There were some wild, unprecedented – frankly stunning – swings in some very large, high-profile stocks last week. The press concentrated on Meta, nee Facebook, and Amazon as the yin and yang, the negative and positive, of the market. Facebook (FB) (how long before Zuckerberg abandons Meta? I give it a year) managed to lose a quarter of a trillion dollars in market cap in the course of one trading day.

Image: Alhambra Investments

Zuckerberg lost a cool $25 billion or so himself. All because the company reported earnings that were less than expected – but revenue higher than expected – due to spending on the shift to a metaverse company. Never before had any company lost so much in such a short period of time. Of course, there have been precious few companies in history that could lose that much and still be worth over $600 billion so it isn’t that surprising, I guess. One of the big tech behemoths was bound to blow up at some point. Facebook did lose users for the first time ever (what took so long?) so there was news here but I think the real shock was the spending. I have no idea what they are building in the metaverse but it is most certainly expensive. Whether it will have any value is a different question and I don’t think anyone knows the answer to that one, including Mark Zuckerberg. But it does appear that he’s willing to bet a big chunk of the company to find out.

Amazon (AMZN), meanwhile, was down in sympathy after Facebook’s report although I’m not sure what actual connection there is between the two. Amazon hasn’t, to my knowledge anyway, subverted democracy for profit recently, so they’ve got that going for them. Admittedly, Bezos looks like a Bond villain and has a yacht to match (I’m not sure about the white Persian cat) so I can see why people don’t like the guy. But I don’t think he’s actually trying to take over the world or hold us all hostage with cheap goods and convenient delivery. But the downdraft in Amazon stock lasted all of a day until they reported their own earnings which just so happened to be a lot better than expected (shh, don’t mention that gain in Rivian stock that goosed the reported figure). One day after Facebook set a record for a one-day loss, Amazon set one for a one-day gain. Bezos reportedly bought a small country to celebrate.

What’s interesting to me is that of the two, Facebook is by far the cheaper stock. It trades for a lower price to cash flow, price to earnings (trailing and estimated), and price to book and has no debt. It generated nearly $13 billion in free cash flow in the quarter and $39 billion in the TTM. Amazon’s free cash flow is negative. It has higher returns on assets, equity, and invested capital. It has higher gross, operating, and net margins. In short, by the numbers, Facebook is the superior company and yet Amazon wins the beauty contest of the market. Benjamin Graham said that in the short term the market is a voting machine but in the long run it is a weighing machine (and the short term can be interminable if all you have is a scale). Facebook is losing the vote right now but Amazon has yet to be weighed.

What’s also interesting is that despite Amazon’s big day, the stock is still down for the year. Even more interesting is that it is no higher today than it was in July of 2020 – which is almost exactly the same situation for Facebook stock. And yet the popular perception is that Amazon is still a winner, a must-own stock, while Facebook is now on the downswing. The truth is somewhere in the middle, I suppose. Someday Amazon will have to generate cash flow and justify its multiple but that day isn’t today; the market hasn’t put it on the scale yet. Facebook, on the other hand, is embarking on a risky venture, betting a lot of capital on something no one understands or trusts. The weight of the metaverse – and a loss of users for the first time in its history – was too great and voters turned against them.

There are, however, a lot of companies being weighed by the market since the beginning of the year and I don’t think the dieting is over. It is true that a lot of the highflyers have come down a lot. It is also true that many of them – the ubiquitous EV makers, the SPACs, the meme stocks, the metaverse plays, fuel cells, payment processing, crypto assets, and development-stage biotechs – are still ridiculously expensive. And it isn’t just the very speculative assets that are getting hit. There are a lot of good companies out there with valuations that just aren’t supported by the fundamentals and they are being weighed. Clorox is a great company with a great brand name, a high stock price, and a lot of debt. Higher costs pulled down earnings and the stock was down almost 15% last week. Home Depot is a good company but the stock is down 13% YTD. I could go on but it is a long list.

