Why These 2 Stocks Can Be Unique Assets To Your Portfolio

Let’s face it.

Valuation is for dummies.

Just buy any of the hot tech stocks and you are set for life.

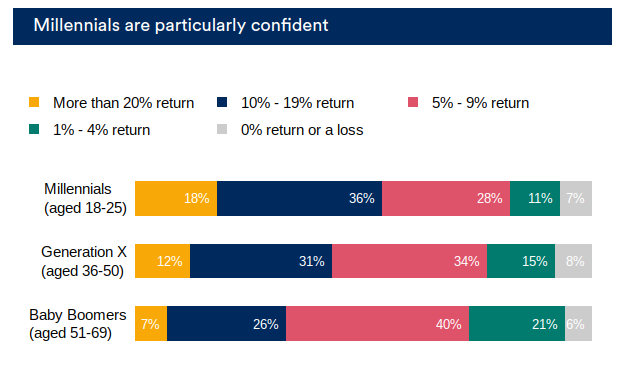

After all, millennials expect an average return of 12% over the next five years.

Who can blame them when all they have witnessed is this:

Source: ClearPath Capital Partners

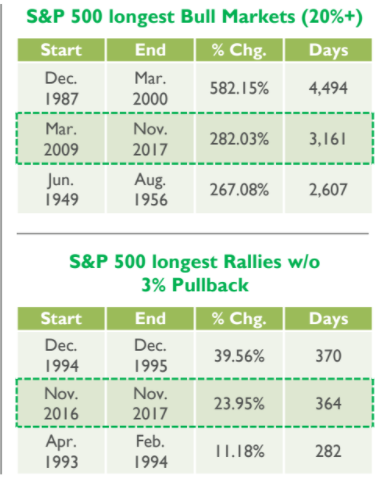

Use the rule of 72 and money will double in 6 years.

If you held a portfolio of Facebook, Amazon, Netflix and Google, you easily achieved it and more over the past 6 years.

Kidding aside, as we race towards 2018, in a market where valuation doesn’t get any credit, where millennials believe investing is as easy as apple pie, what do we older folks look for?

Cash is Always King

Call me outdated or old fashioned, but I love cash.

No company has complained or died from having too much cash or from growing their cash reserves.

One way I search for cash-rich companies isn’t to look at the cash on the balance sheet, but rather, the growth of Free Cash Flow combined with how management makes use of it.

Free Cash Flow growth is easy to find and calculate.

Most companies don’t provide the info, but the simple calculation is:

Free Cash Flow = Cash from Operations – Capital Expenditures

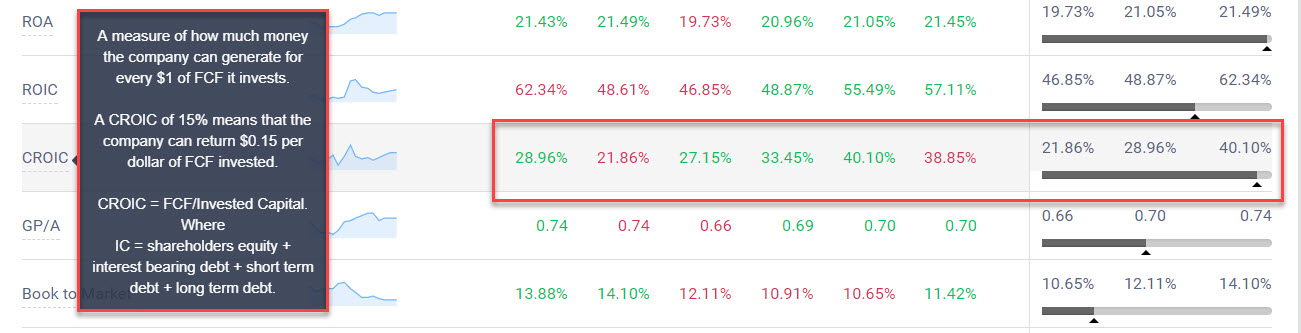

To measure management effectiveness, you can use ROIC, where

ROIC = Net Income/Invested Capital where invested capital usually comes out differently based on how you define it.

