I'll let you complete the headline, each to one's own worldview; but the stock market is getting off easy blaming the Middle East for its current correction rather than its own excesses.

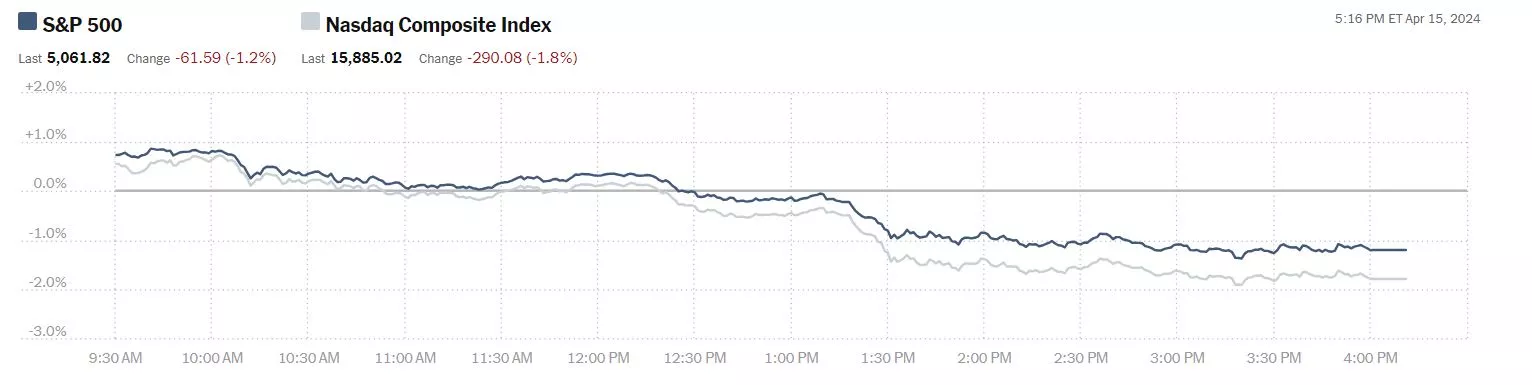

On Monday the S&P 500 closed at 5,062, down 62 points, the Dow closed at 37,735, down 248 points, and the Nasdaq Composite closed at 15,885, down 290 points.

Chart: The New York Times

Most actives were led by Tesla (TSLA), down 5.6%. followed by Apple (AAPL), down 2.2% and Ford (F), down 3%%

Chart: The New York Times

In morning futures trading, S&P 500 market futures are up 15 points, Dow market futures are up 271 points and Nasdaq 100 market futures are up 35 points.

TalkMarkets contributor Patrick Munnelly in his Daily Market Outlook - Tuesday, April 16, notes the correction in the NYSE made its way to Asian markets as well.

"On Tuesday, Asian stock markets experienced widespread declines, mirroring the sell-off on Wall Street the previous day. This was driven by a surge in bond yields after a report revealed stronger-than-expected U.S. retail sales growth in March. The data raised concerns that the US Fed may delay lowering interest rates in June. Additionally, traders remained wary of geopolitical tensions in the Middle East. Most Asian markets ended Monday with lower closing prices. In light of the latest data, CME Group's FedWatch Tool currently suggests only a 21.6 percent likelihood of a quarter point rate cut in June. In China, Q1 GDP growth came in at 5.3% year-on-year, surpassing forecasts, although March retail sales and industrial production fell short of expectations...

Later today, market focus will shift to US housing data and industrial production, following recent positive surprises in economic indicators, including stronger-than-expected retail sales. Consequently, expectations for Federal Reserve rate cuts this year have been scaled back...

Overnight Newswire Updates of Note

- China First-Quarter GDP Grows 5.3%, Beating Estimates

- Israel’s Military Chief: Will Respond To Iran’s Weekend Attack

- US, Europe Seek To Dissuade Israel From Striking Back Against Iran

- US Speaker: House Will Vote On Ukraine And Israel Aid This Week

- Fed’s Daly Says No Urgency To Cut, Policy In A Good Place

- Japan's Yen Hits A Fresh Three-Decade Low Of 154

- China Loosens Grip On Yuan By Weakening Fix Amid USD Strength

- Tesla Plans To Lay Off More Than 10% Of Workforce

- Lockheed Wins US Missile Defense Contract Worth $17 Bln"

You can find additional updates and predictions in the full outlook.

The "blame" game moves to Australia as contributor Akhtar Faruqui notes AUD/JPY Falls To Near 99.00 Amid Market Caution, Awaits Israel’s Reaction To Iran’s Attack.