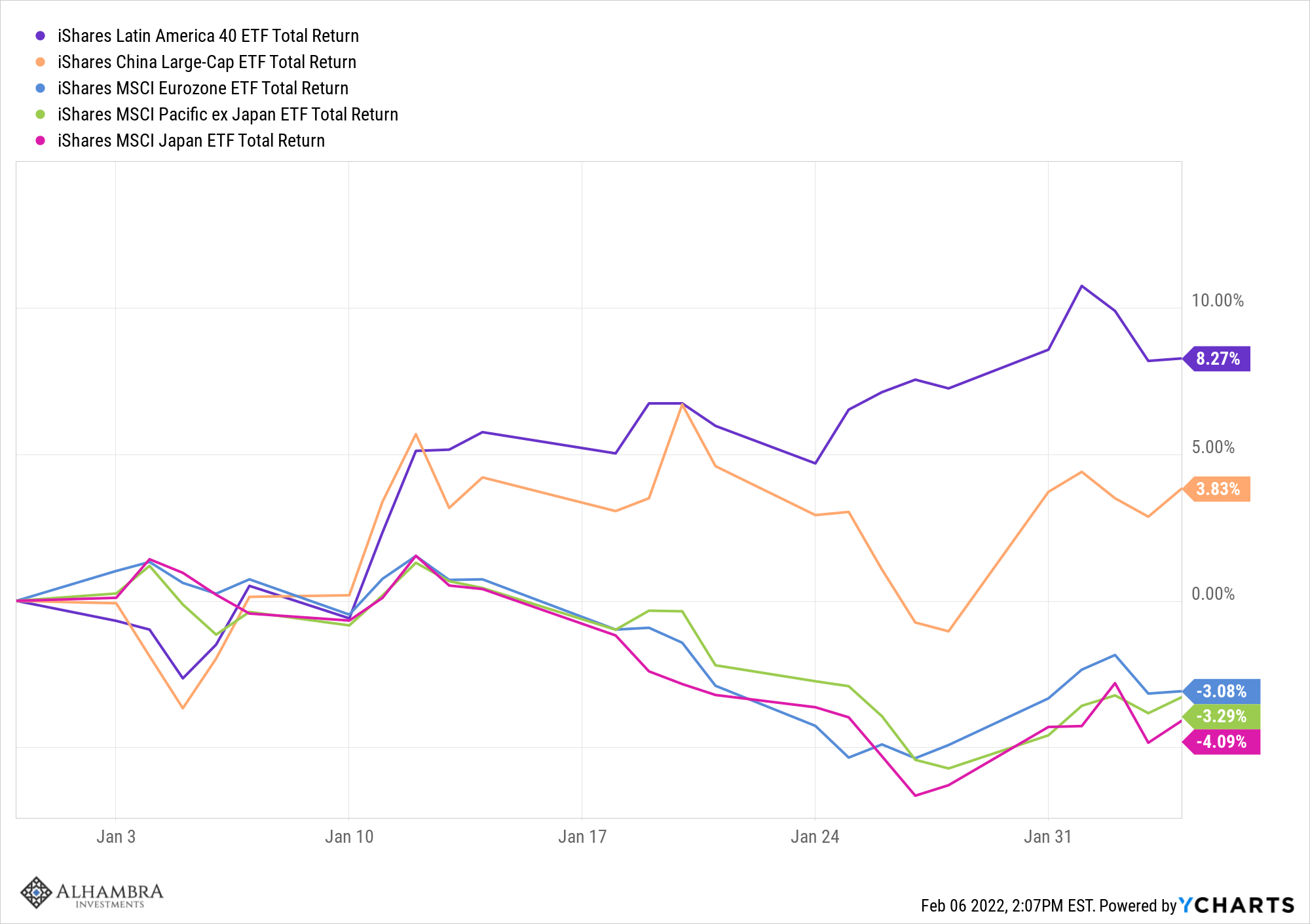

There are assets doing well this year but you probably haven’t heard about them because they aren’t sexy or part of the daily Twitter wars. Did you know Deutsche Bank was up nearly 17% – last week? And 26% on the year? HSBC is up 23% YTD, Mitsubishi UFJ 17%. The Brazilian market is up 12.9%, Colombia 9.3%, and the Latin America ETF 8.3% year to date. Everybody knows that China is in a world of hurt and yet FXI is up nearly 4% this year. Everyone knows oil is up big this year but so are natural gas and palladium and platinum.