Source: old school value

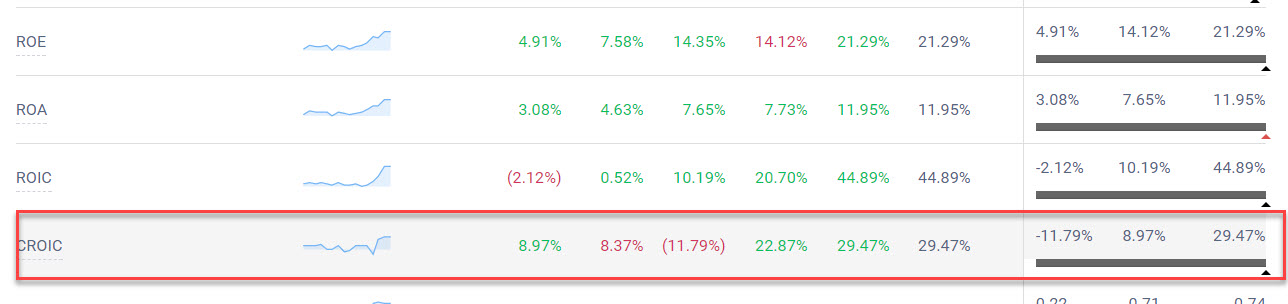

However, I like to take ROIC one step further and use CROIC.

Cash Return on Invested Capital

CROIC is the ROIC for cash. By looking at CROIC, you understand how management is making use of the cash and whether the money they are investing is profitable and increasing value to the business.

The CROIC formula I use is FCF/Invested Capital.

Rather than Net Income, use FCF and this measure gives you an understanding of how much money the company can generate for every $1 of FCF invested.

My FCF and CROIC Screener Details

Here’s what I’m looking for:

- FCF positive companies

- FCF CAGR over 3 and 5 years is positive

- CROIC is positive

- 3 year and 5 year CAGR CROIC is positive

This quickly eliminates companies that are losing money and companies where the leaders can’t manage and generate returns on their cash.

My goal is to focus my time and energy on a barrel full of fish I find appetizing.

With that, here are two stocks that are making money in this market with good fundamental cash growth.

Ross Stores (ROST)

Despite the economy riding on high consumer confidence, more retailers are going bust.

The retail apocalypse is real.

In a fiercely competitive market where margins are thin, Ross Stores has continued to defy trends.

I use a combination of Quality, Value and Growth factors to dig into a company.

But before I even get to those numbers:

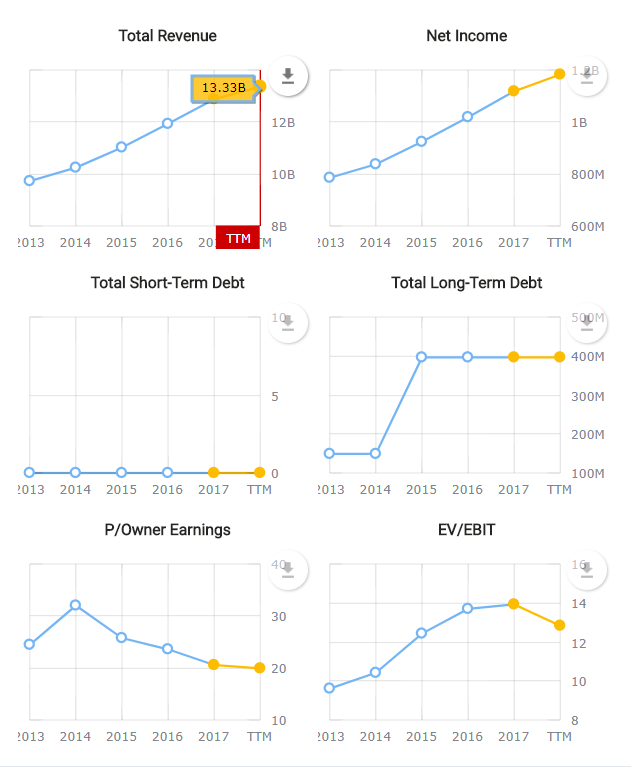

- revenue and net income has continued to increase

- no short-term debt

- long-term debt is easily manageable being 14% of total equity

- 3yr FCF CAGR = 38.8%

- 5yr FCF CAGR = 25.6%

- 3yr CROIC CAGR = 22.4%

- 5yr CROIC CAGR = 10.3%

What the last four points above show is that Ross Stores has been firing on all cylinders the past 3 years. The last 5 years were good, but the last 3 have been superb.