"AUD/JPY relinquishes its recent gains, likely attributable to risk aversion as investors await Israel’s reaction to Iran’s air strike on Saturday with caution. Furthermore, the Australian Dollar (AUD) encounters obstacles amid apprehensions that the Reserve Bank of Australia (RBA) may be compelled to reduce interest rates in the foreseeable future. The AUD/JPY cross trades around 99.10 during the European session on Tuesday.

The Australian Dollar (FXA) faces increased negative sentiment, which contributes to downward pressure for the AUD/JPY cross. This sentiment is driven by divergent monetary policy outlooks between the Reserve Bank of Australia (RBA) and the Federal Reserve (Fed). The “Financial Review” suggests that the RBA may need to ease monetary policy before the Fed. Furthermore, persistent high inflation in the United States (US), the world's largest economy, introduces uncertainty regarding whether the Federal Reserve will take action this year.

Moreover, the Australian Dollar pares losses after mixed data from its significant trading partner, China (CYB). This rebound may have helped to mitigate the losses of the AUD/JPY cross...

Per Reuter’s reports on Tuesday, Japan's Chief Cabinet Secretary Yoshimasa Hayashi emphasized the importance of currencies moving in a stable manner that reflects underlying fundamentals. He noted that authorities are closely monitoring foreign exchange (FX) movements and are prepared to take all necessary measures to ensure stability...

AUD/JPY

| OVERVIEW | |

|---|---|

| Today last price | 99.12 |

| Today Daily Change | -0.27 |

| Today Daily Change % | -0.27 |

| Today daily open | 99.39 |

Similarly, Japanese Finance Minister Shunichi Suzuki reiterated his vigilance regarding FX movements and affirmed his readiness to implement any measures deemed necessary... "

Contributors Chris Turner, Francesco Pesole, and Frantisek Taborsky write that CNY Depreciation Risk Adds To Bullish Dollar Tone.

"As if high US inflation and strong activity data, geopolitical risks and a looming ECB rate cut were not enough to drive the dollar stronger, the dollar could now be buoyed by Chinese authorities allowing a weaker renminbi (CYB)...

USD: The dollar has plenty going for it

Instead of geopolitical risks, Monday's FX session was dominated by the very strong March US retail sales numbers. Consumption was meant to be the weak link in the US economy, but the lack of slowdown in this segment very much supports the view that the Federal Reserve is in no rush to cut rates. US two-year Treasury yields pushed back close to 5.00% and the dollar extended recent gains.

The broadly stronger dollar is now having some ramifications for Asian currencies. Many high-yielding or high-profile currencies such as the Indonesian rupiah and Korean won are falling sharply - alongside the Japanese yen. The fact that China has been keeping the renminbi stable has meant that the trade-weighted renminbi has surged about 1.3% (quite a big move) over the last week. On investors' minds is the question of whether the People's Bank of China (PBoC) will now allow more flexibility into the renminbi - a not unwelcome development given very low Chinese inflation and weak export growth. That is why investors are hyper-sensitive to the PBoC's daily USD/CNY fixing.

Back on 22 March, the PBoC experimented with a fixing above 7.10 - which resulted in heavy losses for both the onshore and offshore renminbi. Subsequent fixes were made sub 7.10, but last night the PBoC fixed USD/CNY at 7.1028 - suggesting it was acceding to market pressure to allow the renminbi to weaken. The prospect of the PBoC allowing a weaker renminbi is a bullish one for USD/Asia and for the dollar in general. The highest correlations with the CNH in the G10 space are the Australian and New Zealand dollars. In the EM space, apart from the directly managed Singapore dollar, the South African rand has the highest correlation with the CNH.

In short, should the PBoC start to allow a higher series of USD/CNY fixings - acceding to market pressure - it could prove a boost to the dollar around the world."