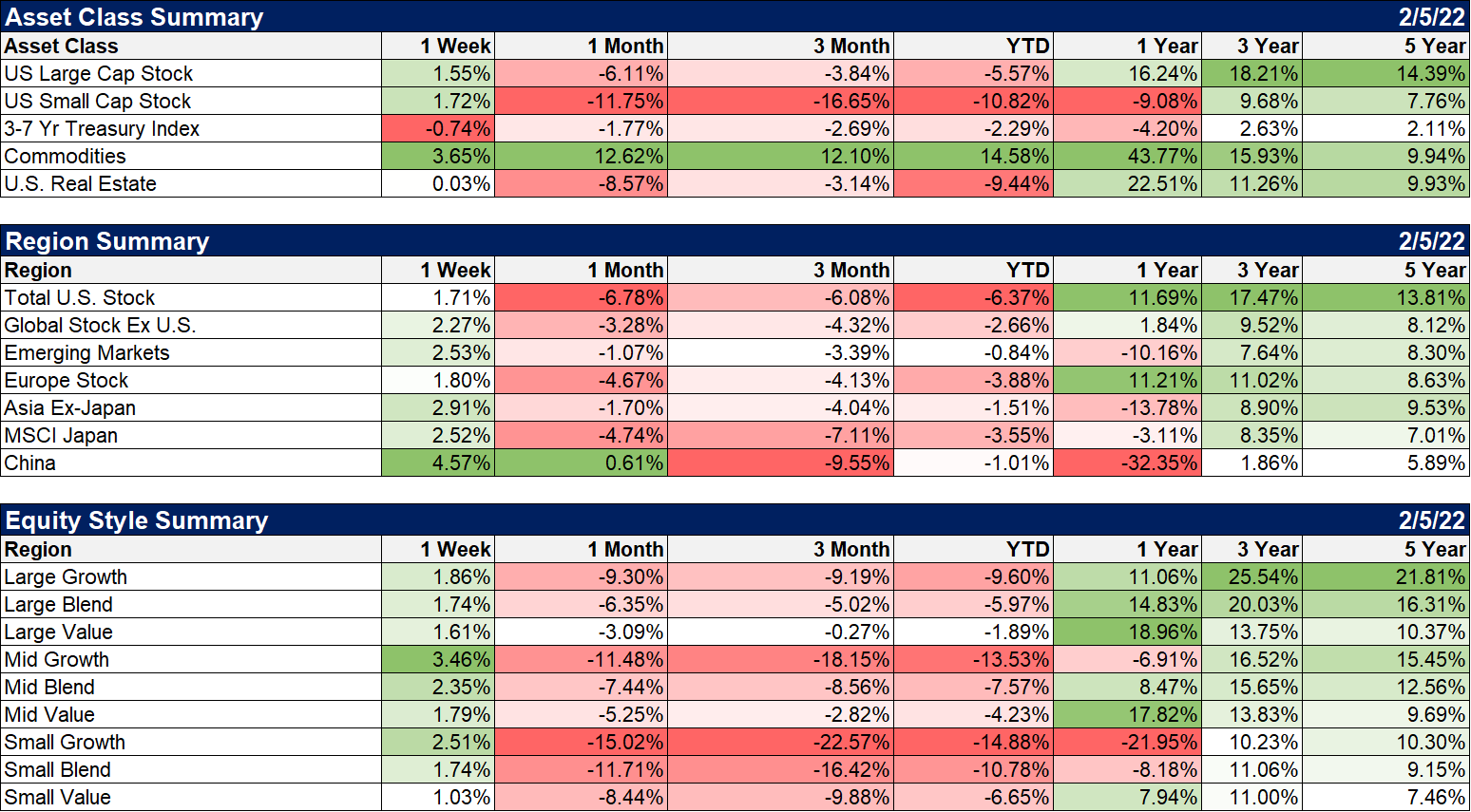

It is hard to predict what the next popular thing will be, which sector or asset the voters will take a shine to next. That’s why you need to diversify and consider a wide range of assets. Diversification can be frustrating at times because while you will probably own some of the winners, you are by definition going to own some of the losers too. In our portfolios, we own value and dividend stocks, which have beaten the market by a wide margin this year. Our portfolios also have a fairly large strategic allocation to real estate and REITs, the worst-performing sector this year to date. We minimized the damage somewhat by owning half of what our strategic allocation calls for, but we’ve taken a hit on real estate this year. We also own International value and US financials which have outperformed this year. And some small-cap stocks and large-cap biotechs which haven’t. And we own commodities, which are the best performing asset class year to date. And gold which has done nothing. We own emerging market stocks, which have outperformed, and US bonds which are down on the year. The overall result is a moderate portfolio that is down slightly for the year but less than half the drop of a standard 60/40, US stock/bond portfolio.

Over the last decade or so, it became popular to say that diversification no longer works or, in extreme cases, wasn’t necessary. All you had to do was buy large-cap US stocks – preferably tech stocks – and watch the money roll in. We disagreed with that then and we still do. For investors who want to earn a reasonable return without taking excessive risks, diversification is the only free lunch in the investment world. Diversification still works and we think you’re going to need more of it this year. The weighing of the highflyers is not over.