Whether it be a recession or a confident market, Ross Stores is outperforming.

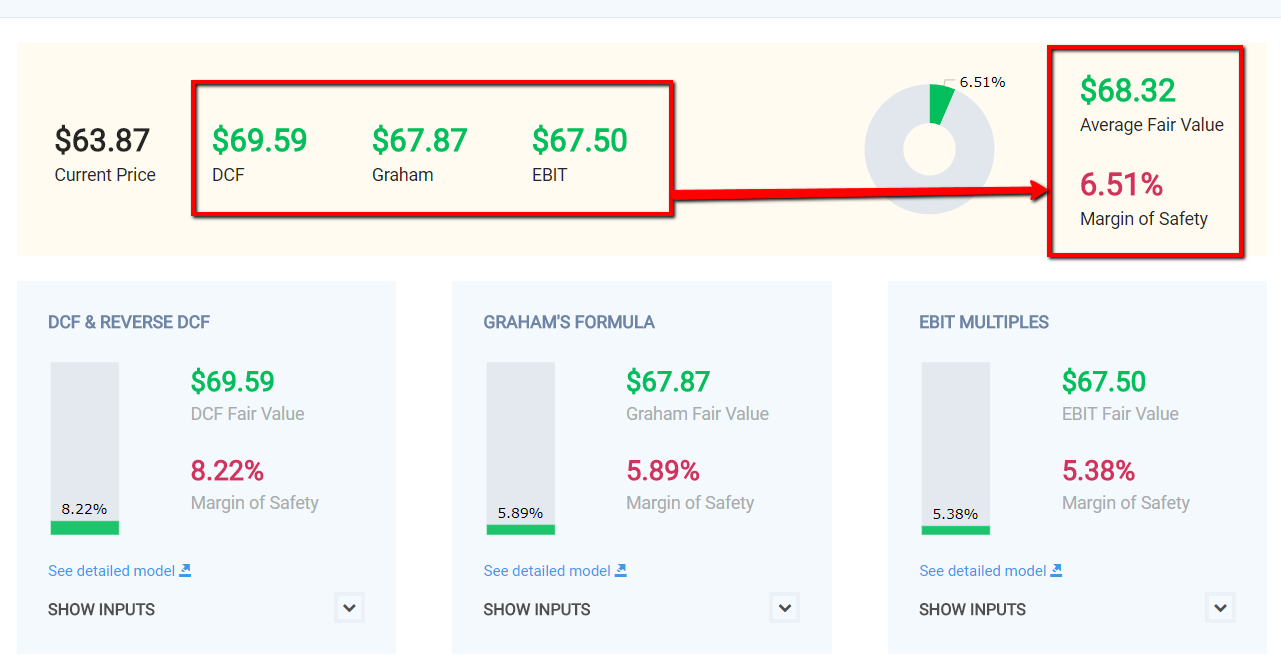

What’s more, a quick valuation shows that Ross Stores isn’t richly valued.

The PE is at 21, but the EV/EBIT multiple is at 13 and P/FCF is 20.

When I run my quick valuations to gauge what the market is expecting from Ross Stores, I come up with a range in the upper $60’s.

Source: old school value stock valuations

In a market where negative returns, negative FCF and negative CROIC is perfectly acceptable, Ross Stocks bucks this trend.

Just be prepared to be called senile if you hold Ross Stores.