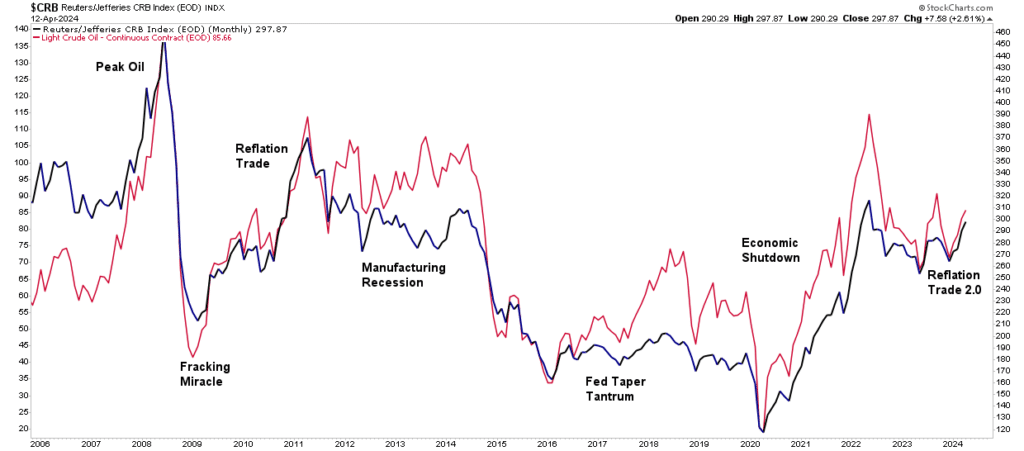

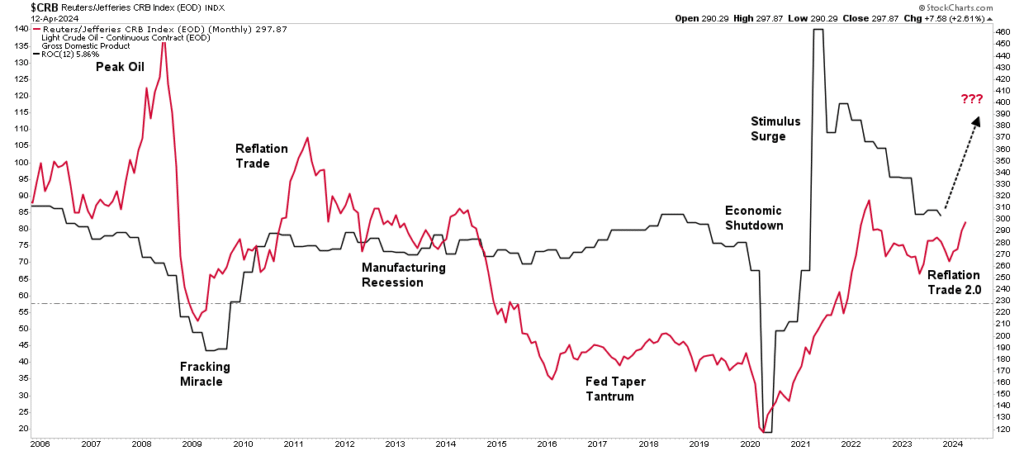

Contributor Lance Roberts alerts readers today to a current trend (narrative), Reflation Trade Is The New Bullish Narrative.

"Economic “reflation” is becoming the next bullish narrative as equity valuation increases continue to outpace earnings gains, at least according to Gold Sachs and Tony Pasquariello.

“If GS is correct on the big calls, the macro backdrop is set to remain friendly: the US economy should continue to grow nicely above trend — picking up speed as the year moves along — with three adjustment rates cuts along the way. to not obscure the moral of that story: the Fed is set to ease policy … into an upswing. while Fedspeak this week had a somewhat hawkish bent, the house view for 2024 remains intact.”

Interest rates, gold, and commodity prices have increased in the past few months. Unsurprisingly, the bullish narrative to support that rise has gained traction. Interestingly, this “reflation” narrative tends to resurface by Wall Street whenever there is a need to explain the surge in commodity prices. Notably, the last time Wall Street focused on the reflation trade was in 2009, as noted by the WSJ:

“The most talked-about investing strategy these days isn’t stuffing money in a mattress, it’s the reflation trade — the bet that the world economy will rebound, driving up interest rates and commodities prices.”

While that “reflation trade” lasted for about two years, it quickly failed as economic growth returned to 2%-ish growth along with inflation and interest rates. As shown, oil and commodity prices have a very high correlation. The critical reason is that higher oil prices reduce economic demand. As consumption falls, so does the demand for commodities in general. Therefore, if commodity prices are to “reflate,” as shown, such will depend on more robust economic activity.

As such. The reflation trade hinges on a global resurgence of economic activity, usually associated with economies recovering from a recessionary period. However, the U.S. never experienced a recession. As discussed in “Deficit Spending,” despite numerous recessionary signals, like the inverted yield curve, manufacturing data, and leading economic indicators, the economy avoided recession due to massive governmental spending. To wit:

“One explanation for this has been the surge in Federal expenditures since the end of 2022 stemming from the Inflation Reduction and CHIPs Acts. The second reason is that GDP was so grossly elevated from the $5 Trillion in previous fiscal policies that the lag effect is taking longer than historical norms to resolve.”