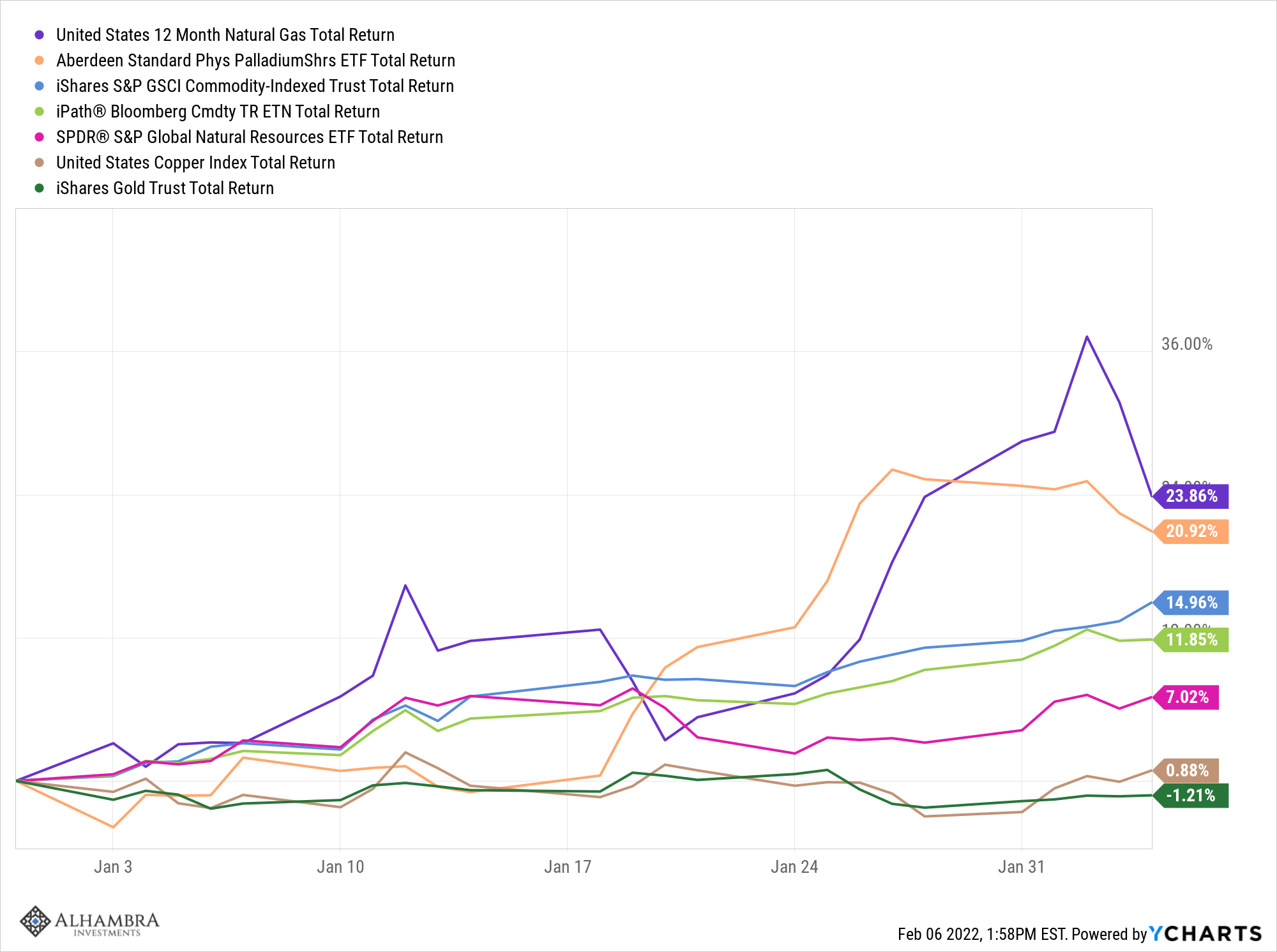

Commodities had another good week and the 1-year return is getting to territory where we think it might be time to do some rebalancing. The trend is up and you want to ride that as far as possible but there are limits.

Emerging market stocks returned to outperforming last week after a brief detour based on a spike in the dollar that turned out to be rather short-lived (more on that below). China led the way, up nearly 5% on the week.