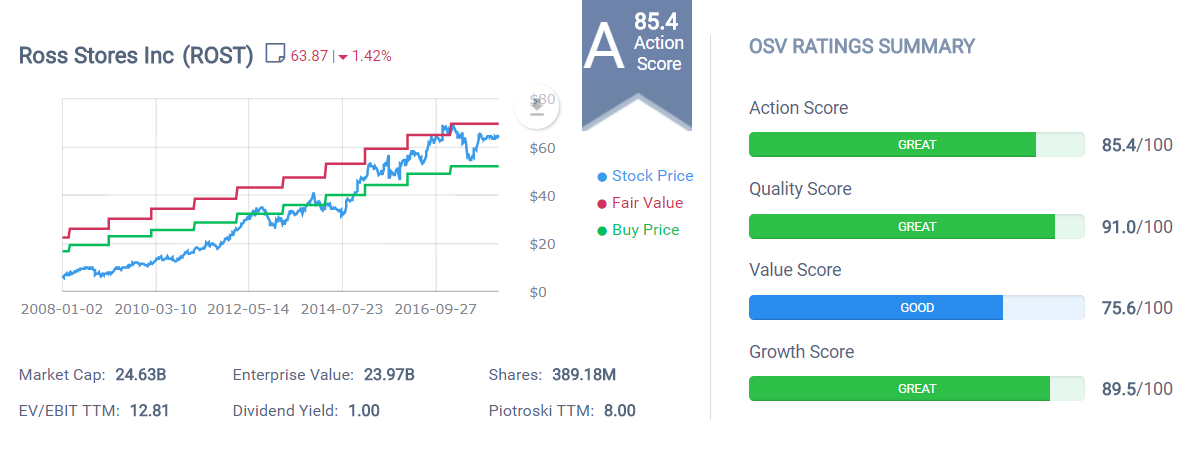

Here’s the summary snapshot.

Kimball International (KBAL)

Moving on from a discount retailer like Ross Stores is a small furniture company based in Jasper, Indiana.

They too have a list of impressive stats.

- P/FCF is 13

- EV/EBIT of 10.3

- 3yr FCF CAGR = 12.8%

- 5yr FCF CAGR = 10.6%

- 3yr CROIC CAGR = 28.9%

- 5yr CROIC CAGR = 52.1%

Coupled with very minimal short and long term debt and conservatively run balance sheet, Kimball is under the radar in this market where value is shunned.