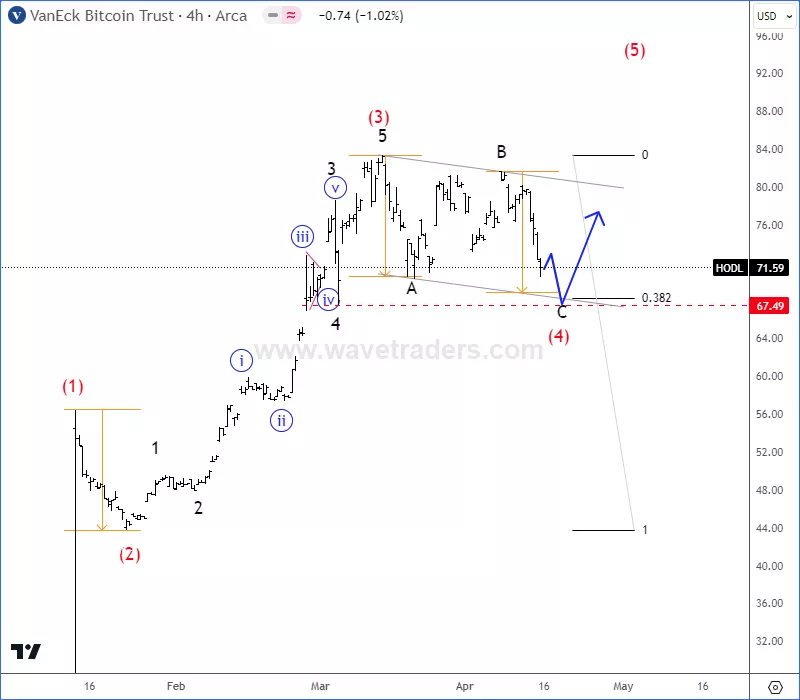

Looking over to crypto, TM contributor Gregor Horvat says that Altcoin Season Is Ready To Resume.

"We talked about ALTcoin season already back on June 27th of 2023, when we actually spotted the start of ALTcoin season. Clink here.

ALT season have slow down recently, due to a bullish Bitcoin dominance, but now that Bitcoin dominance can be finishing an impulsive cycle, ALTcoin dominance may step in again.

Crypto total market cap can be still finishing an A-B-C flat correction within wave (4) ahead of BTC halving, which is scheduled for Friday April 19th. Ideal support is still around 2.0T area, so soon be aware of a bullish continuation for wave (5).

Even if we take a look at VanEck Bitcoin ETF with ticker HODL, we can see it finishing an A-B-C flat correction in wave (4) with textbook support around 68-67 area.

Long story short: When Bitcoin (BITCOMP) completes its wave 4 correction and will be on the way back to highs for wave 5, this is when ALTcoins could fly high."

Looking for something to chew on? TalkMarket contributor Timothy Taylor tells us Why So Many Shareholders Of US Firms Are Untaxed.

"Over the last half-century or so, the share of corporate stock that is owned by investors with taxable mutual funds or brokerage accounts has fallen dramatically. Steven M. Rosenthal and Livia Mucciolo tell the story in “Who’s Left to Tax? Grappling With a Dwindling Shareholder Tax Base” (Tax Notes, April 1, 2024).

Here’s their figure showing a breakdown of who owns stock in US publicly traded corporations. Back in the 1980s, 80% of this ownership was in the form of taxable accounts. However the share of US corporate stock held by foreign investors and retirement accounts has risen substantially, and nonprofits own a chunk of US corporate stocks as well. So in the last two decades, only 20-30% of US corporate stock is in taxable accounts.

Rosenthal and Mucciolo offer some additional discussion of how these groups are taxed. For example, dividends paid by US firms are taxable, even when paid to foreign investors, but these payments are governed by international treaties. They explain: “However, the rate is often reduced by tax treaties between the United States and the home country of the foreign investor: from 30 percent to 15 percent on portfolio investment dividends, for example, and 5 percent or even 0 percent on dividends from direct investments.” Foreign investors do not pay capital gains on stocks to the US government–instead, such gains are taxable in their home country. If US firms use the increasingly common practice of distributing funds to their investors by repurchasing their shares, then such payments are treated as capital gains, not dividends.

For retirement accounts, the common practice is that the money is not taxed when it goes into the account, and the returns are not taxed as they occur over time. Instead, retirement money is taxed as income to the taxpayer when it is received after retirement. Nonprofit, of course, is not subject to income taxes.

With these patterns in mind, proposals for taxing owners of corporate stock as a group–not just the minority who hold their investments in taxable brokerage and mutual fund accounts–are going to run into complexities. Dramatic changes in retirement accounts or international tax treaties are not a simple matter, in politics or economics. Jacking up taxes on the 20-30% of shareholders who are taxable would create incentives to push their share even lower. One can make an argument that a reason for an explicit tax on corporate income is that it has become so difficult to tax the gains to shareholders of those firms."

Hmmm...

That's a wrap for today.

Have a good one.

Peace.

More By This Author:

Thoughts For Thursday: About Those Rate Cuts

Tuesday Talk: April Is The Cruelest Month?

Tuesday Talk: Big-Tech Under Attack

Comments

Log in or sign up to join the conversation.