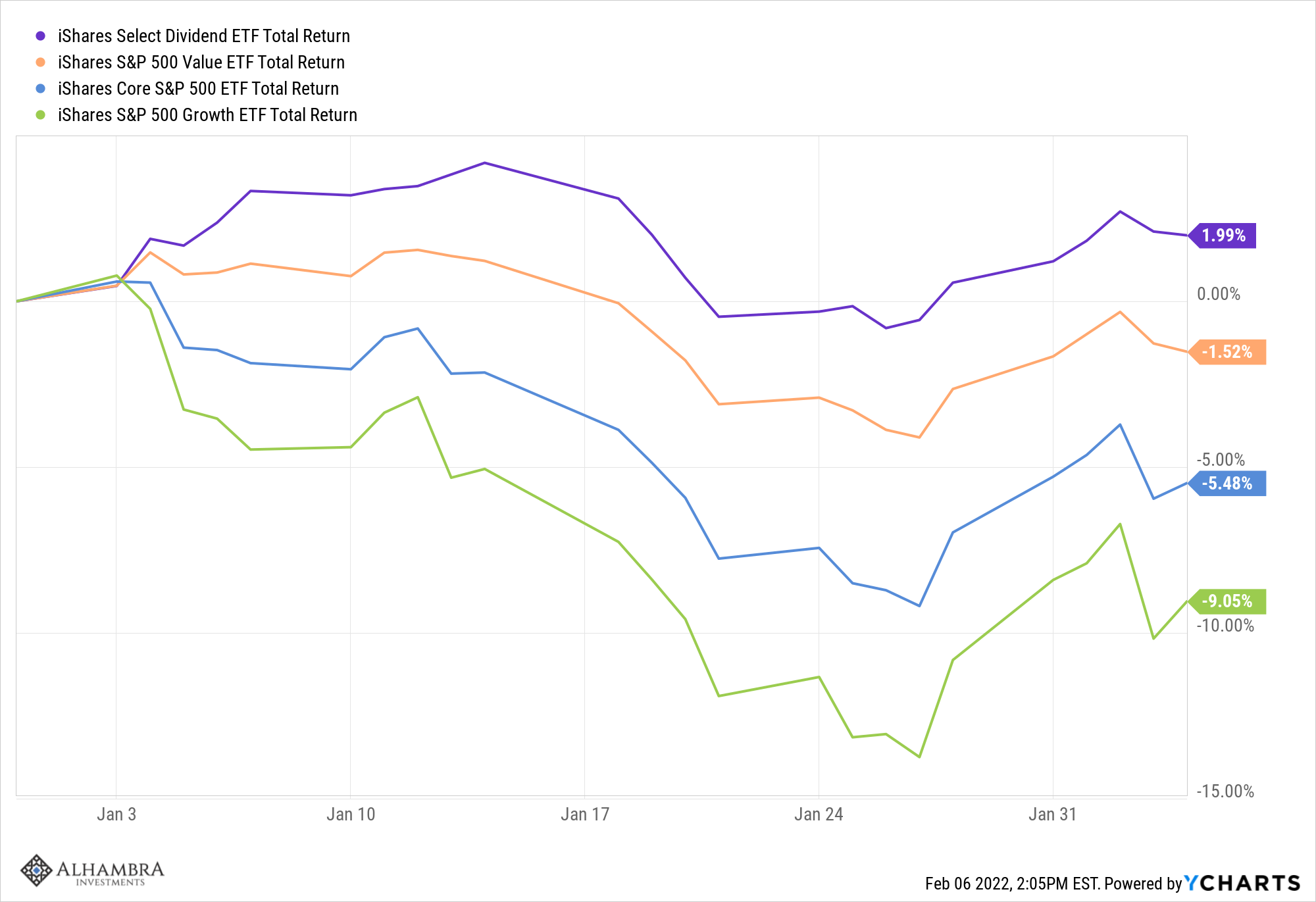

Growth stocks had a better week but as I said above, this looks like a rally in a downtrend for most of these stocks.

Dividend and value are both outperforming this year.

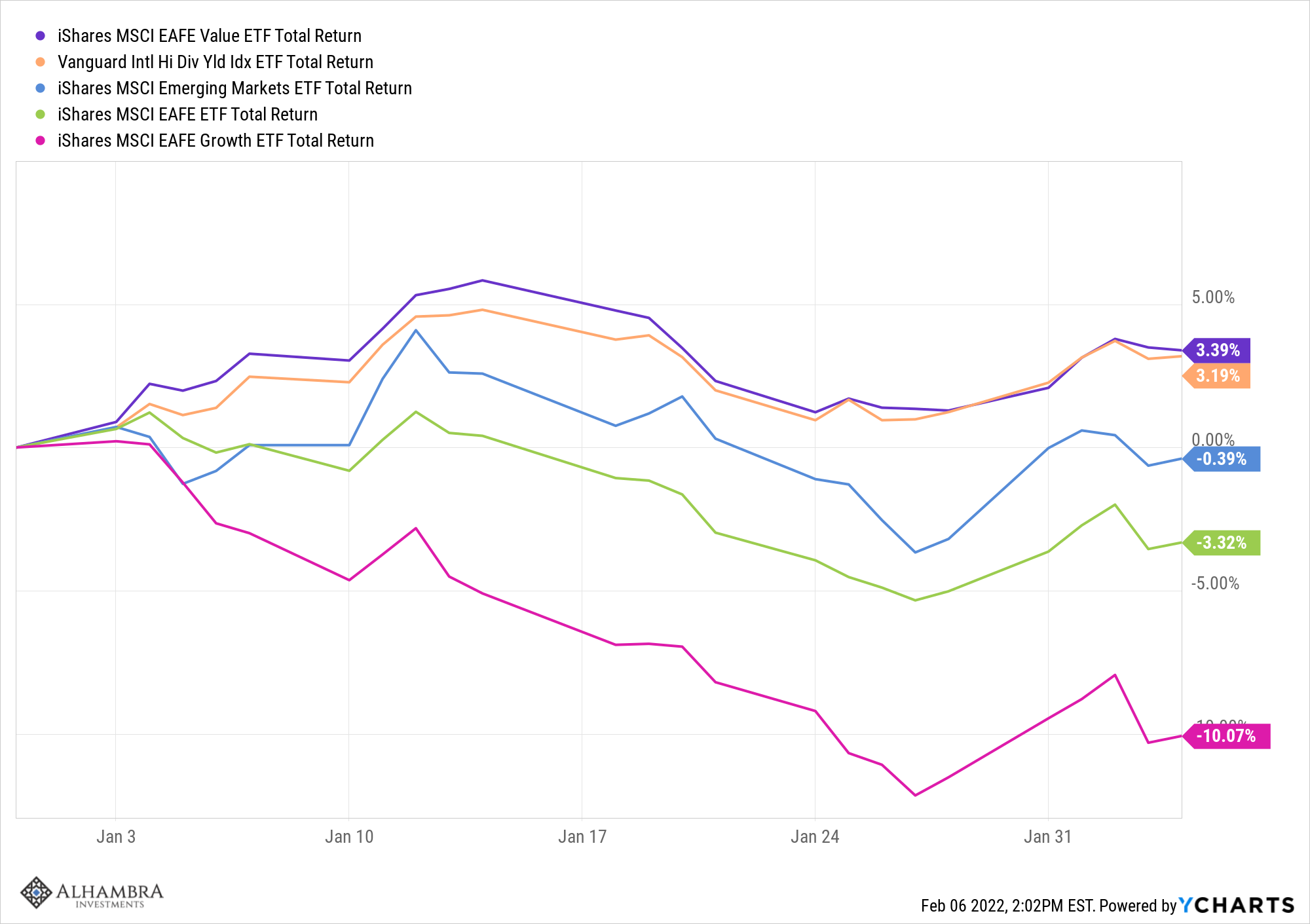

International is also outperforming with value and dividends also leading the way in non-US markets.

Latin America is the surprise winner so far this year. Brazil gets most of the attention but the rally is pretty widespread.

