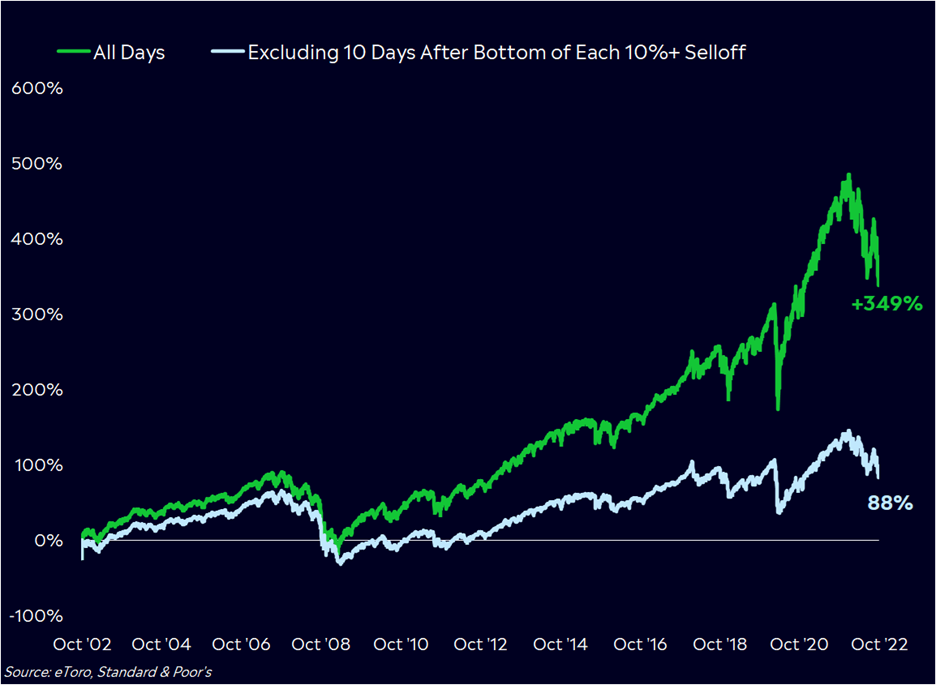

Today I saw an interesting statistic that I wanted to share with you. If you sold stocks at the bottom of each 10% selloff, and then bought back 10 days later, you’d miss out on over 2/3rds of the gains since 2002. This really speaks to the strange dynamics of financial markets.

I was speaking with one of my coworkers yesterday and we were discussing Citigroup trading at 50% tangible book value per share. Each 100 bps in Federal Funds rates adds about $2.5 billion to their pretax net interest income, but that hasn’t stopped the stock from dropping.

In a fearful market, fundamentals temporarily don’t matter. This is why it is important to let time do its thing, and as earnings come out over the next couple of quarters, catalysts will arrive which close the disconnect between stock price and intrinsic value, which hovers around $80 per share conservatively.

These could be good earnings results that lead to upgrades, stock buybacks to take advantage of current prices, or selling a non-core business at a higher price than expected to highlight the underlying value of the business, etc.

So many people and analysts are predicting another leg down in the markets. Pessimism is exceptionally high for the obvious reasons. There doesn’t seem to be a clear exit plan on this horrible war in Ukraine. Inflation remains stubbornly high, and the Fed continues to jawbone that it intends to keep raising rates.

Many people that expect stocks to continue to decline, bail out and go to cash. These are the same people that miss 2/3rds of the gains that come from staying invested. Earnings season starts in earnest on Friday with many of the big banks reporting. I expect generally strong earnings. There will be some headlines about leveraged loan losses, but those will be very small in relation to the many billions in net profits.

Book values per share decline a bit as higher rates lower the other comprehensive income from their large bond portfolios, but ultimately that money is earned back from higher net investment income. Dividends are very high, and in a few quarters, we’ll see stock buybacks come back more significantly, which should be a big catalyst.

Credit is very strong, and while it will get worse as the economy weakens, it shouldn’t prevent the banks from being robustly profitable, which is a big difference from prior recessions.

The VIX, or volatility index, has recently been seen trading in the mid-30’s, which is very high. This dramatically increases the prices of options, causing wide market fluctuations. Remember that at options expiration (which for most of our options is in late January), time value and volatility value go to zero. This is why we often see a nice surge in our account values as we arrive in December and January.

I believe this year that could be very significant, and for some accounts, we could potentially see 10%-plus moves even with stocks trading where they are at currently. This is a big dynamic that we really try to stress to investors, as it doesn’t work the same way as a traditional stock and bond portfolio. Time works to your advantage.

You are living through a long and nasty bear market. The S&P 500 has been down 14 of the last 17 trading days. The Nasdaq has lost a third of its value year-to-date. Even a so-called conservative 60/40 portfolio is down 21% year-to-date, on pace to become the second worst year in history after 1931.

The long-term UK Gilt bonds have posted a return of -52.3% since December of 2021, wiping out a whole decade of gains. The Fear and Greed Index is at 17/100, indicating extreme fear. All of this has already happened.

Markets have a great track record after mid-term elections, including the last two months of the year and the following year as well. According to Mike Zaccardi, during the last 90 years, the S&P 500 has generated a median return of 3% through year-end and 17% during the 12 months following mid-term elections.

I think we will see some very robust results coming out of this, and the fact that we have held up far better than the market should make it much easier to capitalize on those moves. The market isn’t going to give you an all-clear sign when the bear market is over. It will just happen, and we are likely much closer to the end than the beginning, if we look at the history.

More By This Author:

S&P Down 25% YTD, Investment Grade Bonds Down 22%

When to Expect Recovery in a Bear Market

Update on Bank Earnings

Comments

Log in or sign up to join the conversation.