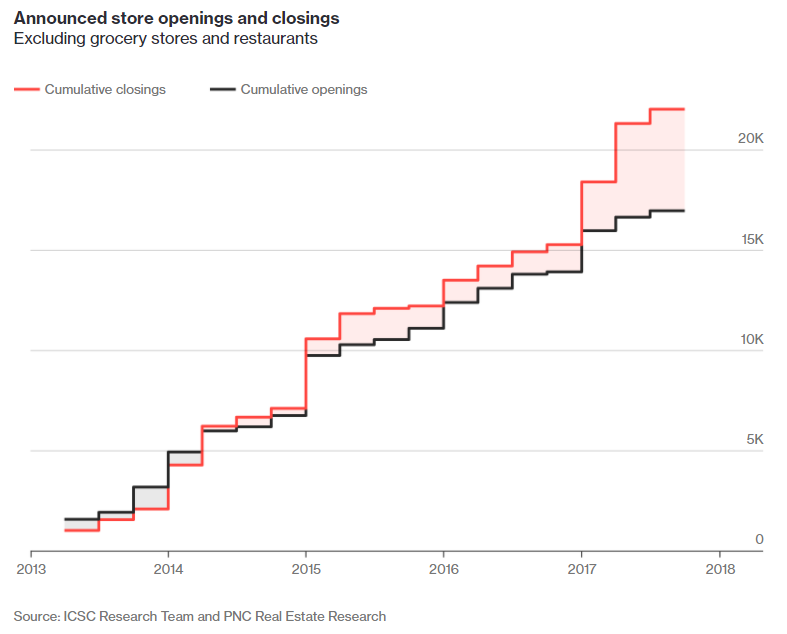

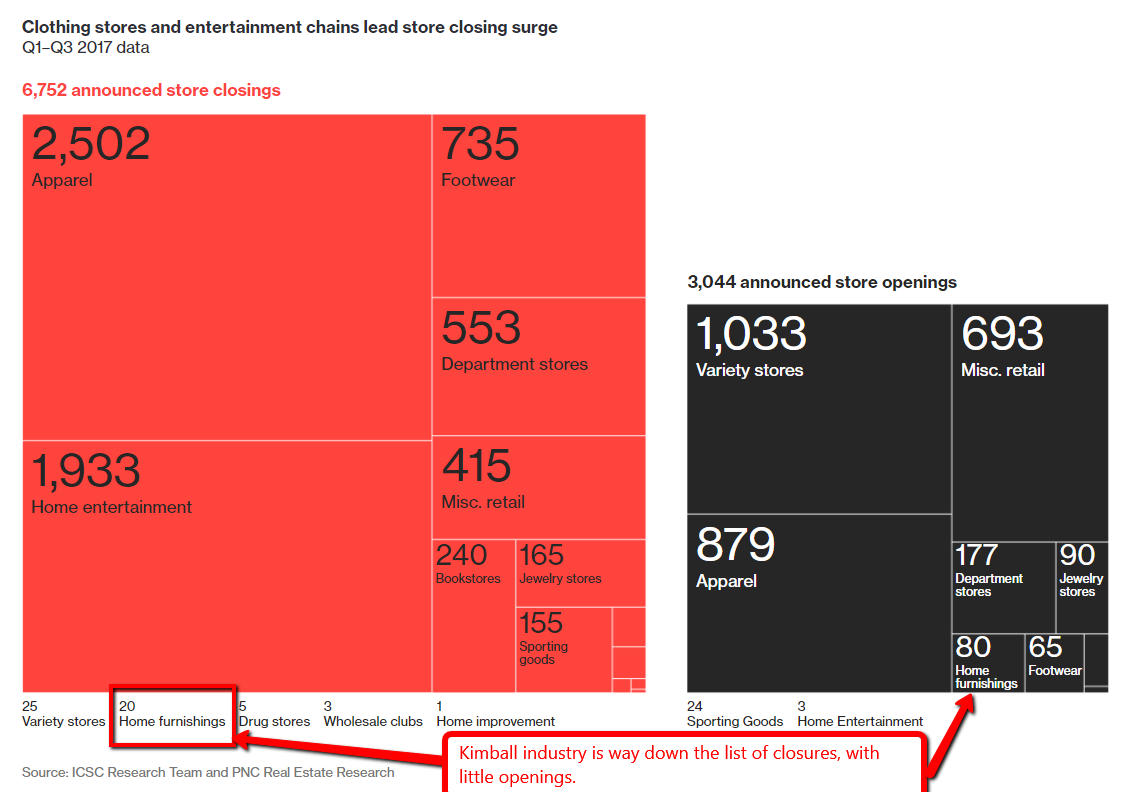

Take a look at this chart.

Apparel is at the top of retail closures with home furnishings way down the list.

Conversely, home furnishing stores are also at the bottom for new store openings.

The basic message I get from this chart is this.

1. it’s not easy to open a furniture store

2. not many want to open a furniture store

Where Kimball shines is that they are not a “home” furnishing company. Their main focus is on the commercial and government office and hospitality industry.

Their latest earnings slowed as it was up against one of their best comparable periods from last year, but earnings is the highest it has ever been and order backlog is at a healthy, although slightly down, balance of $122M.

When management of a furniture company mentions that their operating margins are going to increase with a return on capital exceeding 20%, that’s something to keep an eye on.

When management words also match how the company is performing, that’s a green light.

A couple of business accounting numbers that stood out for me is their cash conversion cycle and inventory turnover.

For the cash conversion cycle, it’s getting shorter. The shorter the better.

What’s most impressive is the surge in inventory turnover. Going from 3 inventory turns in 2013 to 11.7 in 4 years – astounding.

It sends the message that the business is improving efficiency, creating hit products and selling.

As Mark Cuban says, “sales cures all”.

Kimball is definitely worth a deeper look.

Summing Up

Ross Stores and Kimball International are two good examples of companies that are cash rich with growing cash.

That’s a win-win combination.

Regardless of how hot the market is, and how overvalued some companies are, these two companies are not expensive and cash will always be a major factor whether a business survives and grows or not.

Valuation may be considered old and boring to newer investors, but the price you pay is what counts.

Value investing may be out of favor at the moment, but companies like ROSS and KBAL should continue to shine many years into the future.

Disclosure: None.

Thanks for putting these on my radar. I had never heard of $KBAL and I had initially dismissed $ROST since I'm bearish on retail in general, but these stats are impressive.