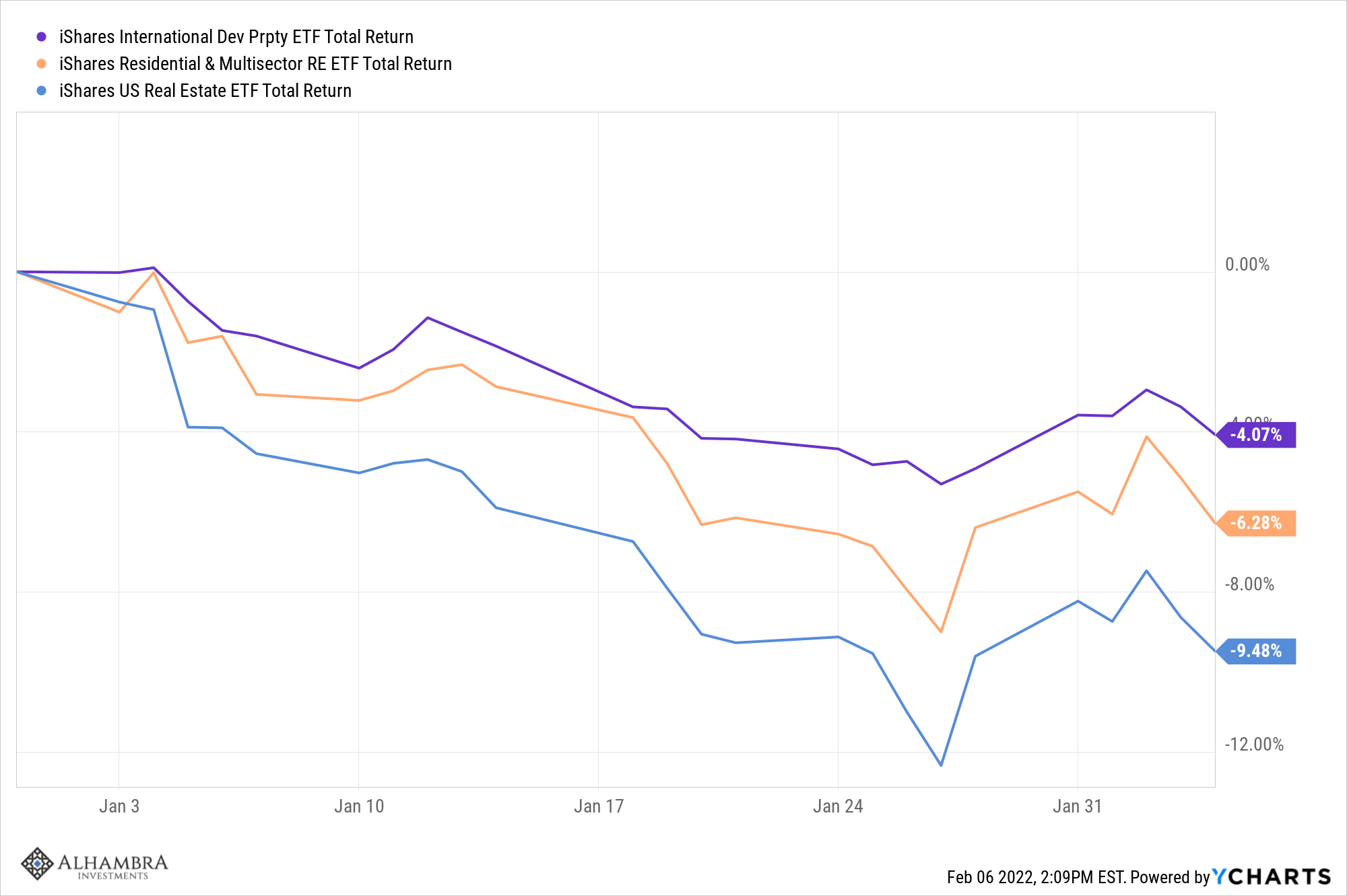

REITs have taken a hit this year but international markets are again outperforming. We have half our real estate exposure in international which hurt last year but is helping this year.

Commodities have been big winners this year but it isn’t just crude oil going up.

