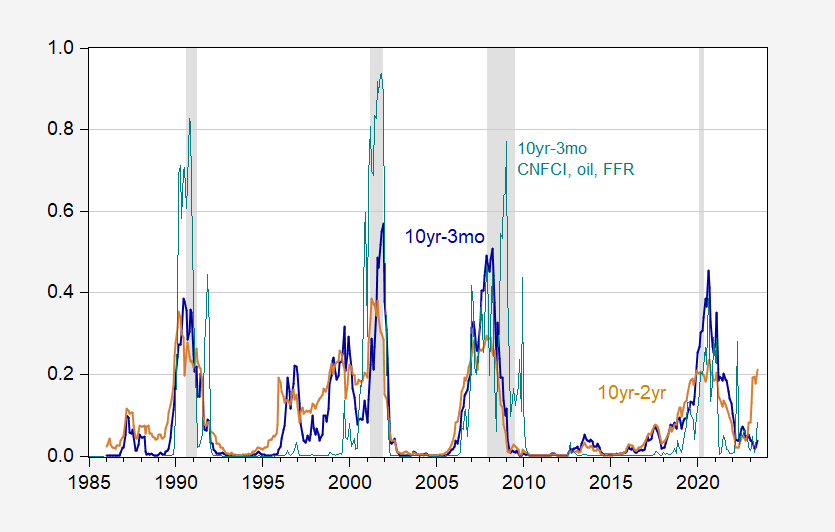

Probabilities from 10yr-3mo and 10yr-2yr spreads:

Figure 1: Probability of recession for indicated month, using 10yr-3mo spread (blue), using 10yr-2yr spread (brown), and 10yr-3mo spread augmented with Fed funds rate, Chicago Financial Conditions Index, 12 month change in oil price (teal). NBER defined recession dates peak-to-trough shaded gray. Source: Treasury via FRED, NBER, author’s calculations.

Probabilities for June 2023 are 3.8% and 21.2% for the 10yr-3mo and 10yr-2yr spreads. If one augments the 10yr-3mo with Chicago Financial Conditions Index, Fed funds rate, and 12-month change in oil price, then the probability is 8.4%. Note this specification is similar to the one used by Ahmed (2022), except for the exclusion of foreign spreads and stock market variables (the McFadden R2 is 0.51, vs. 0.28 for unaugmented).

I’m certain alternative term spread models, including other variables, could lead to higher implied probabilities of recession, but the plain vanilla ones don’t at the moment lead to higher than 22% (10yr-2yr) at the 12-month horizon (26% at the 18-month horizon for 2023M12).

Comments

Log in or sign up to join the conversation.