them something to blame. There are plenty of things coming that they will try to blame before they ever accept blame themselves.

I’ve said all along that Trump presents an easy scapegoat for their failure. He is a president who loves surprise and erratic moves, who feints left and leaps right, who seems inclined toward wider warfare (or toward risking it) and who admits his style of leadership thrives on conflict. All of that creates a shipload more of that uncertainty that markets don’t like. Plenty there for the Fed to throw blame on.

Regardless, it’s Epocalypse now, no matter who takes the blame, because the illusion of recovery is fading, soon to reveal the perilous chasm of debt over which our entire global economy is built.

When everyone starts scapegoating someone else … just keep in mind that all of this was completely foreseeable from the moment the steps of “recovery” began. Our politicians all failed to respond correctly as did all of our bankers, all of our regulators and most of our market advisors and certainly most economists. Instead of attacking corruption and greed, our politicians and head bankers bailed the greediest of them all out — even made them richer and all the more too-big-to fail. They solved none of those problems and have failed to regulate their greed by barring the worst activities of bank involvement in markets that created the Great Recession in the first place.

All of these failures have been laid out here at every turn, and the ways in which it will fall apart have been predicted here many times so that when it all falls apart, you can turn here and say, “No, look this could be seen coming by anyone that wasn’t in denial or blinded by some school of thought (be it Keynesian or Republican trickle-down economics).”

We are watching this economic collapse unfold with stocks and bonds right on schedule. The next set of troubles in the stock and bond markets should hit at the end of this month when the rate of unwind jumps up by 50%. Then things will get real serious in the summer when the rate jumps by another third. Then comes October with its usual Halloweenish spell on the stock market when. Their may be a great October surprise for some when we see what happens as the Fed’s unwind reaches terminal velocity in October.

If you think we’re going through all of that with no greater troubles than what we’ve seen, you’re not really thinking at all. That’s almost impossible.

In my next article, I’ll show how housing and auto sales are starting to widen again as cracks in the economy … exactly on schedule, too — how they started falling apart last year, why they got a predicted respite from that failure, and how they are now falling back on schedule. (All completely predictable because the housing market is entirely dependent on low interest.)