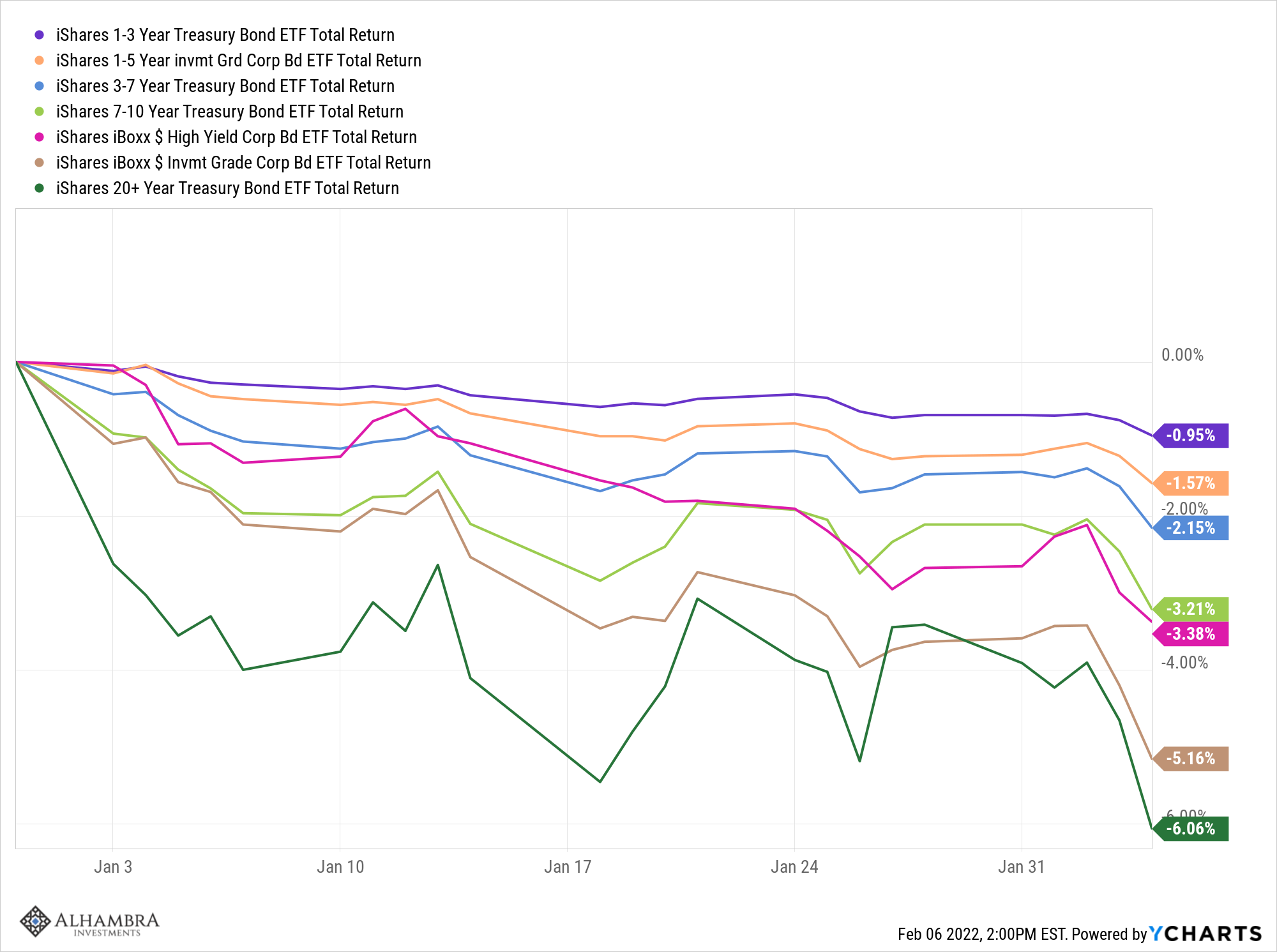

Bonds are down on the year and over the last year as well. In a rising rate environment, which is where we’ve been most of the time since August of 2020, you want to keep durations short. There is one bond market we follow that is up this year but isn’t listed in this chart – EM Local Currency bonds. EM currencies are up about 1% this year accounting for the gain.

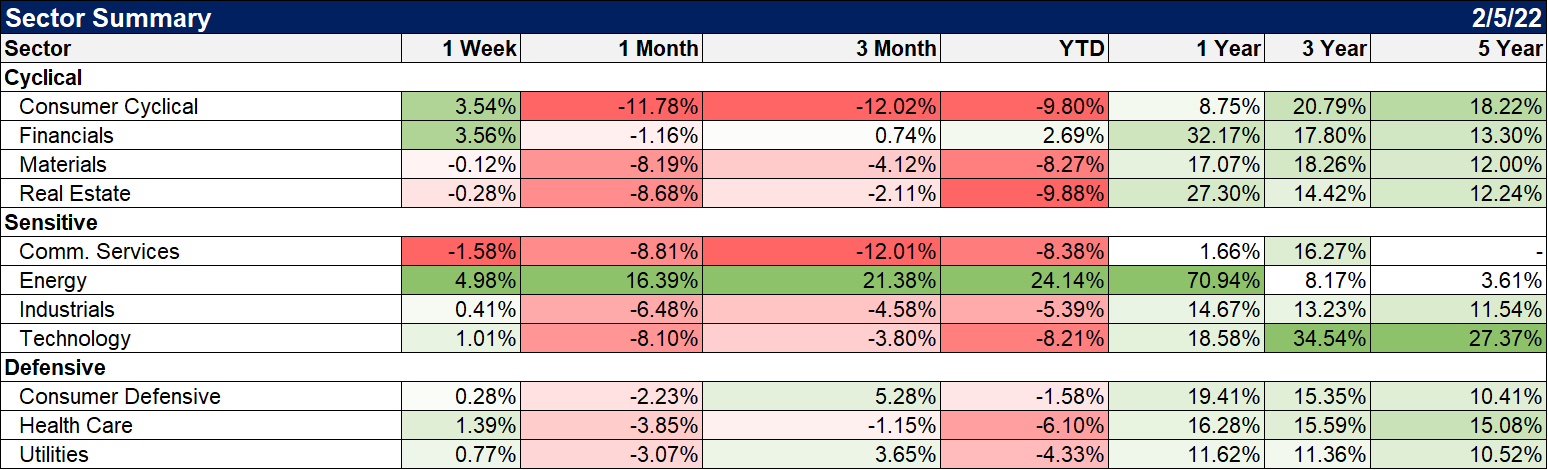

Financials and energy remain the only sectors up on the year and they both had good weeks.

We’re changing our graphic a bit to provide more information. We classify the economic environment broadly by what is happening to interest rates (10-year Treasury note yield) and the US Dollar (dollar index). At times how you see the environment depends on your perspective. So we decided to refine it a bit by showing what we really look at. We look at rates of change across various time frames. In this case, the dollar is down over the last month but up over 3,6, and 12 months. What that means is that the intermediate-term trend is still up but there is a potential trend change as the 1-month figure is negative. The long-term trend is a narrow trading range that has persisted for now 7 years. As for interest rates, the trend is up and obvious across all the relevant time frames. The nearly 2% drop in the dollar last week convinced me to hang onto our EM position and I’m glad I did. We’ll see where it goes but I continue to believe the trend is changing and that the dollar index will move back to the lower end of its long-term range.

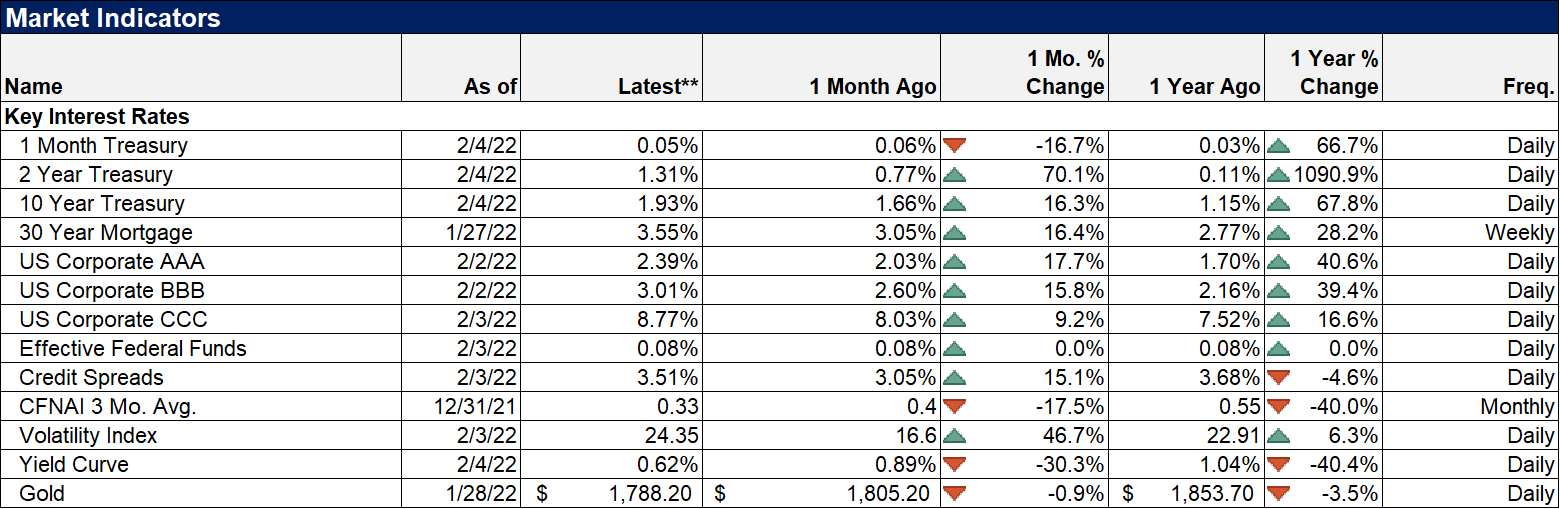

The yield curve continues to flatten but is still positively sloped and was flatter by all of one basis point last week in the context of a 15 basis point rise in the 10-year Treasury yield. The move in Treasuries was interesting more because rates didn’t fall with any of the weak economic data last week – not that it was all that negative. But a negative print on the ADP employment report had essentially no impact. What really seemed to get rates moving up was the hawkish (at least that’s how it was taken) talk by Largarde at the ECB. The German bund is back in positive yield territory for now and that seemed to accelerate selling in US Treasuries. That was also when the dollar took a big hit. It would seem that a lot of people believe there are a lot of Europeans parked in Treasuries and if Euro rates and the Euro go up, they’ll sell Treasuries and the dollar. I’m a bit skeptical of that but the idea at least moved the market last week.

I saw a research piece last week that pointed to widening credit spreads as a warning sign for the economy. It is true that spreads are wider than they were a few weeks ago. It is also true that they are no wider today than they were in December and they are lower than they’ve been for most of the time since the late 90s. To say that spreads constitute some kind of warning at these levels is just fear-mongering and angling for attention.

The stock market has been volatile of late and some individual stocks have made some extreme moves, but overall, the market averages have just had run-of-the-mill corrections. This is just normal market activity and happens about once every 18 months. Is it over? I still think probably not based on market sentiment – not enough fear yet. For those of us with diversified portfolios, January was a frustrating but not particularly painful month. Even if the markets continue their correction there will always be pockets of strength, parts of your portfolio that buck the trend. A lot of investors – and advisers – try to mitigate drawdowns through market timing and almost all fail. The better approach is to mitigate losses through portfolio design. That’s diversification and it still works.

Comments

Log in or sign up to join the conversation.